Weekend Rebel Review Oct12th, 2024.

What a SAGA!

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

What a market. The first thing to learn when you start investing is that the market is bi-polar. You will see weeks on end where everyone wants to buy shares, valuation doesn’t matter, picking a winner is like shooting fish in a barrel. Then the market changes, everyone is selling, all regretting buying or adding at the short term top. No matter what the reason for the buying, all that has gone out of the window, shares are falling and they just want to join in, they hate giving money back, it hurts, they just want pain relief. Then the bi-polar cycle starts again and the punters decide to buy the dip before the market gets away again. In most cases you should ignore the volatility. If you buy a cheap at £1 because it’s cheap, at 50p it’s screaming cheap. Minds run away, you can imagine all sorts of warnings coming and things that might have happened. In reality, most of the time, co’s are going along as guided, they haven’t suddenly hit a huge problem or struck gold, roughly things trend and stay in that trend. Annoying as it is, when your shares come off, the best bet is to just hold and ignore the moves in most cases, or add more, if you bought having researched well and you believe the story with conviction. Most stories don’t change that much, just investor sentiment changes. When you watch the 250 index soar 10% then fall 10%, do you really think all the companies in that index have suddenly had issues then suddenly recovered? Most of the time it’s sentiment, investors realising they had got too long at the highs and panic selling to reduce, then realising they have panicked too much at the low and buying back. Wasting time and money, we all do it, I do it, but I know I’m doing it. It’s about trying not to be jumpy, trying to keep those imaginary demons contained in a box in your head. Watch the RSI on a chart, when it’s really low and oversold, that is usually a great buying point, when it is way overbought, think about banking a little.

On the global side of things, China has pulled back a bit from the huge recent rally while the US has seen the S&P hit a new recent high.

The FTSE Small Cap index has continued on trend for that break out at the end of the month – the firmest UK index of the lot.

Fear/Greed is in the higher part of Greed still, likely it has further to go before a big bout of profit taking imo:

The VIX has crept back up to 20+ but that isn’t surprising with an election next month imo

Monday was a quiet day but the stand out was Beeks Financial Cloud, BKS.

I’m out my depth with the tech here, don’t understand how good it is, exactly how it differs from the competition and what the exchange win is worth that is being touted (Nasdaq I believe). I can only look at the valuation and on a PE of 48, falling to 38 it is way too expensive for me to buy. What is the chance of it doubling in a year on that PE ? I would think you could make an argument if the earnings history was great, but it isn’t, especially as sales have constantly risen.

While the sales have risen nearly 5 fold in 6 years the eps has been all over the place. The operating margins have gone from 16% in 2018/2019 to 0.5% in the trailing 12 months. The largest holder is Gordon McArthur who has 33% and been selling down. There isn’t a director buy in 3 years and just two director buys 6 years ago 49p and 70p.

If you have been holding it, well done. It looks like it’s net cash but the number of shares in issue has doubled in 5 years – that’s 15% dilution each year – the first 15% earnings growth each year is eaten by new shares. I guess the real problem for me is I can research as much as I like but a £150m UK co serving the largest index in the world seem a bit questionable as to what the competition is like and why can’t a big US co do what this little UK company can?

Way off my buy radar but caught my eye on a quiet day.

Greencore, GNC – the retail food supplier, which I highlighted here a few months back, said that trading was ahead of expectations. Greencore says full-year adjusted operating profit to be "ahead of current market expectations," and in a range of GBP95 to GBP97 million. This was raised from GBP90.5 to GBP92.5 million, so a 5% upgrade approximately – this caused a 15% rise in the share price to a new recent high. I like GNC, it looks a buy still, they have bought back £50m of the co shares and plan to buy back another £10m so the eps is being enhanced too. I hold M&S who Greencore supply. The news today increases my belief that M&S are doing very well. M&S rose 2p in sentiment.

Wednesday saw CMC Markets post their trading update for H1 to the end of September and very good it sounded imo:

£180m income and £51m pbt is way over 50% of full year expectations, by my calculations, that’s around 13p eps when forecasts are for 20.7p for the full year. At that run rate they will beat 2026 forecasts in this year (2025).

Just doing the same again in H2 should see 26p eps for the year. The co’s declared aim is to pay half full year earnings in a divi so the forecast of a 10.9p divi looks somewhat conservative. Obviously brokers may want to upgrade those numbers in the coming days but the shares gave back their gains later that day and on Thursday. Perhaps brokers and the market feel they are up with the events here on a PE of 12 or so.

When I sold down in July this was one of the two I kept hold of in size (aside from a few tiddly 1% ish holdings) along with Carclo, CAR so it’s pleasing to have faith rewarded. My only negative regarding the results was that they were a bit sort of ‘steadily’ regarding Revolut.

I’m sure there will be interest ahead of the results on Nov 21st. I’ve reduced down and banked some profits as the first of my buys are now up over 200% since Dec and I suspect these cannot one bag in a year from here – time to redistribute some of the gains into earlier OBIAY potential. I’ve been adding more to SAGA, MKS, RR. and GNS. I think of late I’ve been spreading myself a bit thin and was doing better with far fewer holdings, that’s just a consequence of selling out and back in and also being a bit undisciplined. You can sit and tell people as much as you like about discipline but it’s another thing to do it. Trying to be a bit too clever trading, while I should be all in or all out, I’ve given back 4-5% I need not have done by staying 80% cash but if I bought back in any time there’s a few percent cost that I would have to incur for trading. Difficult market but not as bad as some I’ve lived through - those heavy in tiny Aim stocks must be getting blended.

M&S, MKS saw yet another broker upgrade this week, there has been a fleet of them recently:

DEUTSCHE BANK RESEARCH RAISES MARKS & SPENCER PRICE TARGET TO 430 (350) PENCE - 'BUY'

That’s the 6th upgrade into the “Fours” in 3 weeks. The upgrade came as Kantar, the retail analysts said M&S’s sales increased 12.4 per cent in September. That was the biggest increase in the sector, surpassing gains by rivals Tesco and Sainsbury’s, and discounters Aldi and Lidl.

With hindsight, putting everything into MKS and RR. two years ago would have been a great, easy life investment ! I’ve been buying back both recently to increase my holdings. The charts have huge momentum and they both seem in a sweet spot – a nice place for cash while I wait for the Aim market to settle down and start rising again. The shares broke out through resistance to an 8 year high this week:

Another past featured share here is Marston, MARS, who put out a trading update on Wednesday, and the update came in pretty good and inline.

The chart is still making progress but not looking like a rapid one, there’s likely more exciting places to be imo.

Gulf Marine Services, GMS, highlighted here recently, announced a decent fall on the debt on Thurs together with a new contract Award:

Net debt was $410m in 2020, the above suggests the co has reduced debt since the start of the year by $46m. On a PE of 6.1 falling to 4.8 looks cheap and as debt falls the cost of servicing becomes less and means higher profits. All else being equal.

The market is bi-polar, people have been selling stocks just because the market is falling and this exacerbates the falls. At some point that ends and the reverse happens and punters rush in so as not to miss the rally. Chart looking like its trying to make a bowly bottom possibly.

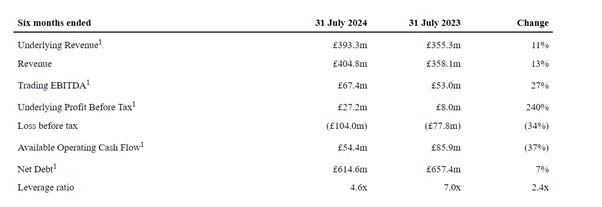

Having highlighted the bowl on SAGA two weeks ago and the news since that SAGA were in talks with Aegas, the European insurers, it was nice to see Saga’s results and the update on talks today.

Greatly improved numbers across the board. The outlook statement sounded rather positive, they have a new CEO who has earned his wings from what he has done there so far, taking them towards a capital light business model and the bowl on the chart gets better and better imo

Saga also published details of their negotiations with Aegas:

The full results and the full negotiation statement are available to read on RNS

On a PE of 4.7 falling to 3.3 it looks the perfect shunned recovery play imo and that’s where the multi-baggers and OBIAY stocks lie for me.

There’s high debt and leverage but as I have said many times, these are the things you have to live with with recovery plays, it’s the uncomfortable part, but if there’s a new board and they look like they know what they are doing then I’m prepared to give them a chance – you only need get one or two right while avoiding the bulk of the failures but that is if you are comfortable with recovery plays. I fully understand it isn’t for everyone and you need to know your own risk/reward profile. The shares hit 151p almost immediately on the Friday open, nearly 40% up on two weeks ago’s purchase. A lovely winning bowl. If the deal goes ahead, debt should fall dramatically, this could then pretty much become a cruise co and see a decent re-rating - let’s wait and see.

SAGA have a presentation on Monday (14th) with investormeetcompany at 9.30am

I share I have been buying is International Personal Finance, IPF

Highlights for me in the valuation are:

PE 7.8 falling to 6.4 and 8% less shares now than last year

12.6p eps in H1

Yield 7.5%

EPS was 30p+ in 2019 and while that fell during covid it is now back on the rise. Forecast to do 20.4p eps (Sharepad) this year they have actually said they are ahead “Expect full year pre-exceptional profit before tax of between £78m and £82m for 2024, ahead of current market expectations” Sharepad base their eps forecasts on £78.8m pbt so if they hit the top end they could do 21p+ eps. Add in now that they Are doing heavy share buy-backs and there are now 8% less shares in circulation than last year then 22p+ eps might not be fanciful. An interesting feature of the co is that they pay 33% of earnings in a H1 divi. If they do 22p eps then the H1 divi for the coming year will be nearly 5% in H1 alone.

Up 150% in less than 2 years there is strong momentum in the chart.

IPF looks an interesting, cheap stock imo. They are due a trading update in a fortnight.

There is a good write up on Stockopedia by Graham Neary if you are interested:

https://app.stockopedia.com/content/small-cap-value-report-wed-31-july-2024-ipf-mgmt-interview-rch-1003840?order=createdAt&sort=desc&mode=threaded

So that’s been the week here - the market is tough because many have sold or are selling to avoid tax changes in the budget. What this likely means is many punters have just sold without thought, which means there will likely be some real bargains to steal when news comes out or results. Plenty more 40 percents in a fortnight waiting to reveal themselves imo – what were in demand and soaring will likely in many cases roar away again in many cases imo.

Lastly, a bowl I will highlight that I have noticed:

Xaar, XAR – an old muli-bagger of mine from the Covid fall – no reason to highlight it other than a bowly bottom that is worth watching imo. I may be a buyer if the bowl gets going.

RR. closed the week at 537.2p - an all time high.

One last thought - why would any co’s release updates or news before the budget is out if they don’t have to? If they are going to get received with ambivalence before then they may as well wait till November - so it might be a monster month - fireworks are guaranteed :-)

Have a good weekend – winter draws on! 😊

Rebel

Who knows with CMCX or anything - Labour could do anything

Need to wait and see - likely investors banking profits wherever they have any at the moment.

well done, no bad idea