The Rebel Bumper Year End Review and 2024 Preview,

Naps, views and other stuff.

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required. Please do your own research, know your own risk profile, understand what you are buying and make your own educated decision to buy and sell.

So one year closes and another opens. 2023 has been tough, but it hasn’t been dull, certainly not in the past few months anyway. I think if I was to use a football analogy, I’d say it was a game of 2 halves Motty. I think gloom was about as bad as I can ever remember it, around the summer, while actual fear wasn’t that deep. It was very clear by the summer most people were not selling but there were just no buyers around. Summer is never good for drawing in buyers, too many people are doing too many other things, so it was likely that the old ‘Come Back on St Leger Day’ was going to work this year, and so it did. The overwhelming things I noticed early on this year was the lack of two-way trading. Sharepad was regularly showing me throughout the first 9 months that the average daily volume was around 30% of normal volume for nearly all stocks. Trying to buy a small cap share that had been constantly falling last year, I called my broker and was told there was very little stock available – and that’s how it carried on. Prices were falling on some stocks but you couldn’t buy much if you wanted to – almost as if we never had a market. This is why I watch Fear/Greed and the Vix. In weak markets like that, I want to be buying when others are throwing in the towel without thought – high fear and high Vix are indicators that point to a good time to buy. Closed end Investment funds were seeing redemptions and so having to sell their holdings to raise cash, a vicious circle as punters fled to an easy 4-5% ‘risk-free’ in gilts and fixed interest. The Truss-shambles also triggered a lot of selling by pension funds that had leveraged debt. All of these issues, triggered by increasingly higher interest rates, set off a domino effect that needed a circuit breaker, which finally came when the BofE stopped raising rates.

It has been a very difficult market for everyone. Aim has been walloped during the year. As a headline, Aim is down 10% from the start of 2023 which doesn’t sound too painful. However, if you measure from Feb to October it was down 25%. Meanwhile, if you bought the FTSE250 at the start of the year you are up. A real tops turvy year where most Aim microcaps were walloped but FTSE350 stocks MKS and RR. were up 100%-200%+, that isn’t meant to happen. I have pretty much avoided most of Aim unless it pays a divi and has a strong recent track record, ie, hitting highs this year rather than getting cremated and also having meaningful director buying. Personally, I think if you play in the small Aim sector, recently floated, no divi, little public trading record, then while you may get lucjy with a multi-bagger the chances are you won’t. The majority will always be losers, so if you get a multi-bagger then the other losses will likely outweigh it. When the market is gung-ho and everyone is buying anything, then you can make money trading the momentum in this dross, trying to do it in a stock picker’s market where winners are in the minority is a losers game imo.

The FTSE250 has trundled up rather like the S&P but less so. In the past market bottoms of the Tech Rout, the Financial Crisis and Covid, the 250 made far bigger gains than we have seen thus far.

Post tech bounce, 40% in 6 months

Financial Crisis bounce, 50% in 7 months

Covid bounce, 40% in 3 months.

So far the FTSE250 has done 16% gains in two months, I think January results and trading updates will be the catalyst for much more gains, I don’t expect any big pull backs, FOMO is driving the buying like it does on market bottoms imo

Having been long in retail from 2022, my retailer holdings held up well through the first half of the year. CARD, which was 30% of my portfolio rose 40% while 5% holding SHOE did 20% in the first half. Undoubtedly though, the real retail winner for me was MKS. Starting the year at around 120p MKS has more than doubled. Starting the year as a near 5% holding it is now grown to nearly 12-13%. I’ve spent the year trying to beat the indexes the best I can. There have been numerous stocks that have disappointed like Marks Electrical – MRK - which I had not foreseen the in-house staffing move and the associated costs coming, but most fallers have been cancelled out by stuff like DLAR which nearly doubled over the period I held them. Two stand out purchases were RR. which I started buying @ 172p and are up 80% and OTB, up 30% which I only bought heavily recently on the results starting at 130p. WOSG which I have bought in very heavily just ahead of the Nov trading update at just over 500p are up 40%. AVON have also done well since buying in November at 540p approx. My average in most of these has gone up a bit as I’ve increased my positions. WOSG, RR., MKS, AVON OTB and CARD form over 70% of my portfolio, something I have never done before. I always had 7% as a maximum position but increasingly I have realised that chasing ever more shares that I don’t know very well isn’t as good as increasing positions in stocks I do know well and have researched well. That doesn’t mean one of these couldn’t go wrong but across the board if one did go bad the others should more than make up for it, hopefully. Obviously everyone has their own strategy and I’m not advocating others copy mine, you need to do what is right for you, this is just what I’m doing and not advice.

All in all the last two months have been my best two ever in cash and percentage terms, the portfolio is now at the all time high which I have hit 3 times in the past 30 months now , and then retreated – I hope that doesn’t happen this time (stop press - went well through the previous high last day of the year). From the bottom in October, 2 months ago, I have ended up nearly 31%, disappointing because up until 2 weeks ago I was trending to be up 40% by year end from the Oct low. I’ll have to do circa 53% from now till Oct to double the portfolio over 12 months – big ask, but I think I have a bundle of one-bagger potential stocks over 12 month so still do-able if this year is as good as it looks like it might be, bearing how much market bottoms tend to bounce, we will see. Markets just fizzled out over the last 10 days as the S&P neared an all time high but nobody wants to buy convincingly until it breaks out imo, fearful of buying just as the market has a big pull back. I don’t think there will be any big pull backs for a while.

At the end of the day, it’s all just fun and a challenge. As long as I’m here still, along with my family and friends and we are all happy and healthy next October, none of this really matters, other than to ego and pride.

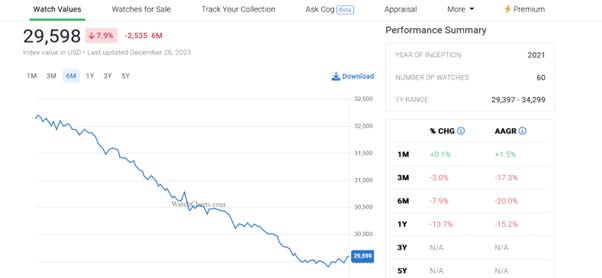

A number of people have asked how I decide when to sell. For me it’s never that difficult, long term holdings or ‘investments’ get sold as soon as I find something that looks like it can perform better. I ask myself, when something has doubled or more ‘how long till this can double again, if it can?’ If I can find something else that can double faster, and all else being equal like risk and liquidity, then I will likely sell the doubler to buy something that’s growing faster. I have no emotion for shares, I never feel sentimental towards a stock, this game is about making money. Shares are casual relationships not lasting love affairs. If a stock has gone from £1 to £2, it then needs to go to £4 to double again. The question is, has the old doubler got the grunt and fortitude to keep doubling? I would likely sell part rather than do the whole lot to start with, mainly because I would probably be cautious, better the devil you know, and all that. It is never a bad policy to sell half on a double, you then hold the rest as free carry. I trimmed CARD to buy WOSG recently and I’ve bought more since and I trimmed some more CARD recently to buy OTB. My thoughts with WOSG is that sellers have just dumped shares, fearing a tightening of belts, Boucherer take-over by Rolex and a recession – all overdone imo. When markets are distressed shares always get over-sold as punters sell just for pain relief. The management sound far more confident, they have been buying shares too. I want to buy before the average investor realises the toughest trading has passed. The recent trading update suggested that, the data is out there if you take time to research. Here’s a Rolex price chart over the past year and more, looks like a bowly bottom forming to me. Also, look at the right hand side and the rate of price decline. In the last 3 months the decline was 2%, the last month it has gone +0.1%. So after a 13%+ decline over 12 months that has reduced rapidly and turned positive. The market looks forward 6-9 months and I feel very confident the trend has changed. You will see that is the first curve up on the chart too.

WOSG share price started to rise well before the used watch price went positive as you would expect. So for me it made sense to hedge my bets and go into what will be a high beta retailer as interest rates fall, and reduce CARD to a more sensible size. I have put the detail in my nap for them below, with my other 4 naps. I like to go in big and early the more confident I get so I like to buy in strongly over a couple of weeks say, in several trades, the more confident I get. Not much worse buying in small then waiting for news that turns out to be good, then topping up heavily after a share has risen 50-100%, even if they have a few hundred percent left in them.

I still like CARD and think they will beat forecasts by some way after the run of materially ahead statement but there has been a string of slight potential headwinds from the rise in stamp prices and the increase in the minimum wage when they have so many staff, both of which don’t help trading. Teleios could still be selling down too, all of which meant a big portion of my portfolio had seen greater risk develop on that basis. I may regret it but I’ve cut CARD to under 10% now. Six to twelve months ago CARD was a great place to be and there were few other places to put a large chunk of the portfolio. Recently, others have shown up and I’m sure more will reveal themselves as we go into 2024. Now the market is turning bullish there’s a lot of ignored bargains ready to move, which were not around 6 months ago. At the end of the day, because I have trimmed it doesn’t mean I can’t then buy back what I have sold, even if I’ve lost out a bit. It can be a good hedge to trim when you have doubts sewn and buy back when those doubts prove unwarranted.

So where do we go from here (is it down to the lake I fear, Haircut100) and what is the outlook for 2024? Well after long bear markets we tend to get strong bull markets where many socks have been oversold and the economy improves. The economy is flat-lining while interest rates have been raised to 10 year highs. Meanwhile inflation has topped out in double digits, retail has slowed, house prices have been falling. That doesn’t sound like a great time to invest on the headlines. What needs to be remembered though is inflation has been falling faster than expected and interest rates don’t look like they need to be as high as they are imo, interest rates are well above the inflation rate. I suspect as bearish as the BofE are, they will be cutting rates by April as they see inflation plunge and risk creating a recession. At the same time new annual pay rises will start kicking in just as pensions rise 10% along with rises to benefits, while inflation runs around in low single digits. Energy prices are expected to fall again around April here in the UK. The government wants to win the election (not that you would know it listening to them) so the budget in the spring will be as ‘give away’ as they can. Over the past year the £ has risen from £1.20 to £1.27 to the US Dollar. That will help bear down on inflation. Fuel and energy prices have fallen too and all these falls in the inflation rate tend to feed on themselves for some time to bring inflation down imo. Markets look 6-9 months out. Come June we will likely be seeing the tangible benefits of these issues in reduced interest rates and higher income. When markets bounce like this then it’s consumer stocks that do well imo, so retailers and consumer facing stocks with high debt and interest charges are likely to be in demand. We could be in a position in June say where inflation is falling, interest rates are falling and companies are growing strongly - Goldilocks. If so, the markets could react strongly too, and likely in advance. Similar looks likely in the US. Of course I could be wrong, I’m no economist, I just like to think I’m a common-sensologist. Why should I invest for the long term here? Well here is the S&P over 30 years. The Financial Crisis and the Covid Crash are now just dips in a chart that is compounding.

Even if investors had invested on any of the previous big highs they would have done great. Most investors would never have dreamed how resilient the S&P and other stock markets would be. The S&P is up 500% from the financial crisis low.

The FTSE Small Cap Index is up around 350% in that time but on individual rises from the lows to highs it is every bit as good as the S&P.

I’m actively trying to keep to holding 10-12 stocks maximum as long term investments and all have one bagger potential within a year. I am, targeting the FTSE Small Cap Index in particular as this is the young, lively breeding ground for the FTSE250 and there’s a long runway from being in the Small Cap Index before entering the FTSE100. I only have a couple of Aim stocks that feel like commited holds other than trades, namely Ashtead Technology (AT.) and Warpaint London (W7L). I have a few small positions in others but need convincing to keep hold long term here.

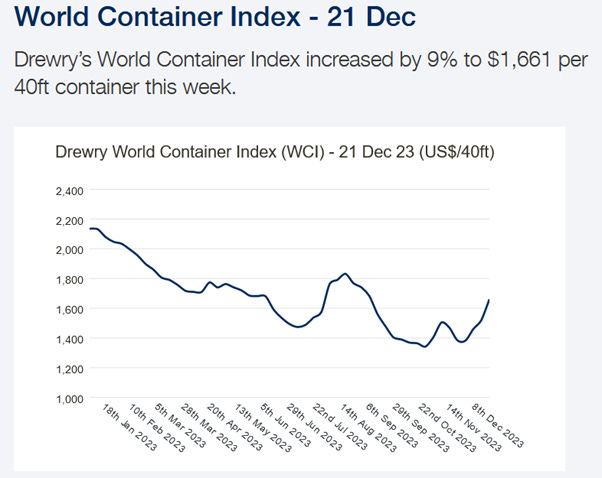

It’s easy to get over confident so I try to stay grounded but I think my confidence is well place on what I have said above. Thurs 21st Dec Shipping Index was great too – having mentioned the two rises in the previous two weeks making nearly 9% rise over the fortnight and what looked like a bowl forming, the rise on the 21st was a further 9% in one week, 18% in 3 weeks! No number this week but we will see a fortnightly number on the 4th I expect.

The Russell2000 is just breaking . Vix and Fear/Greed still out to a 22 month high

A bundle of trading updates hit the wires as soon as we are back in the New Year – there will be some astonishing rallies in the coming months imo.

You only have to look at the potential for recovery on some of these charts to see how these stocks can move when the market is bullish, by looking at the past chart, making sure you take into account any share dilution. Look at a long term chart and we are virtually on the bottom still. There are still some big yields out there that won’t possibly fail to get bought up as confidence grows. Many of these beat up stocks will go on to make new all time highs.

In the financial crisis the FTSE250 fell 55%. After the fall, from the bottom it rose 120% in just under 3 years and was up 200% in just over 4 years. These rebounds occur for two reasons. Firstly, many stocks never underperform as much as price-falls suggest, and secondly, much of the fall isn’t due to a fall in earnings but to a contracting PE. As we go forward and earnings grow we get a rise in earnings and an expansion in the PE on top as investors get more confident and are prepared to pay higher ratings. So an exciting year ahead for the Wide Awake Club. Plane orders stand at a record high, UK car sales were up 14 in October, the price of luxury watches are bottoming out, holidaying is hitting record highs, unemployment is still at historic lows – none of that says recession to me.

As it has become customary in the press, blogs, tipsheets and brokers, we all seem to have to have 5 Naps for the year ahead when we get to New Year’s day. So here’s my 5 for the year ahead, that have the best prospects as far as I can see, at this present moment in time, and a brief reason why. All potential one-baggers in 12 months imo. There are not tips, they are just my 5 largest holdings and they are that size because they are the 5 best shares I can find that have onebagability in 12 months. Do your own research as you make your own decisions.

Watches of Switzerland Group WOSG: Details above, we are not going to see a recession imo, Rolex prices are bottoming, the share chart and the watch value chart are making bowls and WOSG shares have been sold off way too much imo. Huge and fast expansion in the US for growth, which is under exploited and co says it will double sales in 4 years. Directors have been heavy buyers, they are more upbeat and their recent trading suggests H2 will be circa 15% better than last year, that isn’t priced in imo. Used Roxex prices turned positive in the past few days after a year+ decline of more than 15%

Rolls Royce Group RR.: More of the same to come. EPS forecasts have risen 150% over the past year but brokers are way behind the curve. Cashflow will soar, debt will get paid down big and fast, interest payments will fall dramatically with lower debt and lower rates. Upgrades to the shares as RR. debt becomes investment grade, this will see greater institutional demand as will the restoration of divis. Global plane orders hitting highs, global unrest meaning greater need for defence, will all help drive profits. New CEO, lots of heavy dir buying and brokers climbing over each other to raise targets.

Marks & Spencer MKS: Huge self help from their great new CEO Stuart Machine, clothing guru Richard Price, Retail god Archie Norman and Kate Bickerstaff. Closing old stores and opening new ones that drive 30% more profit from 30% less floorspace is a double whammy, so much so that Machin has upped the pace of the rest of the conversions from 3 years to 2 years to do another 200 stores. Food sales up 14.7% and clothing and home up 5.7%, there is so much more recovery to go for, Archie saying ‘we are just in the foothills of what we could achieve’. Loads of self help to come. If there’s two things I like holding it’s food and womens’ lingerie.

Avon Protection AVON: The helmet and respiratory mask maker’s new CEO Jos Sclater and CFO Rich Cashin have both been heavy buyers. They have been in and sorted lots of the issues, cleared the decks in the last trading update and going forward there should be good orders, better margins and strong growth. Brokers have already raised forecasts substantially. There is also a divi being paid. Capital Markets Day in Feb should be very interesting. Avon were £45 a share not long ago, no dilution, needs to rally over 400% to get back to the high. 2025 eps forecasts are not far off the past highs. On my own ‘6 Star recovery indicator’ this co has hit 6 stars, I have rarely had that indicator.

On The Beach OTB: The online travel agent has posted great recovery numbers recently from installation of new software and lower marketing spend requirements. Trading on a single digit PE the recent trading update smashed forecasts. Dir buying including the founder who added over 2.8m recently. A return to paying a divi this year now also been promised after very upbeat results. 50% off its previous high, it needs to rise 100% to get back to where it was. I think it can do record earnings pretty soon. On a single digit PE going forward, they use to trade on a PE of 20+. As the market turns bullish these look exciting imo.

I could have included CARD, but you have to pick these at the start of the year and at this moment in time the five I have chosen have greater momentum.

I hope you’ve enjoyed my views over the past 8 months since starting the Substack and I hope it has helped others make better investing decisions. I would like to thank all those that have sent me messages of thanks over the past year and a special thank you to all of the 30 subscribers that have pledged to pay for subscribing. I will not be taking those pledges but thank you. I do this because I enjoy investing and like spreading knowledge. Investing on your own is boring too. However, if you have made a few extra quid from reading stuff here then how about a little donation to the Trussell Trust

https://www.trusselltrust.org

who do great stuff with Food Banks for those whose best times are likely worse than our worst times, or to Great Ormond Street Hospital

who do great stuff for kids having a dreadful time. Health is wealth.

I’ll leave you with a share-related joke for the year ahead, that you might think of, every time a CEO resigns:

A pretty hopeless CEO of a big listed company gets the sack, as they do, eventually. On the way out of the door, he has a word with HR and saves them all the head hunting by recommending a buddy in the City, ‘ideal’ to take over his job, highly qualified of course, and just happens to be a friend.

Well the guy duly gets the CEO role and calls the former boss to thank him, with a nice lush meal at The Ivy. They are sat chatting over the steak tartare and the Cheatea de Pernon and new CEO asks his mate, with all his great experience, what he should do when things inevitably get tough. The old CEO hands him 3 envelopes numbered one, two and three. “I knew you’d ask” he said. “Here you go, I wrote these when I knew I was about to get the sack. When things get tough open ‘letter one’. When things get tougher, open letter two and when the sh*t really hits the fan, open letter 3, but only as a last resort” he says. Well matey is chuffed, he thanks the old CEO for all his help, pays for the meal on the company credit card and off they go.

Six months go by, the new CEO is doing his restructuring but it’s taking longer than he hoped. Shareholders are calling in, asking when there will be a trading update and how things are doing. He decides to open letter number one. “When it gets tough, blame it on the structural issues being far deeper than first thought, say it will take longer than expected and there will be more write downs” it says. Great, he thinks – puts out a trading update, shareholders accept the reason and the calls stop coming in. Another 6 month go past and the shareholders are getting impatient, things still aren’t turning around as fast as he hoped and the AGM is coming up so he decides to open letter number two. “Blame me” it says “say the former CEO really was out of his depth, you have uncovered lots of additional costs and I had been far too optimistic” the letter says.

Great, thinks the new CEO, how selfless of him – so he blames everything on the previous “useless” CEO and the former board and says shareholders will soon see the positive effects of the new team by the interims. The shareholders reluctantly accept the excuse and everything calms down.

Well another 6 months go by and the interims are getting close, he’s really out of his depth, things are no better and he’s been scared to put out a trading update because he knows the share price will take a wallop. He’s really feeling the pressure and the shareholders are restless, He decides to open the last resort letter 3. He unfolds the letter slowly and reads it, it says:

“Get yourself some paper and a pen, and three envelopes”.

Have a very healthy and happy New Year to you all. Well donre Tim Martin for the well deserved knighthood.

P.S. Remember to enter the UK Stockchallenge for January and also the Annual Challenge too. Great fun, no prize, just kudos. No spamming, phishing or email harvesting – just traders/investors pitting their skills and luck v the rest of the crowd.

http://www.stockchallenge.co.uk/

Click ‘entry form’ at the top.

Rebel

Thank you. I hold Eurocell but I closed DLAR. I want to see ECEL's trading update to decide whether to increase or sell and add the cash into other existing holdings so it's a trade that could become long term hold.

Thank you Charlie - a very healthy and happy New Year to you too!