The Weekend Rebel Review 12-13th August 2023

A Perfect Storm? CARD, SHOE, FOUR, RR.

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, Everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.Well the rain has killed any hope of doing anything meaningful outside today so time for a weekend review again this week. There’s a fabulous feeling about the market currently imo, tho many may not feel it. When investors/traders sell off just because they cannot take anymore, when they just want ‘pain relief’ or 5% guaranteed from gilts looks attractive compared to fluctuating equities that may fall at times and not even pay a yield, you know there’s a lot not participating long in this market. So why do I feel bullish (apart from the fact that I am always optimistic and often get called a perma-bull) ?

Subscribe for free here

Is this the cheapest market in decades being ignore by punter through sheer pain and attrition?

Another good week, blessed by a bit of sun at last. It is quite heartening to here investors and traders at least say the market feels firmer and they are having a series of up days for a change. What excites me more is that as markets do firm it draws the hot money in, the FOMO money. This tends to pick up pace as fear turns to greed. What I expect to see now and expect too see more and more and it already seems to be happening is stocks rallying on result and even if they just meet expectatrons. There’s a number of charts here like the 250 and the Small Cap index that are nearing resistance and if they break through, the technical bods will be chasing stocks higher. PE expansion will start too imo, so where funds or investors might not have been prepared to pay a PE over 8 for the likes of MKS, the PE will rise. When earnings are rising and PE’s are expanding things start to feed on themselves. I think we are near to that point where brokers are more aggressive with their upgrades. It’s already starting JEFFERIES RAISES ROLLS-ROYCE PRICE TARGET TO 310 (210) PENCE - 'BUY' That’s another 50% to go and double what RR. Was trading on a few weeks ago. At the top, brokers are all saying buy and increasing forecasts. At the bottom they are all saying sell. Brokers are raely ahead of the curve and when they are they keep the news for their favoured clients before bigging things up in public imo. I think I and everyone that bought the market big in October got in while the brokers were behind the curve. So I expect to see more and more positive notes and fewer downgrades. The market feels like we are in for a bullish last third of the year imo.

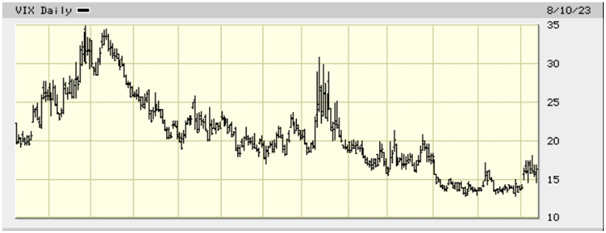

The VIX made a bit of a bowl in recent weeks but looks like it has failed to break higher. That’s good news and I expect the VIX to fall back here.

The Russell and the Dow Transport have both pulled back inline with the S&P but I expect them to bounce soon too.

China’s growth is slumping – how much of that is down to re-shoring? I think the US are doing a lot of this, hence their growth. It’s happening in the UK too and the firmer £ and lower shipping prices are likely to show up in the profit box for many soon imo.

Halifax has reduced it’s mortgage rate by 0.7%. Mortgage rates coming down and house prices falling means much more affordable houses to buy. Regardless of what any agent tells you, house prices are 15-20% lower than 18 months ago. People have become more realistic. It is impossible to gauge price falls and increases accurately because you are never comparing like with like but watching Rightmove you can see the amount of houses being reduced and new instructions are far more realistic. Renters feeling miffed by landlords are likely to get onto the housing ladder. For this reason, simply because markets look forward, I think house builders have seen the builders bottom. Some may think we aren’t there yet but I think we are past the bottom. Look back at Barretts Developments. It bottomed in July 2008 while indexes were still tanking. Even when Lehmans went bust months later Barretts never fell through the July low. Things don’t look great but the market in house builders always bottoms when things look bad. Remember funds usually have to buy when they can, not when they want to if they want a large stake, so they need to buy well before the happy bell rings.

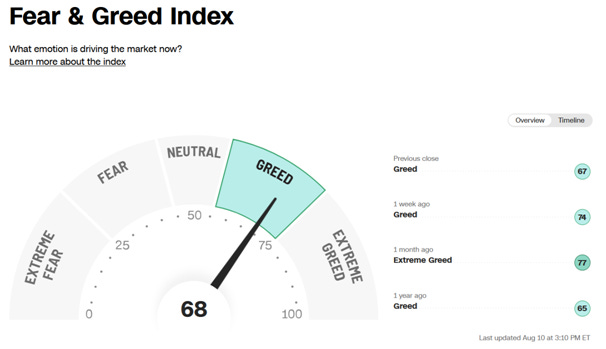

Fear Greed lower still, I don’t think it is going much lower.

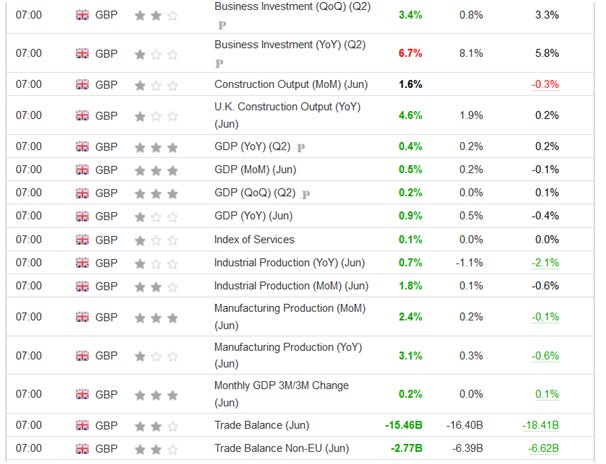

UK GDP data out yesterday was stronger than expected, massively stronger month on month. A forecast of flat zero growth on an annual basis was beaten with a 0.2% over 0.1% in Q1 – that made 0.4% for the year on year number, not stunning but a lot better than the recession the experts have been forecasting for a year. What did catch my eye was the recent month on month numbers which most beat by a country mile – the numbers themselves were nearly all big beats. Perhaps apprenticeships are starting to have an effect with young people going into real jobs where you earn real money rather than shirk it for 3 years just having a jolly at Uni doing media studies and landing themselves a huge debt. I think the state paying for anyone to go to uni and doss for 3 years did huge damage, making kids have loans has actually made them start to think rather than just put of getting a job for 3 years in many cases – tho not all obviously.

Manufacturing was particularly strong along with industrial production so perhaps all the on-shoring from China is starting to show up in economic numbers now? I was dumbfounded yesterday that the 250 was down on such strong month on month GDP numbers. It tells me the fund managers are on their holiday, the private investors are suitably depressed and shares are remarkably cheap. I hear punters on Twitter feeling really down, sick of not getting their daily or weekly tick up. In all the time I have been investing I cannot remember another time, save perhaps 2009, when punters we so depressed.

Card Factory – (I’ll do a full update to my Substack for CARD at the interims in7 weeks time.)

Well after mentioning these in last weeks Review my first Substack write up has come good again and they duly roared away 15% higher on Monday, nothing to do with me but the trading update issued on Monday in which they said they were ‘materially ahead’. Market convention says ‘materially ahead’ means 20% ahead or better, ‘significantly ahead’ being 10-20% higher. CARD said ‘materially ahead’ for both H1 and the full year. Claiming the full year will be materially ahead means the current consensus forecast of 11.4p eps have been raised to 11.9p, clearly nothing like the 20%+ they should have done. I expect 13.7p eps at least this year now with scope for far more. The cash generation should be fabulous, they are investing £25m a year for 3 years, growing the business while reducing debt and returning to the dividend list too. I’m sure now they will declare a divi with the final results, question is will it just be an H2 divi or a bit more to make up for no H1 divi. Either way they are capable of paying a 2.5p H2 divi or a 5p full year divi in April imo. From then on it will be a third of earnings p/a going fwd until they reduce the investment rate I suspect, with potential for specials if they feel particularly flush.

The results are in about 7 weeks time. I expect the market to start to wake up then if not before imo. At the moment there seems to be a seller around. Telios has reduced another 1% but we don’t know how much they want to sell. Investors and punters have a misconception about ‘Card Factory’ too, they assume sending cards is a dying participation. It may be for Paperchase and Clintons but CARD have been part of ‘their’ demise, they aren’t part of ‘the’ demise. If Card were called ‘Super Gifts’ instead and recently floated as a new exciting high growth, high cash generation retailer the brokers and punters would be all over them. Remember Tie Rack and Sock Shop? Small footprint, high footfall retailers can make huge returns. They also can command much higher ratings. Cards are a dying product? Did you know that the fastest growing buyer of cards for the last 4 years has been 16-20 year olds? Let’s see where these go on the interim results in September. I am pretty sure the share price is currently held back by a seller in the market. This happens at times in quiet summers when there aren’t the buyers around or fund manager are holidaying. At some point a larger buyer is going to take out the seller. I have always been a buyer of value and prepared to wait for the price to react as it is often near impossible to buy value like this when the sellers dry up and you want to hold a decent amount. Obviously everyone behaves differently and how they prefer.

Remember too that the acquisition in South Africa already had the sales and profits factored into forecasts. So this is high sales and profits from the shop floor. I will do a more full Substack update on the interims. Meanwhile I suggest investors load the Card Factory app onto their phone and look at the range of gifts they now sell online. CARD will do record sales this year and while brokers and the company won’t say this, I believe by year end they will get to near all time highs EPS in my humble opinion. Obviously do your own research and as I’m very long CARD then I am very much biased and that could just be hype if you don’t check the data out.

On to the market and company guidance and broker forecasts: It has become increasingly clear to me over the past year that many brokers are forecasting way too low on many companies. In some instances brokers are playing cautious. In others, companies are guiding cautiously. You can understand companies wanting to guide cautiously, after Covid and Ukraine many were feeling like they hadn’t a clue themselves. The good companies want to under-promise and over deliver. In some cases both the co and the broker are guiding cautiously which compounds things. When this happens you get some mad catch ups. CARD in Nov said their results would beat by nearly 10% and in Jan they said that would be beaten again by another 10%. Later in April they hiked forecasts again by nearly 10%. The guidance was obviously very over-cautious. They have now said they will be materially ahead again for the half year and the year. That’s a circa 70% lift in earnings since Nov.

CARD are not on their own tho. SHOE has had two earnings upgrades in little over a month hiking consensus from 13.2p to 19.6p. I suspect that won’t be the last before the results.

RR. absolutely busted forecasts, that’s a FTSE100 co. Forecasts have now been raised

FOUR this week mashed forecasts, Forecasts have now been raised.

My point tho is that Joe public often only gets to see the consensus numbers. If there are 4 broker forecasts, one near to correct and three low balls then the consensus will likely be well short of reality. RR. Has gone from 4.98p eps forecast in July, for this year to 7.7p now as consensus. Give me a break – they did nearly 5p eps in H1 alone. Someone is guiding low for another big beat going fwd imo.

FOUR announced interims of 176c for H1 this week. The consensus for this year hasn’t risen, it is at 272c, next year has been raised to 324c. Cummon, credit investors with some savvy. If I double H1 I get 352c this year, if I look at the trailing 12 months it’s 342c. One thing I have noticed with broker calls is that often 2024 forecasts are ofter about where 2023 should have been set – it almost looks like it’s code to those that know to look at 2024 to get your 2023 number when forecasts look plainly too low imo.

Now something many punters won’t know, just worth mentioning. CARD, SHOE and FOUR have no more shares in issue than they had in 2017 more or less, in fact SHOE has reduce the number of shares by 10% from 50m to 46.2m Dilution is the devils work. Look at Mike Ashley and Frasers 531m shares in 2017, now 457m – he owns most of the co, just like the Smiths at SHOE – he doesn’t dilute himself. I don’t think FOUR, SHOE or CARD have issued any meaningful amount of shares since floatation . Anti-dilution indicates class imo.

There hasn’t been a bundle of other great co news out this week but I think September will see a deluge as it is a very active results and trading update month. ‘Sell in May and go away, come back in September for a time to remember’. Very poignant this year?

Wednesday is the UK inflation numbers, that will be a day to pay attention.

Have an enjoyable weekend.

CR

Nice one CR. Have you any thoughts on the impact for Card Factory of Clinton Cards woes? It's easy to say they'll benefit where they are both sited in the same town, though I fear for the survivors every time a retail business retreats from the high street. I'm wondering about what the geographic overlap is of the two businesses and whether CARD might be sniffing an opportunity with some Clinton sites.

I hold CARD and commented about them on another stack last evening. that I like to leave the price sticker on now when I send one, in so doing my business partner was able to appreciate just how little I value him on his 50th birthday! That's okay, £1.69 pleased me and he's a miserly bean counter. I imagine he will tippex out my greeting and send the card to his younger brother in a year or two. In hindsight I should have used a pencil.

I think value has a way to run in the current social and economic mindset. The effect of cheap food retailers marching into Sainsbury and Waitrose territory is breaking down the social stigma. Cards are very similar to food, you have to buy it but don't want to pay too much. Shoes, (I also hold SHOE) is a little different because what you put on your feet is important to health, but lots of people don't recognise that, or hard pressed families and older folk can't afford to. Anecdotally I pick up good vibes from Shoe Zone staff when i call in to top up my mother's array of slippers.

Keep up the good comm's, thanks for sharing.

TEIN

"Regardless of what any agent tells you, house prices are 15-20% lower than 18 months ago.".......source??? Nationwide price Index over the last 12 months is -3.5% (June 2022 to June 2023) while Halifax Price Index is showing an even lower drop......https://www.nationwidehousepriceindex.co.uk/reports