The Weekend Rebel Review 11th May, 2024

A short week, long stocks. FCH, SYNT, AVON, FDEV, THG

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

With only 4 days this week I will make it a shortER one this week. I’ll keep the macro short as not a lot has changed, have done a bit more detail into some stocks instead. The indexes are breaking out nicely here in the UK. With interest rates getting ever nearer to a cut, and two members of the BofE voting to cut, the punters are getting excited. The Inflation numbers the middle of this month could be a big catalyst for chart moves. On Friday we had GDP data and the UK smashed it:

The UK is now the third strongest growing company in the G7 since the Brexit vote -in 2016. With this data shares should be game on in a big way. If we get inflation down further then we could see a rate cut on the way. When did we last have strong increasing growth and falling interest rates? I think the UK will come into focus.

For two to three years, small caps have been ignored. Once the rumour gets around that stocks are on the up, all the investors, amateur and professional will be getting FOMO and rushing into the market again in my opinion. Many will look at what some small caps have done since the start of the year, rising 100% to 200% or more and still fundamentally cheap, so they will be looking to find the next big movers, or buying those that are already moving.

Here's the Small Cap Index, just breaking a key resistance, look at the big lows and highs. This index typically rallies 100% to 200% between major highs and lows:

I would expect the next major peak to be at least 12k, perhaps 18k going by past long term trends. Market bottoms like this are when you get a once in a decade chance to buy lots of decent stakes in grossly over-looked, under-valued companies and just hold them while they multi-bag. Nearly my entire holdings here have easy one-bagability pretty swift, aside from perhaps RR. and MKS. I’ve greatly reduced my stake in these and what I hold now are pure profit but still very meaningful, making 7% of my holding between them, both have more than one bagged for me. I’m trimming GNC because it can’t one-bag in a year I don’t believe, I think there are better candidates now. I have never known so many stocks on compelling valuations, so overlooked. There will be no end of fabulously cheap stocks revealing themselves at results please going forward and sentiment may be very different.

Here’s the S&P – when that high gets taken out the US will start buzzing too – it’s not far off imo.

Look where Fear/Greed is, there isn’t over-bullishness in the market looking at this:

So all in all it’s time for me to get really aggressive (Shut your face! 😊 ). These greatly under-priced bottoms occur rarely so I’ll be going in hard into the most baggable stocks and trimming anything that lags – going big and early increases your compounding. This is just the way I invest at this stage of the market. When markets get long in the tooth, one baggers are harder to find – although recovery plays are always there and can multibag. At market bottoms, there’s loads of one-bagger+ stocks looking at you, you just need to find the best and the fastest.

So onto stocks this week. A lot of stocks are starting to move and the moves are more meaningful. After a decent 1.5% gain last week, the portfolio is up over 4%+ this week. Over 5 % since the start of May. FDEV, MPAC, FCH, PFD, SYNT IGR and others were all roaring away at the start of the week and I’ve kept my holdings down to 17, many hitting new recent highs here.

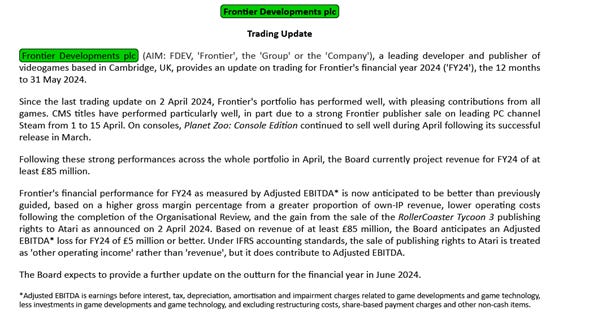

FDEV was very strong this week, thanks to a trading update:

They followed it up with news that there will be a new third Jurrasic Park game developed for Universal Pictures. I was holding these from a little after the last trading update which was ‘ahead’ but it’s not a stock I feel greatly comfy with as far as understanding their market. I did like the bowl on the chart which is why I bought. I think the bowl says there’s more to come. Berenberg raised their target from 170p to 300p. It’s only about 5% of my holdings now as I halved them.

Synthomer, SYNT, is a world-leading supplier of high-performance, highly specialised polymers and ingredients that play vital roles in key sectors such as coatings, construction, adhesives, and health and protection. I have followed the company and held it before, it used to be called Yule Catto. The business has 3 main groups - Coatings & Construction Solutions, Adhesive Solutions and Health & Protection and Performance Materials. Rather than repeat everything in words, there are three videos explaining each here:

https://www.synthomer.com/about-us/our-divisions/

If we are seeing things pick up around the world then these, SYNT will likely be big beneficiaries and one of the first to recover imo, their products get used in a lot of global manufacturing. Michael Willlome has a great track record, he joined as CEO in Nov 2021. He oversaw recoveries and turnarounds in Clariant and Conzzeta prior to joining Synthomer.

They had a good trading update on Thursday.

This is a classic recovery play. The stock has been totally beaten down, 90% from where it was, that means to get back where it once stood, the shares will have to rise 12 fold. It is being valued at half book value. With recovery plays it’s no good waiting for the co to say things are much better, the price will have double or more by then. If they do come out with an upbeat trading statement I think you’ll likely be paying 20-30% more in the opening auction. What I am looking for is nuances in what they say, slightly more positive language.

“Volumes were the highest since Q2 2022”

“we are seeing improving activity levels in some of the segments of the Group that were previously more challenged.”

There are several other positive sound bites. They are 4.5 months into the year, they will want to see 6 months under the belt before starting to sound more confident, they’ve been through the wringer – at the results presentation Michael Willome said they don’t do ‘hope’. When they are certain things are improved into a reliable trend, they will say so and don’t want to over promise. Reporting good news will be when it’s definitely under the belt imo.

The statement gave me what I wanted and what I expected. It rose on the news. The chart is a classic bowl and directors have been buying. This is a big holding of mine. It has one bagged since Jan, I missed the low by some way but well in profit now. The beauty of SYNT is they have chopped out and continue to chop out lots of overheads. When sales pick up, profits pick up much faster. I think these could have a real moment at some point.

On Friday, Berenberg upgraded forecasts with Buy and a raised forecast target from 325p to 375p.

Avon Protection.

On Thursday, AVON announced they had won a £38m contract for General Service Respirator and associated in service support for the UK Ministry of Defence ("MoD"). Defence is a hot sector with all the waring going on. AVON has now doubled since October, I’m getting close to one bagging them. Results are on 12th May. I’m looking forward to Jos Slater laying out the turnaround.

Funding Circle, FCH (Aim)

Funding Circle floated on Aim in September 2018 at 440p a share. Samir Desai was CEO and co-founder, one of three guys that had come up with the business idea for lending to small businesses.

As most people know, who have ever run a small business, borrowing money isn’t easy. On the other hand, many banks will tell you that assessing the risk of loans to small businesses is difficult. Banks have and still do rely on ratings agencies and a business owner’s financial track record for assessing credit-worthiness but the issue is many small business owners have limited track records.

Funding Circle was created with the idea of raising capital, typically from £100-500k, by small businesses, easier, faster and cheaper. They do this by using machine learning and huge amounts of data on small businesses. With this data, they can assess whether a business is creditworthy very swiftly, 30 seconds to see if you are eligible, a 10 min form to fill in and an agreement in principle in one hour. Anyone that has had a small business knows that you can’t even get to speak with your bank in that sort of time.

Funding Circle do not fund the loan, they are just an intermediaries between the lender and the borrower. If borrowers like to use them for the ease of process, lenders like to be involved because Funding Circle’s proprietary credit worthiness machine learning software and their huge data means they are 3 times more reliable than standard bank credit assessment. I like this because it means as an investor, I don’t have a lot of cash at risk via loan defaults.

Funding Circle have recently introduced a Flexipay Card. It’s like a credit card but by offering transfers as well as a card, you get more flexibility than a traditional business credit card – helping you pay rent, bills, payroll and more. You can use it as much or as little as you like and you only pay when you use it, so you’re not tied into a long-term commitment. There’s one, simple flat fee per transaction so businesses always know what they’re paying. No interest, no surprises.

At the recent results in March, Funding Circle had revenues of £162m. up 7%. Adjusted EBITDA loss was £3.9m. They have net unrestricted cash of £169m. This was due to legacy business loans being paid down while the cost of expanding in the US increased.

The UK Loans business produced £6.5m pre tax profit thanks to higher sales and higher margins.

Flexipay sales nearly quadruple to £234m but isn’t profitable yet. 6% of the business is based in Germany and the Netherlands where revenue for the year grew 19% to £13.3. This business is being consolidated into the UK. “Germany and the Netherlands represent only 8% of Group revenue but c.60% of adjusted EBITDA losses. By reorganising both businesses we move to a more efficient model that better serves small businesses in these markets whilst allowing the Group to accelerate its plans to deliver profitable growth.” The company says.

The UK businesses (UK Loans and FlexiPay) will be PBT positive from H2 2024.

As far as the US goes, Funding Circle have been accelerating investment there but have made the decision that with them reaching a point where they have to increase investment heavily to grow, while still loss-making, they are withdrawing from the US. They have received a number of expressions of interest in the business there. The US is basically the same as the UK but behind due to it coming later to the company via investment, it makes the rest of the losses. The company says it’s exiting the US business and they have received expressions of interest. They have been expanding into the US but I don’t think the US business is as easy as the UK and as they are at a point where they need to increase investment their to grow it, they’ve decided it isn’t worth the candle. I don’t know what they could get for the US business. Total income for US Loans was £32.5m and it made a AEBITDA loss of £10.6m. Could they get one times sales? I don’t know. Conservatively I am just looking at them offloading it and ending the losses in the US and anything they get will be a bonus. The great thing going forward will be a profitable business, a huge amount of net cash, and Flexipay growing like a Triffid. The loans business and Flexipay are great self-pollinators, those that take out loans get introduced to Flexipay and vice versa. FlexiPay transactions almost quadrupled to £234m.

So I’m looking at £6.5m pbt from Loans. Let’s say you could add another £7m by killing off the US doing back of a fag packet calcs. Germany and Netherlands representing 60% of EBITDA loss and that looks like it could be reduced or even wiped out when they re-centre it to the UK. All in all that looks like they could be doing £20m+ pbt now if these changes were already in action. That ties in with the 2025 forecasts of £27m pbt and that would mean FCH are trading at around 10 times pbt.

Now take into account they have 65% of the market cap in unrestricted net cash + anything the get from selling the US. I looks mad cheap still imo.

Lisa Jacobs is the new CEO, she has worked her way up into this position by running the UK so well for 8 years. I wonder whether Samir Desai stepped down as he knew going into the US wasn’t the greatest move and would look better if a new CEO actually did the job of pulling out, rather than him admitting he had goofed up perhaps? Whatever the reason, Lisa Jacobs seems a very capable CEO. I think if you strip out the cash these are likely trading on a PE of 3-4 perhaps. Stocko have 6.08p eps forecast for 2025, A PE of 13 ignoring the cash. There will be no more cash burn after 2024 and what cash burn there is sounds like it will be minimal, listening to the CFO. They have just started £25m buy back and have already repurchased 2% of the company shares. The CEO has said she is doing so as the shares are ‘materially undervalued’. They could possibly give 25p a share back to share-holders quite easily. All in all, it looks very cheap despite the shares having risen 200% in a month – but that’s what happens in crazy markets. I’ve been buying from 43p. The co has bought back paying up to 76.6p this week.

D.Bank came out last week with a 250p share price target.

The company has its AGM next week.

Forecasts are for a 2.5p eps loss this year, 6p eps next year. Looks conservative imo. If you ignored the net cash of £169m the PE is just 13 for what could be strong growth and plenty of cash returns to growth shareholders.

A little bit of trader stuff – THG – I noticed a bowl forming over the past two weeks, yesterday the CFO bought 312 k shares. This would never make a hold for me but might be an interesting trade:

Coming up this week to watch out for imo:

14th GRG trading update

14th LUCE AGM

15th MPAC AGM

15th FCH AGM

16th PFD Finals

So a cracking week but remember these are just the views of a private investor, not an analyst. I hold all or nearly all the shares I write about here so I will be biased. Please do your own research and make your own decisions, these aren’t tips, just biased waffle about the market and my shareholdings.

Rebel.

that sounds pretty reasonable as a plan. I just don't think I'd be able to gauge the currency and the rate cut decision and timing so I tend to stick with what I know and am best at.

Good luck

Thanks again CR. For continuing sound info. Which is making me a nice profit in stocks I probably wouldn’t even have noticed