Weekend Rebel Review, March 2, 2024

The Spring Market - ready to burst into life?

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

The market has been slow yet again this week but if there’s one thing I have noticed is that the market firms off good news as it has always has done. As we go into March it’s a big month for news from individual companies but we also have some macro news due. If the inflation data beats I think we may actually start to see indexes firm a lot more sharply. Rolls Royce( RR.) results were received very positively and the shares have moved up 10% since with brokers D.Bank raising their target to 465p from 400p . The more results that come out and beat, the greater the read across to other businesses and drive the market higher. More bids on super premiums will help too.

In the US, the S&P has continued higher but this week saw a bit of a breather until Thursday, it then carried on up on the trend. Since the end of October the trendline has been easy to see:

The Vix has trended a tad higher but volatility has picked up somewhat on the Vix itself:

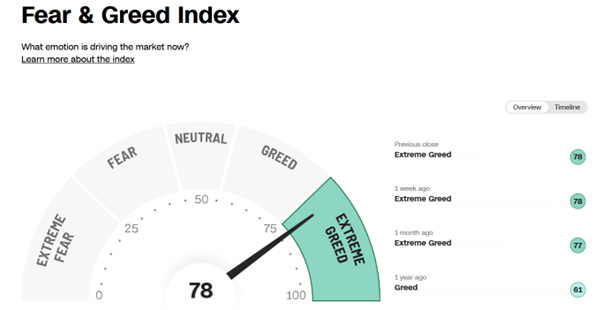

This is just indicative of the Middle East and other unrest and inflation not falling as fast and steeply as hoped for in the US imo. Fear/Greed has crept into extreme greed but reflective of the relentless rally in the US rather than the UK imo. The US may be due a bit of weakness soon. This looks like a pretty no thrills Vix to me but things can change quickly.

The Russell 2000 is just breaking out as I type – hopefully money moving from Fangs and Large caps as the market senses rate cuts ahead. That’s a big positive for UK Small Caps. While Aim still seems weak the FTSE Small Cap Index is actually trying to break a recent resistance. KIE has just got promotion, BMY a cracking trading update, WIN a 100% premium bid CMCX and AVON at 8 month highs, there’s a lot of fully listed Small Caps getting attention even if they are screaming cheap, while somewhat rarer to find on Aim. If company earnings keep increasing and interest rates fall, the market has to turn at some point, meanwhile just look for the shares that are bucking the trend imo.

The Russell 2000

The FTSE Small Cap Index

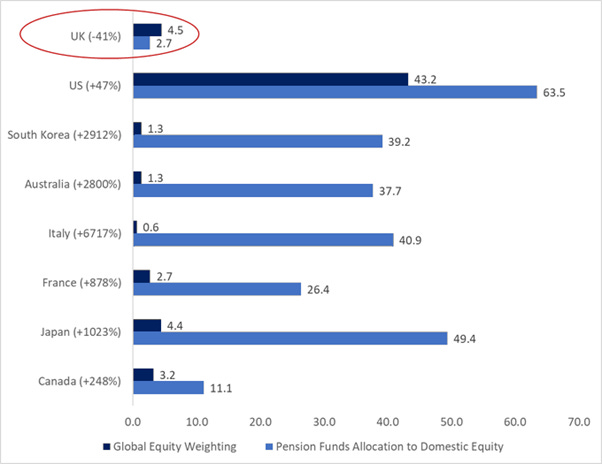

An interesting bit of data I saw this week, posted by Simon French was the absolute dire amount of investment in the UK by UK Pension funds. This is a big reason why the FTSE 250 has only risen 12% since October while the French CAC has risen 30% and the DAX 40%, all while the UK has outperformed both countries.

It can be frustrating doing research, finding very cheap shares but the market not responding to many of them. I’d say that UK valuations are the lowest I have seen them especially compared to prospects. On Friday the Nationwide House Price index rose 0.7 year on year. We’ve had 5 yoy rises in a row.

Other GDP data has been better than expected for manufacturing and services, far better than Europe. When the big investors stop running scared then there is likely to be a rush back into UK stocks so I’m staying well invested and plan to be ahead of the crowd,

Tuesday saw McBride (MCB) post full year results and an immediate near 20% rally in the share price, the first of many imo. After posting 9p adjusted eps in H1 alone. 19p forecast eps for the year means that even after that 20% rally in the share price, the PE for this year is just 4.5. Even going on 7p basic eps in H1 the PE can only be around 6.5. They have high debt but this fell in H1 by circa £24m to £145m, similar to the mkt cap. So if they can keep bringing the debt down the PE may likely rise more sharply. Risk or a likelihood of a dilutive fundraise is keeping it cheap and looks very likely imo. If they raised half the market cap here in cash that would double the shares in issue. An interesting situation to just watch for now perhaps, they would like to raise with the stock higher I’m sure.

Having bought HFD the previous week on the small bowl and seeing it soar on massive volume late that week, I was all ready for an RNS to say they were ahead or there was a bid approach, then on Wednesday an RNS warning, downgrading profit forecasts massively. I took the hit and sold, pretty much a repeat of WOSG in Jan, clearly neither co has a handle on how they are trading short term.

Thursday saw a counter bid for Wincanton (WIN) a, cash offer at 605p from GXO Logistics, up from the 450p bid from CEVA. That triggered another 20% rise in the share price, a 100% premium to where they were trading in Jan, to underline just how cheap UK companies are in many cases. The shares were firmer still on Friday with buys going through at over 630p which suggests the market thinks another bid is coming . If pension funds are only looking abroad the UK will get cheaper and cheaper, until they suddenly wake up. Looks like another UK co will be leaving the LSE – UK fast becoming depleted of decent listed co’s.

On the same day, Kier Group (KIE) gained promotion to the FTSE250. With interim results this coming week on 7th, they should reinstate the divi too. This should attract interest from FTSE250 tracking funds and FTSE250 Income funds going forward imo. The shares are just breaking out to a 4 year high. Let’s see how good the results look – I hold – half way to one-bagging them after 7 months. Huge bowl and break out on the chart.

Bloomsbury (BMY) has continued to do well. With the year end on Thurs last week, 2 weeks after the trading update, there may be more in the pot for earnings, above what the co said for the year just ended. Sarah J Maas sold nearly 45k books in the first week of the launch. These are no longer a one-trick Harry Potter pony imo. The launch of Cixin Liu’s Three Body Problem series on Netflix in 3 weeks could be another major headline. After a pull back late last week, BMY trade at 10% above their high of 14 months ago and 50% above the low 14 months ago. Earnings will be double where they were then.

I find that cheap on historic earnings and believe earnings will reset to a higher level going fwd, especially with acquisitions, so I’ve increased my holding substantially. If you want to see the trailer for Cixin Liu’s Three Body Problem you can watch it here

https://www.netflix.com/tudum/articles/3-body-problem-teaser-release-date

Finally, having banked some profit in Rolls Royce (RR.) I have boosted M&S (MKS) further. Over excited turned to oversold here imo. Still making a bowl to bounce off the long term support line I feel.

Two months into the year and the portfolio not going as well as I hoped. Having taken a 3.3% hit in Jan from WOSG and a hit on Monday from HFD FOR 0.6%. , that hit the portfolio for nearly 4%. I sold HFD splitting my sale half in the opening auction and the rest in the day. Having taken those two hit’s the portfolio is still up over 1% year to date which I can’t moan about in this market – and I ought to be due a cracker of a winner to offset those two duds too I hope. The year is young.

That’s about it for this week’s action though I reduced LUCE a bit as it has been so weak. XPP and DIA reported weak trading but LUCE has better than those two so I doubt they are in the same cub but it seems sentiment is a bit weak. If it feels tough still then the good times will be a breeze. March is here so I expect to have a lot more of interest going forward and far more opportunities to show up.

Please remember these aren’t tips, they are just my thoughts on what I’ve bought and buying and the market. I will be biased, you cannot count on my objectivity in that case so do your own research into any stock that you might want to buy.

Have a good weekend.

Rebel

CR, Thank you for sharing your thoughts.

I bought McBride first in July 2022 adding throughout 2023 up to a max of 50p. I have not sold any and it is my largest holding. I think you are wrong on the need to fundraise. MCB did refinance on 29/09/2022 which cost "11% of any increase from the current market capitalisation". MCB terminated the 'Upside Sharing Fee' on 25/10/2023 for a cash settlement of £5m. This was beneficial to MCB once the share price hit 50p. The MCB board could of diluted in 2022 but avoided it.

SCSW "X" feed reported on 29/11/2023 "I've just never seen anything like it. Can't keep up, selling all we produce and we've have paid £24m+ off the debt since June,".

Since the all time MCB high in 2017 (£2+) the number of shares in circulation has fallen 5% due to an ill timed share buyback.

Forecast EBITDA for FY24 (06/24) is £83.65m verses the previous record of around £50m

IMO the MCB share price was well "managed" in 2023 but since the SCSW tip in December a short seller has been trying to move the price down.

MCB have a Capital Markets Day on 13 March

My own thoughts on MCB are on ADVFN, which will also no doubt be biased due to my holding.

You may also be interested in the long smooth bowls forming in LIO and SFOR