Let's get ready to rumbleeee!!!

Are you ready for this?.....

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

Today kicks off the start of a new financial year. It’s always great to have a financial year out of the way. All the end of year crystalising of gains for CGT purposes means lots of weird selling in March and often it’s the great winners of the year where the CGT is the highest and punters may want or need to crystalise to use up allowances. That seems to have come along after the gains from October, prior to that, many never had much in gains to utilise imo. Next week will see those that want to add cash to their ISAs start to do so – so more cash in the market.

The Macro:

It was good to see UK Manufacturing PMI come in above 50 on Tuesday. Anything over 50 signals expansion. Contrast that with Germany just scraping over 40, they are in a deep manufacturing recession. Europe as a whole was at 46.1, France at 46.2 while the UK at 50.3. Italy at 50.4, Spain at 51.4. On Friday UK Construction PMI hit 50.2, indicating expansion. There is no way the UK is being valued for its performance imo. Years of doom and gloom about Brexit in the media but the truth isn’t reflected in the real data. The problem is the City is so insular and don’t see the real world out there. It seems to me that the City is where they most feel sorry for themselves too, how London feels is how the rest of us feel obviously to them. I think there’s plenty more shocks coming for the City as companies report. I’ve lost count of the amount of stocks rallying 20% + on results or news lately.

The VIX has looked very benign up until Thursday night’s spike, it has firmed by 14% on Thursday after Fed words spooked the mkt on interest rates. I would look to that possibly testing 18 as a high, it doesn’t seem the sort of news to push the VIX way higher so I suspect if it gets to 18, the punters will be piling in. The big fall on the US on Thursday spooked the UK and caused a sell off. I spent all the cash I had on Friday, now back up to fully invested while we ended down, and the US rebounded, our market mugged again.

Meanwhile the Russell 2000 since mid January has trended upwards continuously – it feels like the FANGS are getting a bit long in the tooth (no fee for that gag 😊) and money in the US is heading towards small caps where there’s greater value and the most benefit from interest rate cuts in my opinion:

Fear Greed has drifted right back and at mid Greed now – that’s very positive for a strong rally ahead at some point imo, but there may need to be a move into neutral or fear before it fully bounces – the S&P has had a huge run, it’s good to have pull backs to draw new investors in.

Lastly the Dow Transport still seems to be firming:

Interestingly the FTSE250 is curving upwards lately, that signifies increasing buying strength in the market in my opinion.

More interestingly the FTSE100 has a bowl set to break out to a new all-time high, I expect that break out to come next week.

All this is happening right at the end of the financial year. The market feels firmer, rate cuts look closer here if not in the US and if we get a bit of momentum I’m sure FOMO will kick in.

We have already started seeing it – CMCX has been roaring away, up 120% year to date and many other stocks are posting firm gains, even if indexes aren’t making great headway.

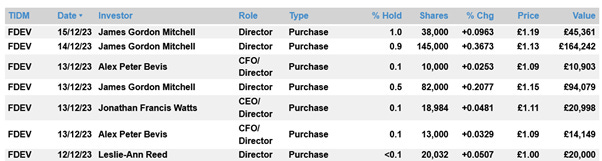

Frontier Developments, FDEV the video game developers, has seen a 30% rally in 3 days after posting a trading update. It’s up 50% year to date. I’m not really into gaming stocks but couldn’t help notice the bowl that has now formed on the chart which I love seeing. There has also been solid director buying recently.

The last interesting feature is that there has been virtually no dilution in the shares since 2018, 39m then, 40m today. Here’s the chart, 95% off the high:

FDEV’s put out a trading update on 2nd of April which triggered the rally. In it they said “Frontier's cash position grew to £23.4 million as of 31st March 2024, up from £19.9 million as at 31st December 2023.” They have sold publishing rights of Roller Coaster 3 . It sounds like there’s further cash to come in too in 2025. They were already net cash of £1.88m as of the full year results according to Stockopedia. With a market cap of Just £72m this weekend, that looks potentially cheap, backed by a lot of director buying. Directors rarely buy for short term scalps imo. I have been buying these now the bowl has shown up. Who knows how far back up that chart they could go but I do know stocks like this are likely hugely undervalued after 3 years of fall and punters hiding in cash or the US shares. I’d need to do a lot more research to feel comfortable holding them very long term but for the medium term I have seen enough to think they could be mighty cheap and have some decent gains ahead.

There are lots more big rallies I could cite, ITV up 40% in 3 weeks – you just wasn’t seeing these moves before Christmas hardly. We might not be seeing FOMO (Fear Of Missing Out) but Concern of Missing Out is creeping in.

Someone posted this to me this week off Morningstar – fund flows inwards into UK Small Cap funds for the first time in 2 years+. That bodes well for Liontrust, LIO, which I hold and other Small Cap Funds and stocks imo. Liontrust should have a trading update on 17th April.

Liontrust. LIO

One stock I have been buying over the past week is Greencore, GNC. I did a short write up on my November 26th Weekend Review having bought them for a trade. As it happens I should have probably hung on but there were several other stocks I liked more at the time so I just took a small profit. The trading update sounded pretty decent but it didn’t set my heart on fire. Greencore are the worlds largest pre-packed sandwich maker. They make food for MKS among others and they have a dedicated supply factory in Northampton just for MKS. They make 795m sandwiches a year, 2m a day, for all the major supermarkets. Together with on the go snacks, they also do chilled soups and 2000 other products. in fact they are the worlds largest pre-packed sandwich maker.

What interested me was the 15mm in share buy backs they were doing, this is now completed, reducing the shares in issue by around 10%+ from 2019 and over 30% from 2018. They had a new CEO 18 months ago, Dalton Phillips who came from ‘daa Ireland’ where he was CEO for 5 years, a large global airport and travel retail group. They have had a new Chairman, and in February Catherine Gubbins has been appointed to the role of Chief Financial Officer – she also came from daa Ireland so I presume she was CFO where Dalton Philips was CEO – he sees to have rated her by the praise he dished out in the RNS. Also in recent months, 4 directors bought meaningful amounts of shares.

Recently there has been a story that activist investors Oasis have acquired nearly 5 % and they are pushing the board for changes, complaining that they haven’t paid a divi while BAKK and PFD have despite having weaker financials. Oasis are the activists who got involved at RTN before they recently got taken over. Since 2018 net debt has fallen from £501m to £199m. I’d ignore the bid noise and just think of that as a possible bonus. Greencore got rid of the ill-fated US business, 5-6 years ago. Dalton Philips CEO has reduced 250 management jobs and ended duff contracts and made significant cost savings – it all has the mood music of a great recovery play in action imo.

All of this and the recent curve up in the chart has got me buying them over the last 10 days. In 2018 they were doing circa 13p eps on sales that were 30% less than the co will do this year. There’s also over 30% less shares than then too. If they can get margins back up to 5.2% that they had 6 years ago from the 3.45% they are currently doing then EPS is likely to be 18p or perhaps more imo.

The recent trading update says they are trading inline:

If they hit the highs of these forecast they will be on a forward PE of approximately 10, I think they can do better. They are forecast to reinstate a divi this year of 1.8p this year and 3.3p next year. With directors buying, a bowly chart and an activist chipping away at them, plus 15m share buy back this year reducing the number of share then I think they could beat. Times have been tougher recently too – may workers taking a sandwich to work with them rather than buying on the go but with NI cuts and a £1 rise to the living wage then perhaps peeps will feel they can have that lunchtime treat a bit more often. The shares started to take off on Tuesday with huge volume , around 3%+ of the company’s shares traded on the day, they have been up every day this week. Interims are on May 21st. With a market cap now of over £620m at the time of writing, they should go into the FTSE250 come the next reshuffle along with CMC Markets imo, if they continue to make positive progress.

You may find this interesting

I’ll say it again, do your own research, don’t trust me, I own the share so I could be no different to a car salesman. I’m also dyslexic so I may have read this totally wrong and you’ll never know unless you research for yourself.

Another I have bought is SYNT.

Synthomer are a world-leading supplier of high-performance, highly specialised polymers and ingredients such as coatings, construction, adhesives, and health and protection – growing markets that serve billions of end users worldwide.

I sold TIFS at a loss this week as I said I likely would last weekend as directors haven’t bought any shares even on the placing dip – that’s just not good enough. The directors don’t have much of an holding and they should be showing support and at least buying some shares in a dip like that in my opinion. I used the cash to take a position in SYNT with what looks like a bowl now in the making with the shares nearly 95% off their high of £42- very a la AVON. They were clobbered hard after governments bought up all the latex gloves they could and left the planet with a massive overstocking issue. This sounds like it may now be unwiding. Michael Willome comes across as a guy that knows what he is doing but has faced a huge task to keep the debt in hand and the bankers at bay. He seems right across the numbers and a very capable guy that doesn’t dodge a question. He and the CFO have been good buyers of shares. They have halved net debt to £555m but that’s still more than the mkt cap. But they have forecasts of 6.62p eps this year and 24.7p eps next year and a lot of the competition has gone to the wall. If sales pick up sooner or better than expected these could have a long way to bounce.

One really positive feature there has been the board’s confidence shown by share buying. They have bought deeply over the past year and rather reminiscent of Rolls Royce before their huge bounce imo, and completely opposite to TIFS. Again, do your own research, this isn’t a tip, it’s just me doing what I do and talking about it. The results webcast is a good place to start imo

https://stream.brrmedia.co.uk/broadcast/65dc7b44994661e3abf8b33c/660a9943f0472c009c2ea0c2

It also won’t take much more of a rally for these to get back in the FTSE250.

So, I think the market is turning decidedly bullish. A Tory defeat has to be priced in along with Brexit and Armageddon imo. Punters have run shy, pension funds have moved most of their investment abroad, but if the market can be anything it can be fickle imo. If the UK markets start to rally I can see a replay somewhat, where fear turns to FOMO, a re-run of the Covid bounce in many respects. If you’ve stuck in here for 3 years I think we may be about to be rewarded soon. Those that walked away will feel out of it and lost when we do get the rally.

The big clue will be lots more co’s being met with decent rallies on just average statements.

Now remember I’m a perma bull and I’m prone to getting a bit bullish after a Bovril or too, or some rare steak so take what I say with a pinch of salt.

For the last time – don’t trust me, I’m a simpleton, do your own research and be sure – this is just idea-generation.

Have a great weekend and stay wide awake and up early next week

Rebel

Agree the debt is an issue and still over the market cap, which is why the shares are so cheap imo. But watching the results webcast I gained confidence that it can be dealt with. The director buying since June, while no guarantee, increases my confidence. The fastest ever 8 bagger I have held was Thomas Cook who's debt was huge compared to the market cap but a bit a new CEO, a bit of director buying and the share price rallied. Then a few bits of good news meant the shares rallied more. Then the market cap compared to the debt looked far greater and a much smaller placing looked necessarily to bring them back to something healthy. As brokers saw this coming they hiked their targets, also boosting the share price to 8 bag the stock in 6 months. I'm not saying that will happen here, but there runes are saying it's a similar situation in my opinion. Won't 8 bag in 6 months but could very easily one bag in 12 months, especially is these customer inventories are starting to run down imo. As ever, just my worthless opinion.

Loving the bullish commentary Cockney. Appreciate you making these updates public 👌🏻