Weekend Rebel Review, 24th August, 2024

Bank holiday edition

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

I omitted to mention Synthomer SYNT last week after the interims. There were lots of happier stuff in the results but I struggled to get over the leader headine “H1 trading in line with expectations, with revenue, earnings and underlying EPS progression”

Underlying EPS progression sort of got my goat a bit. The shares are trading in the 230p range. From an underlying EPS loss of 35p last year, it is a progression of sorts, but these were trading at 160p when they took off in March with forecasts of 6p eps, now they are 230p with forecasts of -0.6p. Walking your forecasts down with the brokers then exclaiming you are beating expectations is disingenuous imo. I thought Wilome was better than that. I had sold out in my dash for cash a few weeks ago but there was nothing in there to say these were an OBIAY so I’m in no rush to buy back. There may be a time but not yet for me. Quite disappointing because having watched presentations from the co and read all that they had said, this never lived up to what they had guided imo.

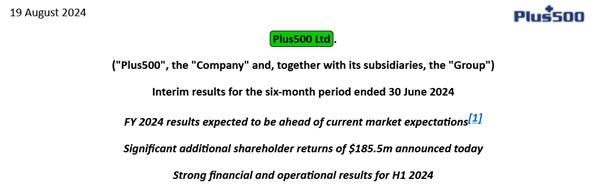

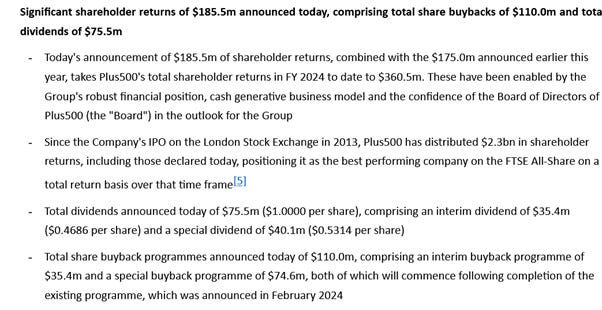

Plus500, PLUS put out a very positive trading update on Monday

The full RNS is there to read but basically they have done 190 cents earnings in H1. For the full year PLUS say “For FY 2024, the Board expects Plus500's performance to be ahead of current market expectations”

313c eps were the current forecasts so with 190c in H1 they need just 123c in H2 to meet this year’s forecasts. With half the market cap in net cash, they are paying out a lot of cash to shareholders, nearly 10% of the market cap:

On a PE of 10, falling to 9 and the co saying they are ahead, a 10% return of cash to share-holders, with a divi likely in H2 as well to add to that, then there’s a lot of return coming here.

With good read across to the likes of CMC Markets, CMCX who are rapidly becoming more a fintech co and who have constantly beaten forecasts lately and who say they will pay out half net income in divis, I’m very much looking forward to their trading update in early September. I am biased of course, this is my biggest holding having increased recently but I’d sooner add more CMCX than buy PLUS as the potential looks far greater and there’s the promise of half the earnings being paid in divis as they have suggested.

The RNS News service is rapidly becoming a joke in my opinion. For a long time now, news on a Friday has mainly been irrelevant tosh or a quiet time to bury some poor Aim results. Brokers and analysts for a log time, seem to have been bunking off on a Friday. After Covid and the surge of working from home, the 3 day office has emerged and Mondays are just an extension to the weekend for many directors so we get little to no news on a Monday. Of the three days in-between, it seems company’s all want to release on a Thursday if they can, it’s like some PR thing or the day analysts regard as the end of the week so they can finish with a bang. This is especially worse in the summer with holidays and such. It’s hard trying to cobble together a review of pretty much nothing through the week sometimes, even Thursday RNS were few this week and Friday wasn’t even worth getting out of bed for, with a bank holiday upon us the boards, the brokers and the analysts must be already on their holidays. This does mean there will be some pretty manic days mid week in September.

Over the past two weeks I’ve increased CMCX and CAR back to the highs that I was holding. I have had some FCH back lower than where I sold but not as many as I once had, I don’t really want to buy much else back yet. US data and UK data were better than I feared but with Israel and the budget still yet to be resolved I’m staying way above 60% cash. I am focusing on a smaller number of stocks. I have bought small stake in one new stock though.

I mentioned this recovery play on Twitter this week - Marston’s are a pub co. They have racked up a lot of debt over time but they also have a lot of fixed assets. They currently trade on a PE of 6.7 falling to 5.5 for the year starting in just a month’s time on Oct 1st. Trading seems to be improving nicely seeing they did 5.1p eps last year and H1 this year they are 0.4p up on last year With H2 accounting for a 33% / 66% split in earnings then the 6.14p eps earnings forecasts for the year coming to a close in 4 weeks time looks doable imo, as margins have also been improving. They have a new Chairman and a new CEO, formerly chief strategy officer of from Merlin Entertainment for 12 years, Justin Platt. He arrived in November he has been in the seat for nine months. This is the length of time in which I like to see tangible results coming through in a recovery play and the recent updates have sounded more upbeat. They have just disposed of their 40% stake in Carlsberg for £206m in cash and I like to see big things starting to happen which makes this a ‘pure pub play’ rather than part brewery, in turn making them a more attractive bid target also imo.

There has been just 10% share dilution from that 170p high on the chart, making the previous high roughly 160p in new money.

I have seen some big transformations in the past in this sector for Enterprise Inns and Green King so I wonder what could happen here. I also notice that last months the number of clubs and bars in the UK rose for the first time in a number of years which is a positive along with the fact that local pub growth is up 7.4% over the past year. Having sold the Carlsberg stake it becomes a pure play pub-oriented business and the business assets become clearly the pubs and property, which makes them more a potential bid target. Justin Platt has said the future is a successful pub business in his view. He seems to know that giving customers a good time is what matters, he comes from an industry that does just that and pubs need to be the focus, and that, as we all know, is what we want when we go in a pub or restaurant. In view of what I have posted above, and with the chart making a clear upturn and bowl, and two decent director buys recently, I think I want to back this new CEO for a bit and see if he is the real deal like he seems he could be. Obviously do your own research and don’t follow me, there should be a trading update in early October.

Filtronic has had a good week - there has been a couple of interesting tweets from the company in recent days. This from this week on Twitter:

This from 10 days ago

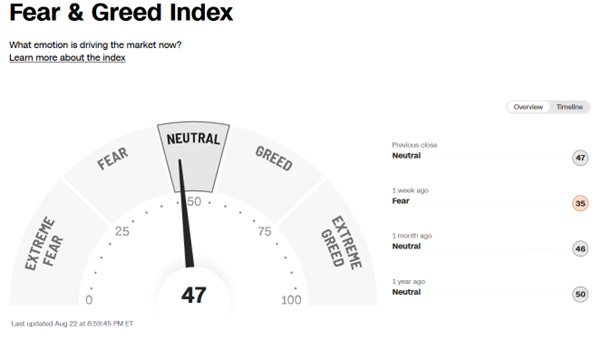

That’s about it this week, I won’t try to say anything when there is nothing to say. Fear/Greed is back into neutral. Where does it go? Back into fear if the middle east kicks off or up into greed if there is some peace agreement imo. Meanwhile we have to wait till October to see what this government is going to do in the budget, so we will be in more limbo than other countries till then imo.

Have a good weekend.

Cockney Rebel.

Arsenal - tho I've not really had much interest in football over the past 10 years, it isn't the same, teams are now just fronts for a huge money machine now. I know it has been ever increasingly that way but now it's ruined the game for me. Bungs, clubs being docked points at no set rules/timescale, VAR, taking the knee, players kissing the badge this week and wanting a transfer next week........I'm a grumpy old man getting my entertainment elsewhere most of the time these days :-)

I think car dealerships are a different kettle of fish. Enterprise Inns and Green King sold off large amounts of their estate on an individual basis to locals who want to run the pubs themselves. My village pub was one of them. Many pubs were sold at well over book value. If you sell off the toughest pubs to the locals and keep your most profitable then value builds. In 2018 MARS were doing 14p eps, the same amount of shares in issue still and debt will be lower this year than then too. They were trading at circa 120p back then.