The Weekend Rebel Review 21st October 2023

AVON, MPAC, AT.

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required. Well the rain has killed any hope of doing anything meaningful outside today so time for a weekend review again this week. There’s a fabulous feeling about the market currently imo, although many may not feel it. When investors/traders sell off just because they cannot take anymore, when they just want ‘pain relief’ or 5% guaranteed from gilts looks attractive compared to fluctuating equities that may fall at times and not even pay a yield, you know there’s a lot not participating long in this market. So why do I feel bullish (apart from the fact that I am always optimistic and often get called a perma-bull) ?

Subscribe for free here:

Well it’s a month ago since my Review in September that pointed out the chart roll overs I was seeing and I warned of a possible market retrace of size. The 250 has fallen from 18500 to 17100 in that month, nearly 8%. Roll overs are worth paying attention to in stocks and indexes. The 250 looked a better index at the time too – the more obvious roll over charts were the S&P which has only fallen 3.5%. Aim is even doing better than the 250, being off 7%.

All of this seems crazy as there are some ridiculously low valuations around. Forward PE’s of 5 or less are in abundance. 9 percent yields are everywhere, commonplace. I never saw this many low valuations like this during the financial crisis. I think part of the issue is small private investors, they seem to be invested in Aim more than anyone else and this index has come off the most, 50% over 2 years, a relentless drop. That’s a lot of pain for many novices and non-pros to endure, it’s bad enough if you are a battle hardened pro. The problem is investors have had so much to worry about in recent years. We had the Brexit vote, that caught a lot out, then Brexit itself, hotly followed by Covid, then Ukraine and now the middle east. You can understand investors thinking “that’s it, I don’t want anymore – 5% in ‘safe’ gilts looks great while we have all the inflation and growth uncertainty!” That just continually exacerbates the fall imo as sellers dump shares the price falls and as the price falls more investors sell – it becomes self-perpetuating. The issue with Aim is there are few divi payers and divis tend to act as a anchor bolts in the mountain side where investors can say they will hold on or buy because they get a decent income. Many aim stocks lack assets too and asset values are another ‘anchor’ investors can use as a comfort blanket to mix metaphores. So it’s little wonder Aim has been hit so hard. Shoezone (SHOE) is on Aim. I have held for two years and in that time I am up 200% approx. It put out fab results this week. In June they raised their forecasts for pbt to be £3m higher than expected at £10.5m rather than £7.5m. In July they upped that another £3m to £13.5m expectations. This week they said pbt will be ‘not less’ than £16m – more than double the expectations in the market in June. The shares have risen 5% in that time! Net cash of £16m. There’s a yield of 4.5% and the company has bought back 3.8m shares meaning the profit now gets shared around by fewer people. They generate so much cash they can buy back loads more shares, increase the standard divi, pay special divis yet the market ignores them a puts them on a PE of 9 on this years forecasts that they have just confirmed, the fwd PE is likely way lower. There’s only 46.2m shares around next year rather than 50m, that increases eps by near 5% on it’s own without a penny more profit. The market may be ignoring it for now but the PE, the yield and the cash means these have held up on Aim when others haven’t, because the others lack profits, cash generation, yield or assets. Investors are just beaten up, the pain of losing money has become so great they are blinded by pain – selling their shares is like a shot of morphine. But like morphine, the relief of selling wears off when you start seeing the market rally and you are all in cash, and that brings it’s own pain. the pain of missing out.

I think going forward, a lot of novice aim investors will be investing differently, and if they don’t they should do. The importance of profit and cash generation will come to the fore. I’ve always found that the best way to make money fast was to try to make money slowly and safely.

There will be a point when this market turns around and there’s a rush to buy quality Aim and other sold off stocks, these valuations can’t stay this low imo. One thing I’d say is it’s easy to let your mind run away when a stock falls – you can conjure up all sorts of scary demons in your mind when a stock falls unexpectedly – the mind is an investors biggest enemy at times. A big mistake many make in market falls is to bank profits on the winners and hold onto those that are underwater in the hope of being able to sell at a profit at some point. I try to avoid doing that as it means selling stocks that are likely your best performing and keeping your poor performers. In a bounce it’s usually those with previous strong performance that get bought heaviest, losers tend to remain losers or bounce minimally imo. It really is a weak market tho, it reminds me just after the tech boom when everyone had ignored ordinary stocks for techs. I remember car dealers CD Bramall and Lookers being on PE’s of 5 with 6%+ yields and the market ignoring them because techs were a one way bet, till they weren’t. So many 10 baggers were born out of that.

Looking at the charts, the VIX broke through the resistance yesterday and that is one big bowl from that high in March.

I don’t know if the VIX will hit that high again, it depends how fast the S&P falls from here if it falls through this weak support level. Looking at the longer term trend on the VIX I expect it to top here between 25 and 28 on a day with a big fall of 2%+ as my best guess – it will likely carry on making these declining highs on the three year chart below.

Markets usually bottom on a capitulation or a big fall when punters just panic and sell. I’d guess the S&P may well give back 4% to that lower horizontal line as a capitulation. That would all add up, get crappy October out of the way then start a positive move from November when all the results emerge. That’s my best guess but I and nobody else ‘know’, it’s all about past experience in these situations and history is the best guide to the future. I lived through the 87 Black Monday crash when the market lost 27% in 2 days – now that’s what ya call a crash’ as Crocodile Dundee might have said. But I have never forgotten that after that Monday and Tuesday fall, the Wednesday rally was the start of the next bull market.

There’s good reason why these capitulations mark significant bottoms if you think about it – any investors left still holding after a fall like that are likely to hold through most things so short term there’s few sellers left – those are conditions for a rally and the market then bounces. Think about risk and perceived risk here too. If you think it’s too risky buying here as a contrarian what was the risk at the highs when you were really confident and was buying?

Onto this week and I have been buying, albeit I’ve had to sell a couple of things to raise the cash to buy. My portfolio is now limited to holdings that I feel can at least double in 12 months. Reluctantly I have sold KITW and the rest of my TEP. I think these will still perform very well but I can’t see them doubling In 12 months.

The stocks I have bought are:

Avon Protection (AVON) – no, it isn’t the Two Rons, ‘der management’ – Avon design and manufacture Army helmets and respiratory masks and are world leaders. I bought these about 15 years ago at around 35p and sold at around 50p only to watch them sail north to 46 ruddy quid! 15 years ago I was more stupid than I am today, I never did the deep research I should have done. In mitigating evidence on my part I would like to say they were making milking equipment at the time as their headline product so I missed the move into defence. They now have huge barriers to entry and a moat as wide as the Thames. Trying to muscle into their business and develop these helmets and masks is a long and difficult process when dealing with the US Department of Defence among others.

The shares have fallen dramatically after a disastrous foray into body armour and products that just failed DoD tests and were riddled with delays and cancelled orders. 10 months ago they got a new CEO, Jos Sclater after getting a new CFO nearly two years ago, the appropriately named “Rich Cashin”. Jos Sclater has been instrumental in turnarounds at GKN, Ultra Electronics and Castrol among others. I like turnaround, new boards, directors sounding more upbeat and charts turning up. Add in director buying and you usually have the perfect recovery formula and boy have these directors been buying, After a great trading update this week the directors have been piling in, in serious size after loading up last May too. What surprises me is the full year results are in 4 weeks time – I thought directors were not allowed to buy shares in the 6 week closed period lead up to results. There’s been a 30% upgrade to earnings on Stocko this week and looking at the forecasts 49.7c (38p) for this year ahead, that’s half what they achieved at the peak share price. An upgrade there after the results might make it even more. The little recent bowl looks good in my eyes and despite the recent rise from £6 to £8.50 there’s oodles of recovery potential left imo

Note there has been no share dilution either.

The co has cancelled the share buy backs and although they paid a 17c interim divi the 37.5c divi for the year is likely to be reduced to a more realistic yield for now while they invest for growth. They have a new Elite Helmet and so other exciting products coming down the line. I would definitely watch the interim results webcast as part of your research if they whet your appetite and get a feel for Jos Sclater – he looks and sounds like a guy on his game imo

I’ve also been buying Mpac (MPAC) Another recover play and one I was buying at 70p around 15 years ago which hit 650p at the market peak in July 2021 after I had sold around £3. I’ve nibbled in a couple of times over the last year but too early – so sold out again as the news disappointed. However Tony Steele the CEO left in March to be replaced by the COO Adam Holland so I’ve been nibbling in at around 210p. The noises from him have been good, they seem to be inline and set to do 26.1p eps this year, 38.5p next year, a PE of 8 falling to 5.5. Mpac started out as Molins, decades ago, a cigarette machine manufacture. Today they produce production lines for all sorts of products for manufacturer to companies around the world. The big story is they are currently building a prototype automatic EV battery line for Freyer. If this all goes well they will be in prime position to build a number of these production lines around the world for them. That isn’t priced into forecasts as they have yet to win the business or prove this automated line but they expect to announce something in Q4 they say, which can’t be far away. I noticed this on Motley Fool a week ago regarding Freyr:

“The young lithium-ion battery maker is one step closer to producing sample cells for customers.”

https://www.fool.com/investing/2023/10/04/why-freyr-battery-stock-surged-today/

As I see it the valuation is very cheap without a production deal with Freyr, if it comes good the stock could rise hugely – seems like great potential reward for little risk imo but obviously do your research. The CEO and another director were buying in March. I should add these are very illiquid and 1-2k can move the price at times so they can be tough to sell on negative news so be careful not to be over exposed, but more importantly do your own research, you press the buy/sell button and I am long so I’m likely biased, I may even be stupid.

Lastly, I have been buying Ashtead Technology (AT.)

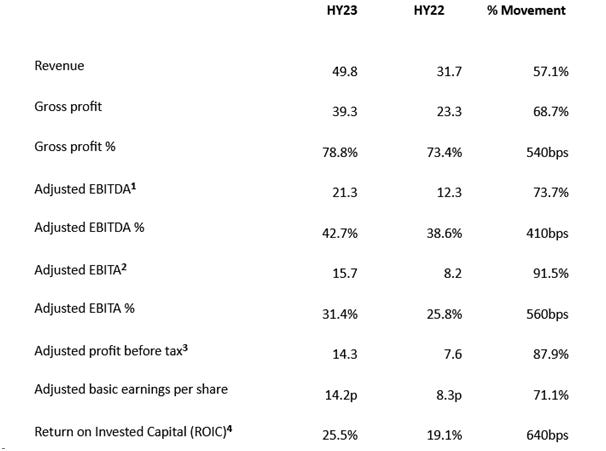

No recovery here, just a float from 2 years ago that has gone from strength to strength over the past two years. They do all things subsea to do with wind turbines and rigs. The last results in September were stunning:

I’ll let them speak for themselves but with 14.2p eps in H1 it means the 28p eps forecast for the year looks well doable, possibly more, and that would be double last year’s earnings.

Doublng earnings on a PE of 16? About to start paying a divi and in the right sector at the right time as Wind Turbines in the sea increasing at pace meaning lots of work commissioning and also doing maintenance let alone repair for turbines and decommissioning of oil and gas rigs. What also looks very interesting is the curve up and momentum in the chart. Makes about one earnings enhancing acquisition a year and has £26m net debt with a mkt cap of £370m

Just to re-emphasise, these are just stocks that attract me but I am not suggesting you buy, you decide for yourself if they interest you and make you own decision and do your own research and due dilly.

One week left in October – there’s a few interesting updates before the end of the months that I’ll read with interest.

23rd IGR trading update

24th ANG interims

25th VINO finals20th

27th FOXT Q3 trading update DB

IGR has been falling sharply recently so that may be lively on the update.

Remember it’s always a good time for stocks, a good time to buy or a good time to sell – you just need to get the timing the right way around!

Enjoy the weekend

Rebel

Rich Cashin? That's brilliant, one you just couldn't make up! It's been a tough week so a little hallows humour goes a long way.

You were quite positive on TEP recently, what changed your mind - was it the lack of a step up on the recent update or simply the refocus on doublers?

There's a good article by Ed Croft in Stocko yesterday concerning limiting losses, and with interesting debate in the comments section:

https://app.stockopedia.com/content/a-practical-guide-to-keeping-losses-small-978068?order=createdAt&sort=desc&mode=threaded

I don't mind personally buying AIM but won't buy micro cap and as with all holdings there has to little or no debt, and there must be a decent progressing dividend (or one to be introduced imminently), and the spread must be tight among a plethora of other requirements!

Thanks for the macro analysis, very interesting and chines with other chartists. Going to hunker down in the bunker with my Avon helmet on...

[I hold TEP]