Weekend Rebel Review, September 6th, 2024

Life returns.....MARS, CAR, FCH. FTC, GMS, CDGP and the market in general

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

So we enter September and things should liven up one way or another, up or down. September and October have reputations for being volatile, often not in a good way. But as an investor you have to plan accordingly. I’m still heavily in cash of 50%+. I’m still not keen on the market despite certain positives. In the middle east, Isreal dealt with the attack on them well with their Iron Dome which I suspected surprised Iran and led to Hamas saying ‘that was it’ and they backed away from escalating. I feel there’s a move to settle things going on so that is a positiv,e foremost for an end to all the killing that is happening but also for the markets. What that leaves us with is the uncertainty this new government is causing. Labour have not inherited the weakest economy since the war as they claim, they have been totally dishonest and despite the growth, investors don’t trust them – you need trust as a government. The Tories were also untrustworthy but you knew where they stood on tax and where they would spend/cut. Labour has introduced massive uncertainty, so those with pensions are cashing in a lot to make sure they extract their 25% tax-free lump sum they are currently allowed. This doesn’t help share prices to rally. We also haven’t seen what else will be in the budget so until that little pandoras box is opened, we are in a bit of limbo re uncertainty.

What happens to property under Labour? Taxing second properties, taxing landlords, rent caps? Will they raise CGT and/or stamp duty? That is just one sector I’m struggling to like. They have hit the pubs, never saw that coming, more below. What else? That’s the current issue – where do investors stand. Rumours of a £100k max gain in an ISA p.a. then you pay tax – at what rate? How does that help grow the economy? That’s the problem with Labour imo, they want to spend our money for us and that leads to wasting our money – nobody looks after your money better than you – just look at how people get scammed by investment frauds, pension frauds, it’s dead easy to waste other people’s money. Plane flights – will crazy Ed start taxing them as a green policy? MPs will keep flying and claiming the cost back for the taxpayer to pay. They are definitely going to need more than their £22bn ‘black hole’ bonus tax hike to do a lot of the greening – GB Energy is basically another tax – we own it of course, we never asked for it. As we own it then we get the profits or the losses - I’ll tell you now, there won’t be profits. All of these things drain the wallets and leave less to go around, so businesses don’t grow like they could. Fuel duty and taxing petrol off the road, that’s coming - not good if you rely on transport and delivery. So there’s a lot to be wary of but the country is growing much stronger than was expected too – so perhaps it can outpace the drag of the new government.

As for the market in general, I think fear of the budget and those with pensions cashing in, means many shares are trading lower than where they should in a normal market so at some point, either after the budget or during the earnings reports ahead of the budget, a lot of UK equities are going to take off on positive updates. I’m still around 50% cash but should I feel sentiment is changing then I won’t be afraid to pile back in, but I need to see solid evidence.

Indexes are all a bit undecipherable in my opinion. Germany seems to be in a mess, EV’s not selling and their industrial data all very poor but the DAX has hit a new high.

France is in a political mess but their market is getting bought after what looked like a big rolling top but may still be in one, the jury is out – you make your choice here, bounce off the long term trend or further to go for support?

As for the UK, well the 250 has gone sideways since the election was called, up a bit, down a bit but flat roughly, when the UK is growing faster than the whole of Europe.

It has been noticeable that since the election was called, acquisitions of UK co’s seem to have died a death nearly. It was pleasing to see on Monday that Rightmove have attracted interest. Perhaps international investors have started to say b****x to it, let’s make a move, or perhaps that’s me being too bullish.

The 250 has a big bowl on a longer term but for now the Weis Wave is firmly red indicating selling rather than committed buying.

The FTSE Small Cap mirrors the bowl on the 250 but recent trading has been firmer.

In the US the Dow Jones has hit a new high, the S&P is testing the high and the Nasdaq has been in slight retreat, but holding up well. With rate cuts coming, it looks positive there while here in the UK we seem to be heading for more austerity and inflation looks like it will be stronger than it was, thanks to give aways to unions and rising energy prices, tho retail prices have been falling so perhaps not.

The VIX has risen a bit, fear/greed has stayed stuck in Fear, at 41, just below neutral. The Russel nd the Dow Transport have come back a bit still but nothing alarming.

I did say last week that August had been slow, but I expected September to pick up with lots of trading updates, it seems to have started.

I have bought more FTC after the rather excellent trading update last week and contract win within their framework agreement with SpaceX. Here’s the FTC chart – there are three times the number of shares in circulation since that huge high at the start of the millennium so the previous high is new money is around 250p. there’s a big resistance set to crack at 96p approximately. The curve up on the chart is as steep as it was in the past big rise.

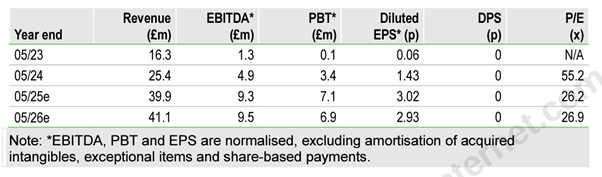

Edison has increased its forecasts:

FTC are only 3 months into this financial year.

FTC have announced £29.3m contract wins from SpaceX since April, all will be fulfilled this year. That is in 4 months. The framework agreement and the warrant based on that agreement are for an ‘at least’ amount of orders on a regular basis. With £29m+ won in in just over 4 months, it is hard to see how they only do £39.5m sales for the whole year, when they have a number of other clients too.

Earnings are already forecast to double+ this year. The current PE is 26. The earnings growth is over 110% which gives a PEG of 0.23, hideously low imo. There is no guarantee they can keep this growth up but with the demand from LEO satellites ad other potential clients like Jeff Bezos who is also putting up a satellite communication system like SpaceX, the much better margins in these applications and a new CEO in Nat Edigton from within the industry and fully understanding scaling up, I just see ever more likelihood of further earnings upgrades. Thus far these devices have been going into satellite ground stations. Filtronic are working on a system to go into the payloads (satellites) themselves which could mean even more of these RF devices. As they scale up volume, margins rise. With FTC the only co in the world that can produce these things with so much experience and huge barriers to entry and Musk having taken 5% and probably 10% eventually via warrants, it is just rare to see such an exciting company here in the UK – it reminds me so much of Arm Holdings in many ways. I now hold more than I had before selling down in July. I watched an Elon Musk video last week showing broadband in the middle of nowhere using his Starlink system incorporating FTC’s technology – 140Mbp download, four times faster than what I get from BT superfast broadband. On Friday Filtronic announced their brand new state of the art facility that doubles their research and manufacturing capability:

Tuesday saw a couple of results that interested me.

Global Marine Services, GMS posted results inline, tho dilute eps was down slightly, due to more shares around through exercised warrants. The fall in the debt ratio was more impressive and on a PE of 5.7 they look cheap to me. The market seemed to feel different tho – market sentiment is what matters – if markets were on the up, these would have been bought up imo.

Chapel Down Group, CDGP, the English wine makers put out some dire results. I have followed these for some time, in fact it is one of the few shares I have ever bought right on the bottom. Fortunately I sold the lot within a year having doubled my money. The stock was far too illiquid for me. This week they announced sales and profits down while stock and debt were way higher – add to that, CEO Andrew Carter is leaving.

I always thought Andrew had the best job on earth, all I saw each day on X was him at some major sporting event, promoting their wines and socialising, schmoosing with clients, buyers and sponsors. I don’t think I’d have resigned!

Marstons, MARS. Well that was poor timing on my part. Trading massively under net assets and looked a killer trade. Then out of the blue, Two Tier Kier decides he wants to stop smoking in pub gardens and raise the minimum pricing on alcohol. These two measures will ruin pubs, especially the cheap end. Haven’t they been through enough with Covid? Tell me this, if minimum pricing is brought in, how does it affect London? Probably not much because prices are already higher. Are there many pub gardens in London? Not many. So it’s the pubs in the country and suburbs that get hit. Not sure how much Starmer wants to raise prices, I’m already paying £12 for a large Sauvignon at my local but there will be lots of pubs where the less wealthy go, like Wetherspoons who trade on ‘cheap’ that will get hit. I think MARS rank in that group. So there’s now a big cloud over the sector till legislation goes through. I decided to halve what I bought, took the loss, running the rest for a while to see what the market seems to think before selling more if I do. That’s how timing and luck work sometimes, but often something a lot better on the news front comes along and makes up for the bad stuff in spades, and so it did! Good stock picking can win through even in tough markets, tho it isn’t as easy as a raging bull market where anyone can pick winners. It’s nice when a stock or two does come good because it gives you that boost in a tough market that you need sometimes, even a perma bull!

Thursday saw Funding Circle, FCH, post interim results. These were very pleasing as the co announced it would be profitable for the full year rather than just H2 which was the prior forecast. The co achieved a 0.1p eps in H1 from continuing operations. A 2.3p loss per share was forecast for the year. If H2 is profitable too as were the forecasts and they are ahead as they say then it looks like they are at least 2.4p ahead of those forecasts, possibly somewhat more ahead.

They have also announced there will be another £25m share buy back when the existing one ends. The number of shares in circulation are already 3% lower than last year. It’s easy for them to do this too as they have £164m in unrestricted net cash still, even after what they have spent doing buy backs – more than half the current market cap.

Disposing of the US for a £10m gain was great business, seeing they hadn’t had the banking license in the US for 5 minutes and the market had changed as far as co’s like FCH having to stump up more cash by way of deposits.

Interesting was the statement that “progressed cost-efficiency actions, to deliver c.£15m of annualised benefit in 2025”. This comes on top of the co saying they expects revenue growth of 15% to 20% in medium term. They also say they expects pretax profit margins of over 15% in medium term. If you make £15m cost savings then that should go straight to the bottom line going fwd. 15% pbt margins on sales of nearly 190m next year would be eps far higher than existing forecasts imo but it’s nice to see forecasts that can easily be well beaten. Flexipay transaction growth of 57% shows great growth, and the Cash Back Credit Card introduction could add further profitability. With total income up from £60m to £79m that’s real solid growth for a fintech on a non-fintech rating imo.

I will let you read the full results for yourself in the RNS but I found them very encouraging. I am only holding around half what I did hold, having one-bagged them but very happy with what I hold and I added more back on Thurs morning as this was way better than I expected. The market was very happy, with an immediate 23% rally by 10am and a new recent high on the chart at the close with the shares up 30% on the day. Not many shares hitting new recent highs at the moment. D.Bank raised their target for FCH from 170p to 180p. I think that could prove a modest call, 15% pbt margin on £190m sales would be more like 6p eps in the coming year. Strip the cash out and the PE is 12 or so for a high growth fincap, should trade on a much higher rating and will imo. I expect any pull back to get bought up fast where punters are scared to miss out. Rockwood trimmed a few FCH on Friday. They are up 300% odd I think and when you are holding a large stake in an illiquid company you have to sell when you can, into strength. not when you want to. They have created a little short term opportunity for buyers perhaps.

Remember to do your research, I might be wrong or dishonest, I might be way too optimistic and you’ll never know unless you verify what I have said by doing your own independent research. Great double bowl on the chart imo.

On Thursday, Carclo CAR, also had their AGM and trading update.

This was another fine report with progress across the board. There were no numbers but for the past two years, this trading update hasn’t carried numbers – yet Doorenbosch has delivered, so you need a little trust until the November interims where they will spell out the performance in detail.

CTP Design & Engineering, CTP US Manufacturing Solutions, CTP EMEA Manufacturing Solutions, Speciality Division all performing positively from what the co says. The last of the production in Tucson, Arizona has arrived and the centralisation of the business now in Pennsylvania means Tucson can close and costs reduced even more.

You can’t want more than that from a trading update, none of the ‘howevers’ in there to take the shine off things, progress across the board. This guidance was nice in my opinion:

“Our expectations for the FY25 full year and FY26 remain unchanged with margin expansion anticipated to continue as the Group starts to see the full benefits of the operational optimisation process, continuing our journey toward our strategic goals of 10% return on sales and 25% return on capital employed.” If they achieve this they should be doing double digit earnings before too long imo. ROCE according to Stocko is currently 2.5% so they are forecasting a 10 fold increase.

There is yet to be news on the pension revaluation which is expected to reduce the deficit substantially and possibly reduce payments into the pension. This triennial valuation started in March so I am hoping/expecting news by the interims in November, the co has said there would be news later this year. Panmure said this about the pension deficit back in July:

“We expect Carclo to release an updated actuarial pension valuation later this year which hopefully will disclose a lower pension deficit. Given our methodology to derive the target price, should the deficit be say £70m (i.e. £13m lower than the deficit reported in 2021), it would add a further 17p to our target price, a material increase. Furthermore, there could also be a reduction in the annual funding of the deficit which is currently stands at £4.0m”.

Carclo is my number one recovery play holding. There has only been 10% share dilution from the £5 high on the chart and they only had £97m sales then. CAR has sales of £133m-£144m over the coming two year. CAR had a big rating back in 2013 but even a quarter of that rating on what is more than 50% more sales than back then should easily get CAR into £1+ territory if they keep delivering as promised imo. Another point to look back at is 2017 where they did 12p+ eps and there has been no share dilution since then, although the pension deficit was a lot lower then. The shares were trading at 175p then so even taking into account the higher pension deficit which now seems to be falling, I still see £1+ potential. CEO of two years, Frank Doorenbosch, has delivered a decent recovery and with his history of turning around plastics co RPC he has good form. Back good management imo.

The shares rallied 27% on Thursday to a new recent high too. This is the thing with recovery plays, they can flop or they can 30 bag. There is no guarantees, this is higher risk, higher potential reward. I like to determine which way it is going and it seems to be the right way, so I hold and have been adding. Obviously I would say do your own research as these are a big holding of mine and I am bound to be biased and talking my own book. Very similar chart to FCH.

I suppose having half as many FCH as I had, could make someone miffed but having doubled my money on them it’s never wrong to take profits on a double, especially if that leaves you with free carry, or shares that have cost you nothing.

CAR I had already got back up to my highest number of shares a week ago so that was great, I increased my holding more on Thursday, well over 10% holding now.

That has been my week, a 4%+ gain on Thurs on the overall portfolio, nearly 7% up ignoring what is sat in cash – I don’t get many 4%+ days. Less than 1% from my high this year tho given back 1% of that nearly on Friday – I know how Frankenstein felt when they put electric into his neck-bolt – seems to have stirred me from what has been two months of mediocrity and negativity in the market.

I hope a lot of readers were lucky enough to hold FCH or CAR or both this week too. A few of interest net week:

10TH MPAC H1 results

10TH GAMA INTERIMS

10TH LUCE INTERIMS

10TH SPEC INTERIMS

10TH LORD INTERIMS

11TH DNLM FINALS

11TH TRST INTERIMS

12TH KIER FINALS

Have a good weekend.

Cockney.

Beyond the Zulu Principle is good. I have never read any others really, I read the Zulu Principle and used that as my bible for the first 5 years. Most other stuff I have learned watching the likes of Peter Lynch online and developing what works for me over the past 25 years using back testing and trial and error. I must have made all the mistakes there were to make in 25 years so I ought to be getting it right by now if I've learned from them!

I bought a few MPAC on Friday, forgot to mention sorry. Not the size I had but wanted a few to be holding into the results.