Weekend Rebel Review, June 7th, 2024

Results and updates kick off here.

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

Well another quiet old week but the more the punters get bored and trim, the greater the bounce on some of these results and news release/trading updates. The rest of June should be way busier for trading updates and results. Monday, like many Mondays and Fridays was low on news. It seems these days that directors and brokers are only in the office Tues to Thurs. Monday and Friday seem mostly earmarked for necessary but unimportant news these days, in the main. No real news but the FTSE closed at a new recent high on Wednesday.

Tuesday saw results from Gooch & Housego, GHH. The results looked weak but they hinted at being inline for the year and more confident. I had bought a few of these about a month or so ago, mainly due to them having a new CEO who should by now be delivering after 18 months in the job. I actually sold what I had bought recently because better stocks revealed themselves. The shares have risen and only gave back 27p on Tuesday which after the recent rally wasn’t too bad. I’d like to see more urgency in the recovery.

Wednesday was the third day in a row where the number of RNS were low and what was round hardly set the heart racing. Scottish television company STV , STVG posting a decent trading statement and showed why it has a fab bowl on the chart. ITV was a tad firmer off the news, interesting chart there too but I think there’s better places for my money elsewhere.

Thursday’s stand out was SPEC for me, This co seems as hot and cold as my toaster in the morning. I lost interest in these a year ago or so after buying into the big low. I made a profit but every time I read their update since then there is plenty of flies for the ointment lying around. Despite all the brands they seem to be commoditised plastic, competing with the far east. No big barriers to entry, paid way over the top for the German acquisition and punching out plastic frames and competing with China hardly seems a killer business in my opinion. 100% plastic more or less, I bet that’s not an attraction for funds thinking about ESG. You have to go back a way to find director buying. There are plenty of far better shares I can find. In a way, such a quiet day which was a blessing that let me watch the coverage of the D-Day commemorations – all these brave people from a different ‘snowflake-free’ unwoke era, and a far better time, other than the war. Very humbled by these ageing, brave men and women that just got on with it. When I lose a bit of cash I try to remember it’s just money and this was a salutary reminder.

Friday brought the end to a desperately dull, quiet week for shares. Next to no news as is often the case on a Friday.

Onto macro and I’ve been watching the shipping container prices, they are hitting new recent highs. Several things are going on imo. We don’t have Covid or Ukraine or any new issues in the Red Sea which drove prices higher in recent years. What we have, in my opinion, is retail and consumer co’s shipping more stuff in for fear of being low on stock for Christmas. We are also seeing businesses on-shoring and increasing automation which means greater industrial movements and shipping of parts and kit in my opinion. This bodes well for the whole market going forward and why stocks are firming I believe. On-shoring and automation has the scope to increase UK growth more than many give it credit for. I do think there’s stronger growth likely in manufacturing and it may be a mini renaissance for the sector as it reduces shipping and labour costs and adds reliability.

Drewry World Container Index.

The S&P made new highs this week, breaking through resistance which is positive for the macro.

The Russell 2000 hasn’t made new highs but it’s firming

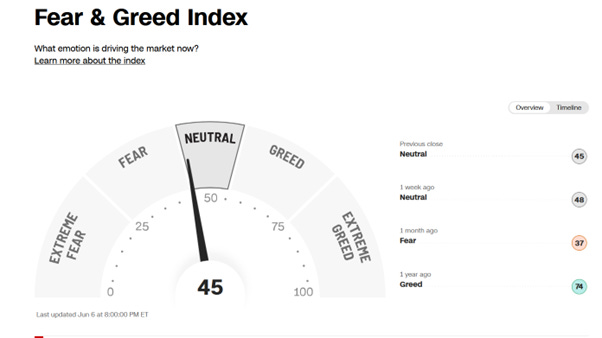

Fear-Greed is still at the low end of neutral so not a lot of exuberance in the market which is positive too

Of all the charts of the macro stuff in the US, the Dow Transport isn’t as firm as I’d like.

Copper is very firm, hitting all time highs here, very positive - a long time bull mkt indicator.

With a quiet week there’s not a lot to say re stocks, so I have highlighted stocks I’m watching for the rest of June that I hold.

June 15th, Warpaint London (W7l) trading update approx..

Last year, it was June 15th, it will be some time in June. The co is on a cracking roll and expanding in the US. The trading update with the results was very good with this outlook

“I am very pleased with the Group's strong performance in 2023 and that this has continued into 2024, with the Group having record first quarter sales. This reflects the delivery of Warpaint's consistent and focused strategy. This strategy is fully reviewed by the board annually and the board works closely with the executive directors and management to ensure that it is implemented. The key to our growth has been, and will continue to be, expanding our presence in large retailers globally, by growing our sales with existing customers, entering into relationships with new ones and increasing our online presence.

Notwithstanding the continuing volatile economic environment and challenges that face our customers, I am optimistic that the strong performance we have seen in 2022, 2023 and now into 2024 will continue and that we have the right offering and strategy in place to continue to deliver profitable future growth.”

Record sales in Q1, they are also building up inventory for a very strong H2 and have picked up Wallmart as a customer in the US too. 22p eps this year, 26p eps next year. A PE of 22, falling to 19 may not seem cheap but these are doing 50% eps growth per year compound.

This from Stockopedia:

June 20th: CMC Markets (CMCX), a spread betting trading and investing platform to trade shares and currencies. Final Results

On Jan 8th CMCX raised guidance for operating income of £290-£310m, from £250m-£280M – a 10 to 15% hike. Current eps forecasts for 2024 is for £55m pbt and14.6p eps. CMCX lost 0.8p in H1 so effectively they will have done 15.4p in H2 @ £55.8m pbt.

Since then the co has said it will achieve £21m cost savings from staff reductions which will add to 2025 pbt.

They have expanded into Singapore now and that acts as a gateway to Asia.

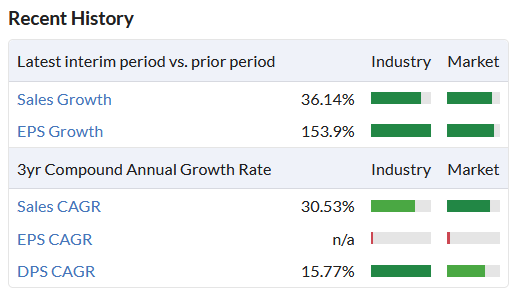

Here’s the H1 results slide showing what has changed up to H1 and what was going to happen in H2 just closed.

There is huge operational gearing with this company. In 2022, before doing a pile of investing, they were doing 24.5p eps on £252m sales. They have done £331m+ sales in 2024 and despite forecasts suggesting sales will be flat, they should do far more in 2025, there are now far more products and global stock markets have picked up.

15.4p eps in H2 2024, 17p eps forecast for the entire year 2025 going forward, including that £21m savings.

June 23rd, Filtronic (FTC) trading update approximately.

A recent trading update said this:

Low Earth Orbit Satellites are expanding rapidly and require RF communications. Filtronic is one of a vey companies that address this and have 40+ years of experience and a great reputation. Filtronic supplies RF based tech to telecoms, defence and satellite sector. Perhaps the Low Earth Orbit satellite business throws this company back out in the spotlight now it has won contracts with SpaceX. 2.7p is the new eps forecast for 2025 but how conservative is this and what’s the growth rate? They will do half that this year with a small 0.25p loss in H1 so H2 alone will have been around 1.5p eps. They have a new CEO, Nat Edington.

https://memuknews.com/business/appointments-personnel/filtronic-ushers-in-new-leadership-era-with-ceo-nat-edington/

They have been winning contracts a plenty recently for Elon Musk’s Low Earth orbit satellite co’s inc SpaceX and defence co QinetiQ. Sales at FTC have been around £16m each year for the past 5 years, this year it’s set to soar to £24.4m and next year £35.6m. Changes like this is what can transform a company’s future. The satellite business is much higher margin than the rest of the business. Being so small and so commanding in it’s field, where little other co’s like it exist to compete, it must be a bid target too imo. They opened up at near 50p on the SpaceX news, I‘ve been buying from when there has been a bit of a pull back to 54p. Although it once traded massively higher than this, here’s a post-techboom chart.

SpaceX has warrants for 10% of the co in return of guarantees of orders going forward. What I do like is that if this is a pivot into a much greater, higher margin sector then as a high growth small tech co there will be bags of room to re-rate and they have got this US interest. Rare for me to be in tech but the forecasts here are for Filtronic to double earnings year on year going forward into 2025 so if they start beating forecasts and re-rating there could be a big multiplier effect on the share price. Net cash and no dilution to speak of over the past 6 years or longer. I’m not sure what the eps could be in the coming year but I suspect it will be somewhat higher than current forecast and as a tech small cap with high growth of 100% p.a going forward then it could command a high PE as high growth tech does imo. It is pretty illiquid and small so everyone should do their research and know their risk here imo.

June 25th IG Design, (IGR) Christmas wrapping paper producer. Final Results.

On April 30th, IGR put out a trading update:

“The Group has continued to make good progress on its turnaround journey of improving operational efficiency and simplifying the business. These initiatives have resulted in significant growth in profit and margin for the year. The Group expects to deliver adjusted profit before tax of $25.9m (FY23: $9.2m), which is ahead of market expectations. The Group's adjusted operating profit margin is expected to be c3.8% which is a further recovery of 200 bps on the previous year.”

“Financial position

“The Group closed the year with a net cash balance of $95 million (FY23: $50m), a $45m year-on-year increase which is well ahead of market expectation. The Group was average cash positive for the year despite its traditional seasonal cycle of working capital movements. This improved cash position was driven by increased profitability and continued improvements in working capital management throughout the Group.

Moving forward, the cash position of the Group is expected to continue strengthening due to its financial performance and sale of freehold sites following footprint consolidation in the DG Americas division.

The Group expects to make a provision of c$5.5m* for potential liabilities relating to pre-acquisition era duties owed in the DG Americas division and is taking legal advice on the matter. Due to the historic nature of this issue, the results for the year ended 31 March 2024 will be adjusted accordingly”.

These were some of the highlights. The full trading update contained far more and worth reading. The response to the trading update was an immediate 35% rise at the open. A further rise since means they have nearly doubled since the trading update in a month.

Prior to the trading update, 10c was the forecast eps. The consensus has since risen to 13c. Canacord are forecasting upward of 15c, this compares to a tiny loss last year. 2025 eps forecasts haven’t been adjusted despite sales forecast to rise around 3% and operating margins expected to grow to 4.5% by the end of 2025, from 3.8% this year.

Although there’s 30% more shares than in 2018, the 26c dilute eps achieved then will likely be near hit again this year adding those extra sale and greater margins imo

I’m looking forward to hearing what the company says.

26th June, Liontrust (LIO) Asset Management full year results Liontrust is an investment for me based on very simple reasons. The chart is one huge bowl. The yield is over 8% and looks sustainable. Stockmarkets are picking up, especially small caps where Liontrust play. As the net assets rise the discount to asset that all these types of companies have, starts to reduce too – giving the shares an extra push. Not many of these co’s pay an 8% yield though. The CFO bought £55k worth in Jan. I’d say this is more risky for me as I rarely invest in this type of company and don’t fully understand the structure and fees. So it’s more a punt on the bowl rather than an investment. Higher risk, definitely do your research. Quite a big pull back recently when D.Bank said sell.

Not so sure about the virtue signalling in the logo.

I did an interview on Vox Live on Friday with Paul Hill, a lot of the stocks I hold were covered, if you are interested:

So that was my week and what I see ahead. Obviously I hold these shares and am talking my own book. I may be biased, in fact I guarantee I am. So know your risk profile and do your research rather than relying on anything I say please.

Have a great weekend.

Cockney

Twitter: @rebelHQ

Thank you Gareth

Thanks Stephen