The Weekend Rebel Review, June 7, 2025

IGR, KIER, PEBB, CMCX, FTC, WRKS, COA, SAGA, TUNE, WPS

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

Expect some spelling mistakes – I’m dyslexic and in a rush to get this out on a Friday so a bit of a task at times.

A dull week for macro stuff up until Thursday, when Musk and Trump’s love-in fell to pieces spectacularly. When a marriage comes to an end it is often nasty, but in the end, most couples start to behave on a more friendly footing, if only for the sake of the children. Trump noise is something we are all getting used to. Trump and Musk had a symbiotic relationship, they need each other or need to leave each other alone. I really don’t have time for spoilt brats so this week, I’ll leave the macro alone and get onto the real business.

One nice chart to see this week is the FTSE All World (AW01). This is a big macro watching chart for me, and what caused me to sell up and dash to cash in February ahead of Trump’s Tariff Fest. The big rolling top has now fully recovered and broken out this week:

Fear/Greed is at 60, roughly the same as a week ago

Aim has continued to break through resistance levels on the chart in pretty much a relentless rally.

On to Stock

IG Design, (IGR) posted this news on late Friday, after last week’s review was done:

You can read the rest where you read your RNS.

I have covered this co several times, held it, made great money on it, lost big money on it and listened to the director bullshot for far too long. I don’t believe the board know what they are doing and are just blagging it. They have sold off DG Americas but the real news to read is that this year’s results will miss again and results will be delayed, That’s $300m sales gone, and back to way before 2019 when they were doing $588m. Looks like they will do $430m sales now. Paul Bal, CEO has had 3 years to turn this co around. 18 months is my normal target to see tangible results. The shares were still below where they were when he took charge. The directors have bought next to no shares at all. The credibility is shot.

I want to see a new CEO, one that comes in and puts his hand in his pocket and buys, an experienced turn around guy/gal. Till then it’s just like a bar of Fry’s Turkish Delight, full of promise, but sadly no delivery yet. Who is going to believe jam tomorrow yet again? This year’s earnings have been chopped on the promise of higher earnings next year. And if they miss that again? There are plenty of better boards running better businesses for my money.

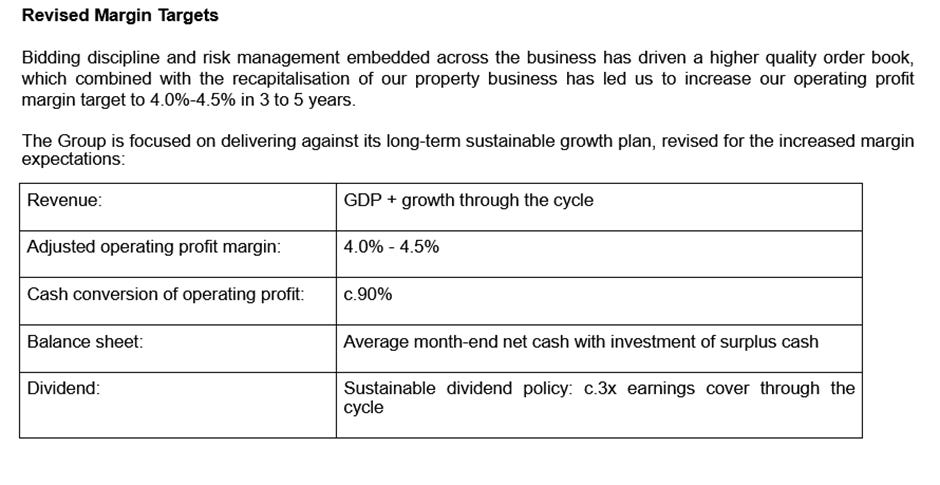

Kier Group (KIE) which I have been holding from around 80p (apart from a couple of short interludes when I traded out and back in), released their trading update on Tuesday:

All of which looks very positive imo. A PE of 7.9, a 4% yield. Net debt has fallen from £500m in 2020 to just £5m last year. It’s a positive statement. Kier raises its operating profit margin target over three-to-five years time to between 4.0% and 4.5%. The target previously was 3.5%. That says to me margins will likely be ahead of forecasts this year. The number of shares in issue will fall this year, as first for Kier as long as I can remember. Andrew Davies has done an excellent job here and the share price doesn’t yet reflect that in my opinion. I’ll also be surprised if there are not significant upgrades going forward as the sector seems to be seeing plenty of demand.

I hold so I would say that – do your own research as always.

The chart has broken out to 6 year highs:

Pebble Group (PEBB)

I mentioned these a week ago “Net cash of over £9m, pay a divi of around 5%. Sales have risen 50% since 2020. EPS has grown from 2.2p to 3.82p in that time.

In April, Dir Christopher Lee (Hammer House of Horror 😊)bought 270lk @ 37p and Stuart Wariner bought 105k @ 38.99p

The company is currently buying back up to up to £4.36m shares, circa 8%. I still need to do more research before buying heavy but I’ve bought a small amount as I like what looks like the left hand side of a bowl forming on the chart.”

They also said this:

I thought that bearing in mind they were trading so reasonably cheaply and now they are going to return a further £6.5m to shareholders then the £10m+ reduction in shares from buy backs and the tender this year made them look even more of a bargain, in view of trading being in-line. Possibly worth looking at as the chart seems to be bottoming but do your own research as ever.

Has made a big spike up off a curved bottom imo. I am still in the throws of researching these more to decide whether to hold or add more but have too many shares as it is (25) that need rationalising – there are just too many bargains about though.

CMC Markets (CMCX posted full year results on Thursday

You can read the rest where you read your RNS

As impressive as 35% eps growth might be in the headline, the PBT and eps fell short of what brokers were expecting by around 10%. The shares took a 17% knee in the crown jewels at the open.

Peter Cruddas, Exec Chair, never lacks confidence but this is way off what they were guiding a year ago when the shares were 2 bagging in no time. A 37% rise in the divi to 11.4p couldn’t consol traders nor the broker verbiage from RBC:

RBC RAISES CMC MARKETS PRICE TARGET TO 380 (350) PENCE - 'OUTPERFORM'

Fortunately I sold about 60% early in the week but that still left enough for a good punishment beating. Oh well, I needed to reduce my holdings and sold the remainder into the midday rally. Time to move on and increase some existing holdings. It is a constant battle to keep my holdings levels down to below 20, ideally I’d like to be holding just a dozen. Unfortunately, as you go down the food chain to small caps, it is hard to hold the really big 25% positions in things on Aim, like you can with MKS and RR. etc. Small caps have to grow in my portfolio to get to those sizes. Seems to be far greater undervaluation and the chance for co’s to beat expectations in small caps here imo.

I think in view of AJ Bell and Plus500 doing so well and CMCX missing, that doesn’t look like a high performer so time to move on for me. I sold the last of mine into the intraday firmness.

The Trump/Musk spat hit Tesla hard on Thurs so punters all run scared and dump anything Musk related on Friday morning. “Sell in haste, repent at your leisure” they say. It’s rarely a great time to dump your shares when everybody else is panicking. As I see it, RF and mmWave are fundamental to US and European space exploration and exploitation now. You can’t just hop to a different tech.

Trump and Musk had a symbiotic relationship, they need each other imo. They will need to both draw back but at the moment, noises like this likely creates buying opportunities rather than selling points in my opinion. One bit of positive news and those that were selling today will likely be buying back. There was some very large buys going on in the week which drove FTC to new recent highs. FTC gave back over 24p first thing on Friday, then it recovered to just off 6p – the heavy buyer this week has had a right result getting stock this cheaply I bet.

A word for The Works (WRKS). Covered for the first time in my May 17th Substack of just 3 weeks ago, re my 4 most exciting small caps . it just about one-bagged my earliest buys for me in 5 weeks when it hit 50p this week. No inclination to sell any, in fact I bought more this week. That may be foolish holding such a large position in such an illiquid stock but with the shares back to 44.8p to buy that is a PE of just 6.6 still. Also, Kelso, Mike Burn, Graeme Coulthard and Hudson Management have all bought 37% of the company recently. It’s my opinion they will not be selling shares into the market at any time as it will prove impossible with the illiquidity in anything but several years. These are smart city guys who know what they are doing – they will already have an exit strategy, such as selling the business to a larger entity at a price that will have made their hard work and risk worthwhile. That’s my opinion and I am holding for a lot more. Obviously I know my own risk/reward appetite and everyone is different, so do your research and know what you are buying imo. I could be completely deluded.

I should add in balance, WJG hasn’t hit the high notes, one of the other 4 small caps, but I think government building development legislation and new rules have slowed development progress rate. Rachael talks the talk but behinds the scenes they are doing damage to construction. If property doesn’t sell this year it likely adds to next year. Brokers have erred on a more cautious forecast but taken as a whole the business looks cheap to me. You can hear WJG comments on their investormeetcompany presentation here.

https://www.investormeetcompany.com/meetings/investor-presentation-864

One company that caught my eye recently and again this week was Coats Plc. Those as old as me will remember it as Coats Viyella. These are a developer and manufacturer of clothing material for apparel, footwear and performance materials such as tyre materials.

Several things about the company interest me. Firstly they said this in the March results:

“UK pension de-risking - c.£1.3 billion buy-in delivered in September 2024; now 100% of benefits payable from the scheme insured following a cash payment of £100 million in September 2024; no further cash contributions required”.

That to me is a big positive going forward.

In the past year they have had a new CEO and CFO which is often a catalyst to step changes in performance too. There has also been strong dir buying and a number of director buys including 600k by the new CEO between 75p-97p approx.

The shares took a hit from the tariff announcements but in the recent trading update they said this:

The shares are cheaper than they were 20 years ago.

This is a business that has always looked like it has huge potential. It got hit bad with the financial crisis and with Covid but after Covid rose 200% to 105p. Tariffs have been the latest hit when the trend was curving up strongly and I thought the recent update sounded confident.

Coats is one of those businesses that has huge potential but has never achieved it in my opinion. A PE of 9.5 and a 3%+ yield. With the recent trading update, the new board, directors buying, the pension off their back and sentiment turning more positive, I think these might be an interesting one to watch.

Do your research obviously, I can easily be wrong.

Bowls to watch

Saga (SAGA) – good director buying, have done a deal with their insurance arm that should bear fruit going forward, and cruises seem to be doing great and appealing to much younger people now too.

There is a long shallow bowl on the chart:

W.A.G Payment Solutions (WPS). Good cash generation but my interest is purely the chart

Focusrite (TUNE) – a much more positive trading update from these recently, with inventories seemingly getting back to normal:

So that ends this week’s review. Hopefully a lot more to talk about next week.

Have a good weekend

Rebel.

Twitter: @rebelHQ

Thanks Richard. Friday doesn’t feel like Friday without the astute observations on the psychology of the markets, the acute charting observations and the attention to novel share ideas.

Thanks Richard, really enjoyed reading your thoughts. You are right, so hard to prioritise what to invest in with so many bargains. It feels like we are moving into a ( short term? ) phase where some investors are tending to hold on rather than take fast profits and bring the price back down. Christie Group is a good example of late.