Weekend Rebel Review June 14th, 2024

Bulls, bears and bores.

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

Aren’t elections such fun? I say elections, to use the proper technical term, a ‘liarfest’. Rather like these rare plants in Kew Gardens that grow all year round in a dormant sort of way then suddenly, once in every five years it burst into flower, and we see this huge bloom flourishing like some wonderful event that everyone pays attention to. So too then is the election, when all these politicians come out with promises and lies on huge scales and we listen to them and know that none of them are true but we have to vote for one of them. I’ll be voting Monster Raving Looney because at least they admit they haven’t a clue. Only another three weeks of this and then it’ll all be over. The stock market had started to pick up this week and had finally seen a bit of action after two weeks of complete doldrums. Trading statements are starting to appear before the end of June for companies with our June 30 half year end. I don’t know what has spooked the market mid way through the election, I can only guess. Realising that these manifestos aren’t going to change a lot perhaps, changes to CGT rates may have got into them minds of many. Macron called an election right after the EU results so perhaps that spooked some wondering if he and Sunak knew something. Couple that with April GDP being flat and traders can easily start conjuring up all sorts of false demons in their mind.

It can be tough sometimes not to be drawn into any selling after a long run of up-weeks on the market. When markets have long runs of strong performance, it’s good to remember there’s a broad spectrum of people in the market from novices to professionals. Most professionals with a long term outlook will be happy to see a fall back and accept that’s what’s happening it’s just normal, even a chance to increase holdings cheaply. As a seasoned veteran, I try to think about what others are thinking rather than think too hard myself. I know when I was serving my apprenticeship as a professional private investor/trader20+ years ago, the mistake I made was to snatch profits in a bull market. For an hour you feel good when the share goes nowhere and you’ve banked some cash. But invariably, when you snatch profits in a bull market, it isn’t long before you are thinking you should have hung on, when stocks hit new highs. In a bull market, the overall momentum is upwards. I try to use any fall in the market to trim my poor performers and add to my winners. Stocks that have 30-40% gains or more in weeks have usually risen for a reason and are likely to continue. If you sell them you’ll sit and feel like you are missing out as they carry on up. You then end up buying back in with regret, and often at more than what you sold for. Your next issue is where do you reinvest the money? Finding something better than what you have sold can often be a task. I’d say, before you sell, make sure you have a much better home for the money lined up. When markets have big rallies then short term tops, think hard before scalping a few quid – you can end up giving far too much to your broker in my opinion.

Wherever or whatever the cause, it has been a weak week for the markets this side of the water. The FTSE250 has continued to form a rolling top on a short term basis.

There is a support around this level but if that goes, there could be another 3% to give back to the next main support. Why the weakness? Well April GDP data was flat which may have been part but the market rose on that news in the hope of an earlier rate cut. The weakness affected Europe too, in fact on Thursday the CAC and DAX were off more than the 250 so I am inclined to think it was more a larger macro thing than just the UK as these indexes have rolled over too. Sometimes markets just need to have a bout of profit taking to get the bulls excited to buy the bargains.

The DAX Germany

The CAC France

The VIX has been weakening and still looks pretty benign

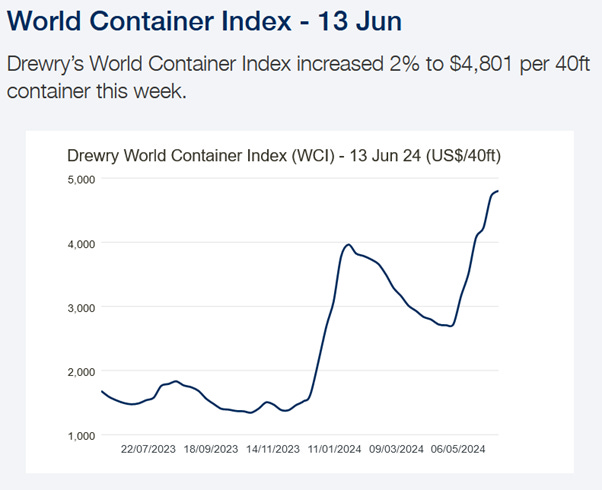

Fear/Greed is still right around at Fear and 42The intriguing thing is shipping costs are still firming which with the absence of any global events can only mean market demand picking up to me. Whether the supply side is improving we won’t know till we here more from businesses with their trading updates later this month and in July.

The market is definitely in a bit of a sell off but having given back 3%, on the 250, how much more will it give back? I have given back 4% from my high this year but I was up 27% from the start of the year. How much does it cost to pay the dealing and spread to trade out and back in?

A bit more in the way of results and perhaps things will firm.

Meanwhile, Wednesday seemed to kick off the return to punters being surprised by trading updates. Frontier Developments, FDEV, featured here in April, put out there trading update which was ahead of expectations:

https://cockneyrebel.substack.com/p/lets-get-ready-to-rumbleeee

The board said they were comfortable with forecasts for 2025.

The rather bowly share broke out to a new recent high with a 17% rally.

Up over 50% since featured here two months ago, I have scalped a lot of profit from these to go into others in my portfolio which I see as far more attractive, but could still be plenty more in FDEV imo.

Through to Thursday and after a close up over 1% higher the previous day the market opened quiet but there was a few bits of interest around. I have been watching AT. recently because having sold near the top, the shares have fallen back over 20% and tumbled back to a great support level so I have started buying back a small few, it’s an ugly chart a the moment, but may be set to bounce.

Another very small cap has been on my buy list too recently. Now before I say anything else, this is incredibly illiquid and hard to deal in at the best of times, so easy to get locked in on bad news. Definitely risky and not for the risk averse. The company is Dialight, DIA, who are manufacturers of LED lighting, similar to LUCE. It is a potential recovery play for me. I’m not looking at the forecasts or recent performance, I’m interested as to where the co could go in the future. As of 31 December 2023, the Group had net bank debt of £12.3m (2022: £20.9m) after having raised £9.8m of proceeds from the equity fund raising completed on October 2023.

In Feb this year the co said Steve Blair would take over as CEO from Fariyal Khanbabi who had been at the helm for 4 years.

In January they had a new CFO - Carolyn Zhang.

In Jan 2023 they had a new Chairman on an interim basis, David Thomas.

The co is forecast to do 8.6p eps this year, 12.9p for 2024.

In 2014 they were doing 36.8p eps and paying a 15p divi on £159m sales – they are expected to do £169m sales this year and there are no more shares now than then.

So it’s a margin recovery story and can the new CEO/CFO get margins back to where they were 10 years ago?

That’s all interesting and there’s a nice bowl on the chart too, but this is a special situation play also. The co is involved in a litigation with Sanmina regarding termination of manufacturing agreements as announced on 29th of November:

Basically DIA could win up to $220m + costs or lose up to $8.3m + costs. This case goes to court in mid July though it could be settled out of court prior then. At the top of the compensation figure, Dialight would receive double he company’s current market cap.

I started buying a few weeks ago, a very small few and it went nowhere, then the thing moved up 10% on Wednesday in a rush of little buys and low and behold a trading update on Thursday said the co was trading inline.

Again, I am not advocating buying it, and 5k is the average daily amount of shares traded. But it is good to be aware of special situations so if there is news you can move fast through being better informed than most.

In Brief:

Funding Circle came off near 10% Thursday when the market was weak. D.Bank who a month or two ago stuck a 250p Buy target on FCH reduced that target to 210p Buy. I never saw the first note or this adjustment so I don’t know what their thinking is/was, but it’s still 100% above the current share price.

Lastly, Greencore GNC -in the news tonight due to an issue with E-Coli. Tracing this E-Coli source has been on going and I suspect the cause of a bit of the weakness in the share price. It seems a salad leaf supplier to Greencore, Samworth Brothers and one other co has an issue with E-Coli and have been identified as the source. M&S don’t seem to have been affected from what I have heard so far today, Greencore have a dedicated factory in Northampton for them and I guess their salad is sourced elsewhere but that hasn’t been confirmed.

The share price has already given back some but bearing in mind GNC voluntarily recalled sandwiches and the source is now identified, it doesn’t look like a long term or large issue for GNC imo. Perhaps a buying opportunity before great results in July? There will be an RNS on Monday I am sure.

That’s it, not a huge week to cover again but H1 end, pre-close trading updates should start rolling out and livening up the market. Being a stock picker will help hugely I’m sure.

Have a good weekend, remember, I’m not an investment advisor or analyst, just a private investor recounting my diary. No advice or tips here, do your research please

Cockney

I don't know, not a stock that interests me much. I do know they will get a one of gain from getting rid of their copper network but the debt load these is huge and they seem to borrow more to pay higher divis which seems mad. But I guess the divi is keeping investors investors interested. What Carlos Slim sees interesting I don't know.

Happily I can find better debt-free co's that could perform better in mid to small caps.

Interest8ng comment on Dialight