Weekend Rebel Review

KWS, HL, AVON, GNC, IGR, MKS, W7L, ZTF, MPAC, BMY

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

A very busy week with lots of the 16 or so co’s I hold, coming out with results and news. It has been a great May so far and Monday kicked off firmly. Keyword Studios, KWS announced a bid approach that they were minded to accept, if a formal offer was put fwd. The shares soared £9 or 60% to a little below the indicative possible offer price of 2,550p. Looks like yet another UK co getting taken out and clearly has been trading too cheaply. I had noticed the bowl forming in recent days but reluctance to increase my holdings numbers I had ignored it ☹

Tuesday was Groundhog day – a potential bid for XPP at a 68% premium from Advanced Energy. Will there be any UK companies left? Well at last this one had read across to stocks like LUCE which I hold and makes them look very cheap imo.

After two days where the FTSE250 went nowhere, it was time for the UK inflation data on Wednesday and CPI came in at 2.3%. Not the 2.1% the market was forecasting but way down from the 3.2% last month. Of course, UK Indexes were muted on the news. The FTSE250 down half a percent at the open – really? The UK is growing faster than most countries in the EU, inflation is now below or in line with the major EU countries and that is the reaction! Well there’s some seriously depressed investors out there imo, but then perhaps that’s why they are missing stuff like IGR one-bag in a month. With inflation at 2.3% and growth picking up, is it so bad to have rates on hold? Loads of co’s reporting great performance and bouncing big or being taken over because the mkt has been ignoring them. All of this was fading from the mind when in the afternoon Rishui Sunak announced he’d go to the country for an election on July 4th. The bad news is we are going to get sick to death of politics. The good news is that unless we have a hung parliament we will at least have an end to some uncertainty which markets like.

Wednesday night closed with a rejected 985p bid for Hargreaves Lansdown HL. Yet another UK co lines up to get taken out. How long till the market actually re-rates on all these bids? AJ Bell, AJB rose higher strongly on good trading and along with the HL. Bid approach, that sent CMCX to a new recent high.

Fer/Greed is back to neutral which is good for buying:

The Russell 2000 has failed to make a new high, so may need this pull back to take a run up and break out imo.

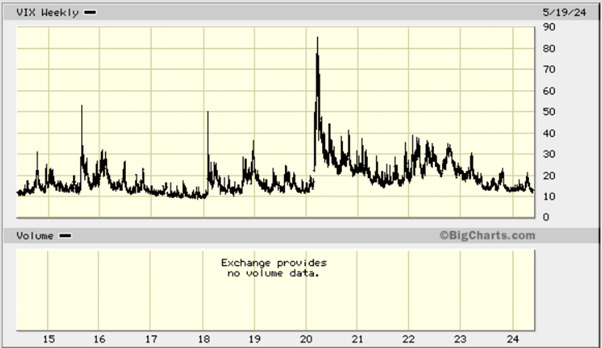

The VIX is down to 12.6 – that’s back to pre-covid levels – here’s a 10 year chart – back to normality

Copper is testing long term highs, a break out of this line would be very bullish imo

All in all, the pilot dials for investing all look very much on autopilot.

Shipping rates have risen strongly again this week. As it doesn’t seem to be Red Sea or Israel/Palestine driving it, I am inclined to believe it is growing global demand and China getting its act together a bit, especially with the copper price so firm too imo

On to the stocks I hold or which I am closely interested in:

Tuesday saw Avon Protection, AVON, a much commented stock here on my Substack and large holding for me, post excellent results:

All of the details are in the results to read but a few of the highlights were :

“Record $199m order book”

“23% productivity improvement6 vs H1 2023”

“Confident in the outlook for H2, issuing updated FY 2024 guidance”

“Revenue growth c.10%”

“Adjusted operating profit margin 10%”

“Cash conversion over 100%”

Jos Sclater CEO and Rich Cashin CFO have done an excellent job since taking the helm. Going forward they have a record order book of $199m and are suggesting 10% revenue growth and a rise to 10% operating margins. They have increased guidance.

In 2019. sales were $164m, operating margins 7.71%, returning eps of 109c.This year sales are set to be $276m sales on near 10% margins. $275m sales this year will be 25% above 2018. Operating margins then were 13.1%. Jos Sclater says they are targeting operating margins of 14-16%.

Here is the historic chart, there has been no share dilution:

I’m closing in on one-bagging these now for my initial buys in November and will likely continue holding for a lot more. If anyone wants an overview of the company, there’s one in my Jan 26th Substack here:

https://cockneyrebel.substack.com/p/avon-protection-plc-avon-f35

I think once traders are out and long term investors start accumulation then Avon will firm even more and has a very niche growing ‘pure defence’ product (ie not an offensive product maker) they are even more attractive to those wanting defence exposure in these times. Will they stay independent? The last two co’s Sclater and Cashin were involved with both got taken over and I expect Avon will attract a bid from a US defence co before too long, now the business has been cleaned up, in my opinion. The shares rose 4% after reaching an 18 month high last week, has nearly one bagged for my early buys and has risen 50% since the start of the year.

Based in Ireland, Greencore business is in the UK. Greencore make food for supermarkets like soups and sandwiches and have a huge dedicated factory for MKS in Northampton. The soup factory that has struggled making profits is closing. They have two factories near by which make quiche and from September they will be making ready meals for Aldi there.

Lot’s of impressive numbers there but I thought the 2.8p adjusted eps wasn’t as exciting enough at first glance, with the forecasts for the year being 9.4p. However, going fwd that should be something like 8.8p+ eps in H2 which annualised would be impressive growth going forward. Brokers have upgraded eps this year to 10.2p and 11.6p next year, which seems pretty conservative imo. Importantly if brokers are upgrading here, then they seem convinced H2 will be even stronger imo. The co has ditched a lot of low margin business which will help over all margins going fwd. Earnings in the past don’t seem to have been weighted to H1 or H2 as a trend. Also, the trailing 12 months eps is already 12p, so beating that after doing 2.3p eps more than last H1 means any growth in H2 adds to the 12p trailing 12 months. The forecasts for the year are less than the trailing 12 months.

Dalton Philips was appointed CEO in May 2022 and Catherine Gubbins CFO in Sept 2023 – I like new boards that really start delivering 12-18 months after taking the helm.

The company has a pension deficit of £20m+ but by Sept 2025 that will free up £10m of cash per year once fully paid. They say they are giving £50m back to shareholders in the coming 12 months, £30m in buy backs and a divi going forward if trading carries on well. There’s an interesting story in the press today re Greencore and M&S which looks like it will help. M&S are upping the quality of a number of food lines which likely means better margins for Greencore as they will be higher margin quality products.

This is one stonker of a curve up on the chart too imo

The shares rose 15%+ on the day which was better than I expected on reading the results initially, as often investors and traders have been muted on this stock’s results. Directors have been buying though, and activist investors have been agitating so I suspect this stock is now on a steep up-trend, especially based on what H2 will do. Shore raised their H1 guidance by 5% today but that looks cautious imo. The next trading update is in July, the co says it’s now guiding £86-£88m op profit compared to the £82.9m consensus. Net debt falling to 1.4 times, and reduced shares will boost diluted eps. The divi forecast for this year is 1.86p, and nearly doubling next year – this year’s divi 5 times covered and more. The shares have continued trading around that high.

IG Design, IGR, has nearly one-bagged in a month after its April 30 trading update, rising from around 120p to rally to 230p. Interestingly, Fidelity doubled their holdings on Tuesday from 5% to 10%. Results are due in a month’s time. Forecasts have risen from 8.2p to 10.2p for this year closed, just in the last month, 18p for the coming year. With the shares staning at 210p that’s a pe or circa 12, for near 80% eps growth going fwd this year.

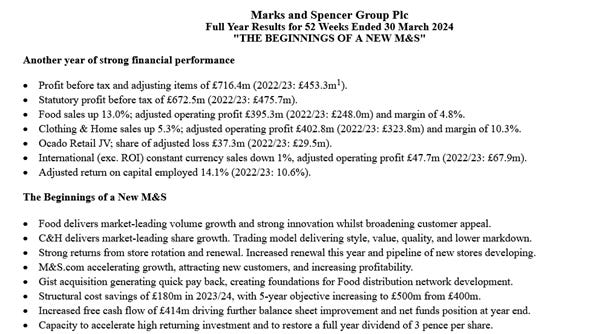

Wednesday saw results from MKS and what results they were!

Pre-tax profit up 41% to £425m

Adjusted basic EPS up 45.6% to 24.6p

Final divi of 2p making 3p for the year.

Net cash ex leases of £45.m, from £3.55.6m net debt

These weren’t just any results, they were M&S full blooded turn around results.

Listen in to the webcast, I’m sure the press will be all over them at the weekend too. I was more than happy with the results and so was the market – the shares rose nearly 10% in the opening 30 mins, they closed the week just short of a 5 year high.

M&S only made up 5% of my portfolio now, but they aren’t going to one bag in a year. I think I can find faster growing shares so while I think there’s a lot more in them I have sold to put the money to work potential one-baggers lower down the food chain.

Warpaint London’ W7L announced a listing in the US.

No more share will be issued, this just opens up Warpaint to the US and shines a light on the company over the pond. Ultimately I believe a large US cosmetic co will take them out and they don’t mess about when it comes to paying premiums to buy growth imo.

Zotefoam posted a trading update which was rather positive. There are numbers in the update but this was the outlook:

A recent acquisition for me and I’m still researching more but I very much like what I have bought. Well worth reading the full update – ZTF rose on the news despite being on a recent high. ZTF board were on Investormeetcompany on Wednesday, it is well worth listening to. Not only will ReZorce be great for recycling as all one material, it will also be good for heating contents up in a microwave, something you can’t do with the foil in current products. It will also allow the holding of oils like olive oil. They said trading is strong and they trading inline but I suspect they are a tad ahead. I added a few more.

MPAC, on Wednesday, announced battery unit cell production had been completed at their trial at Freyer.

This is an important milestone and moves them onto the next automation stages towards a complete automated production like. None of this Freyr work is priced into the forecasts. I don’t know if there’s any milestone payment they receive for this achievement but it’s a big step in what could be a very lucrative run of automated production lines for Freyr and potentially other battery production lines across the pond and in Europe. Te shares rose to a new recent high, still far too cheap imo.

So onto Thursday and that saw Bloomsbury Publishing, BMY published results – all very good numbers imo

“The stifler was in the forward looking statement tho:

Trading for 2024/25 is expected to be slightly ahead of current consensus expectation1. Expectations for 2024/25 reflect the exceptional performance in 2023/24, and that we are not expecting to publish a new Sarah J. Maas title in the year ending 28 February 2025. Last week, we won five awards at the British Book Awards including Children's Publisher of the Year. Today we launch Bloomsbury 2030, setting out our vision for the Company over the next six years.”

So while they expect trading to be ahead it’s only ahead of the forecasts for 2024/25 by a little and those forecasts are well short of lower forecast for the year just ended. Disappointing that there’s no book from Sarah J Maas this year nothing much re Liu Cixin’s “Three Body Problem” being serialised on Netflix so I presume that’s been a duffer.

However, Cash up circa 30% @ £65.8m and a higher divi by 25%, a great balance sheet and an excellent long term track record. Traders dived out at the open along with some investors I guess. Not looking anything like a one-bagger in 12 months though, so I reduced my holding later in the morning, following the crowd and will gradually sell the rest into strength over the coming days. That’s the way a few go at times, no over all loss but probably could have used the money better with hindsight. I will put the cash into my other existing holdings.

Rolls Royce had their AGM and an upbeat trading update on Thursday.

Tuffan tends to under promise and over deliver – even if his promises are usually big promises:

“Our full year 2024 guidance is unchanged, with a broadly balanced weighting for both profit and cash flow across the year”

“In Civil Aerospace, long-term service agreement large engine flying hours (EFH) have returned to 100% of 2019 levels in the four months to 30 April, driven by the continued recovery of international traffic in Asia and our growing fleet. For the full year, our expectations of large EFH at 100%-110% of 2019 levels”

“In Defence, the long-term growth of the business has been underpinned by several recent contract awards. Australian funding was confirmed for the AUKUS submarine programmes, which includes Rolls-Royce reactors.”

These were just some of the highlights, it’s worth reading the full statement. If the market was the judge then the 3% rise to hit the all time high of 10 years ago said it for me.

So that’s what my week has been about. A very firm turnaround on Friday - FTSE250 was off nearly half a percent in the morning to close up 0.6% by the close - market getting ever more bullish. Remember, I am no analyst, I’m a private investor just diarising my week out of interest. Know your own risk profile, do your research thoroughly because the buying and selling is all down to you.

Have a great extended weekend and I’m looking forward to the markets getting firmer and firmer as FOMO gets into the hearts of those just watching.

Rebel

Thank you Gary.

I did the same when I started and it took me time to hone what I do. But constantly back testing and focusing on what woks and what doesn't has helped me improve massively. I still do the odd daft thing but I've learned that what initially looks boring is often 'very exciting about to happen', and what often looks very exciting has more than that built intro the price and can often only disappoint.

Learning the mistakes is the key, as you have done - some people never learn. I know of at least two that have made £5m being a bit lucky and then given it all back - you rarely hit a lucky jackpot twice.

When I bought my first 8 bagger, Hornby, at just 140p, everyone said 'what, the old model trains?' while everyone ignored it. 3 years later no end of press and tipsters were saying buy Hornby at £10+ and saying it was thee most exciting consumer stock.

Boring is good - if it initially sounds uninteresting to you, it likely sounds uninteresting to everyone else - that's when it's cheap. You just have to catch them as the story is changing.

Good luck and well done

Richard

Hi Stephen

Reluctantly I have sold AT. I'm not sure it can double in a year from here as much as some others can, being on such a high.

MPAC I do think can double over 12 months. Adam Holland is targeting doubling earnings in 3 years but that doesn't take into account Freyr. Also, there's a lot of re-shoring going on and companies need to automate and increase speeds. For that reason I think Holland's targets are perhaps quite conservative. The pension deficit looks like being resolved within 2 years too and that will boost for cash. I also think they are a likely bid target, especially once Freyr is a goer, likely to be a target for the likes of Melrose. Next trading update early July.