The Bumper Year End Rebel Review

New Year ‘OBIAY’ Naps: #OTB #CARD #BOOM #LIO #IGR #GDWN

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

OBIAY, before you ask = “One Bagger In A Year”

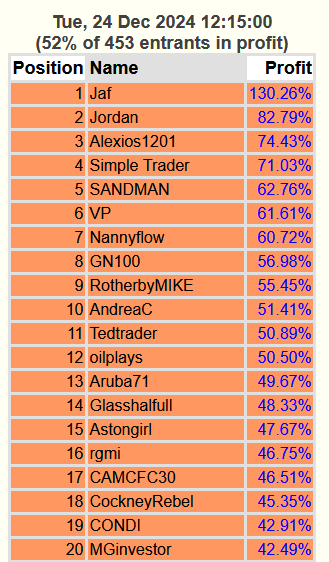

Another 12 months of my live has whistled by. It has been very interesting and another year of great experience and learning, every day is a school day as they say. My Substack subscriber numbers more than doubled from 1660 to 3500 and December 14th issue saw over 11k reads which was a record. ‘May you live in interesting times’ is the old Chinese mantra. It has certainly been an interesting year. When the market is tough, you become a stronger investor for the experience. At the very start of the year I was long Watches of Switzerland, WOSG. I took a real wallop when they warned and fell nearly 50% in 3 weeks, out of the blue, early in January, despite directors having recently bought shares and said they were inline. A 3% hit to the portfolio after I sold. That is no way to kick off a year! On the Beach, OTB slid for the fist 5 months so I sold half way through that 20% fall. Sometimes you know you can take a view but the market decides its doing something else and it is pointless fighting it or holding on in my opinion, if you are a pretty hands-on investor. I often prefer to let the market do what it is going to do, sell out and watch the move closely from the sidelines, and buying back when I feel more confident. I did that with OTB. Having sold out a little over 160p earlier in the year, I bought back recently on the results at a pretty similar price and kept adding. The price is up 40% since. WOSG I haven’t bought back yet but they are still lower than where I sold. I appreciate that if you are an investor with a full time job or someone not doing this full time then trading in and out isn’t as easy. I also doubt I’m much better off for trading in and out and just having the patients to hold. For me, if something is in a clear down-trend and I am watching it all day, and clearly there is nothing to change sentiment short term, then I can use the cash better by adding to something that has a lot more short to medium term momentum. It’s far more difficult to watch charts and understand resistance and support and just sit there and let a share fall while you do nothing. If an investor doesn’t watch charts so much then doing nothing and being patient is likely the best option. Perhaps the best way to illustrate this is my ukstockchallenge for 2024. I picked WOSG, AVON, MKS, OTB and RR. By Feb MKS and OTB were off 20% and WOSG was off 50%. The three together wiped 18% off my ukstockchallenge and I was sat around 340th out of 453 entries if memory serves me right. As we approach year end I am now 18th, up 45% and in the top 5% for the year, for having done nothing but watch. So there is a lesson perhaps.

Sadly that’s the last annual ukstockchallenge as Typo who has run it for over 20 years since the Hemscott days has decided to call it a day. He has done a fabulous job, it has been great pitching your skill against a few hundred others each year and very entertaining. The monthly challenge is carrying on till Easter at least so not all over yet if you want to have a go for Jan:

https://www.stockchallenge.co.uk/

Click entry form at the top.

Really, over all, trading out and back in on stuff hasn’t made much difference to my performance on these stocks, I might have been up or down a few percent either way. The only place I did gain was to use that cash elsewhere for a time in a market that was firm.

Hindsight is great. Over the past year I’ve had a great year as far as shares go. I ended last year (2023) up nearly 32% from the October low to December 31st. That was great and sort of left me thinking could I do 51% this year to October and maybe double the portfolio in 12 months? It actually was going pretty well up to the election where I was up around 42% for the year to date thanks in good part to Rolls Royce being 15%+ of my portfolio and up 60% by July. The real big driver though was CMCX which I bought late Dec at under £1. I went very heavy into these in Jan and Feb and by July my first purchases were up 200%. Great bowls give me confidence and this gad a great bowl followed by quick-fire positive updates. These made up 35% of my portfolio by March and doubled in 3 months. Funding Circle, FCH also made up nearly 8% of my portfolio and that more than double from Jan to July. In May I bought IGR @ 143p and in July sold them with the rest of the stuff when I sold right down, making over 50% in a couple of months. I bought them back recently below 120p so that has been one great trade amongst a lot of pretty average trades, some up, some down. That’s where the gains really came from. I also trimmed my holdings down to just 8-9 holdings. Concentrating the portfolio when great buys are hard to find, is something I like to do. With these couple of stars and such large percentage holdings I was up nearly 90% from the previous October and over 40% year to date by July. The election changed everything at that point, along with fear about the middle east and also the forthcoming US election. As the market started to feel weak, and with the sun in the sky, I decided to sell up 90%+ of my holdings and enjoy the end of summer more. I’d had an amazing 9 months and I wasn’t going to give it back when all I could see was negativity down the line. I couldn’t see any short term upside even if the market never fell. I’ve ignored these event in the past and regretted it, so the plan was to sell, watch and wait.

As it happens, the FTSE250 has given back 5% since July. The election has had a poor effect on the markets. However, the middle east hasn’t erupted as much as I feared and the market has come to realise that Trump is back as President and at least he is business friendly for the US and a known quantity after being a President 4 years ago. Harris would have been more uncertain. He looks like he will hit the EU with tariffs but we are out of the EU and I detect friendliness towards the British people from Trump, if not the government. I’ve been buying back in over the past month, 50% initially, heavily into IAG and more recently since their results, OTB who now form over 25% of my holdings together. I’ve given back around 7% having now bought back in even heavier over the past 2 weeks and am now over 90% invested. I have probably not saved much for trading in and out but what I did do was sleep a lot better knowing if things had gone dreadfully bad I wasn’t going to give my gains back – there’s a lot to be said for being able to sleep well, it has a value. I freely admit I’m a bit addicted to investing too – it’s hard to spot bargains like BOOM and be sat all in cash and ignore it. I’ve ended the year up roughly 34% as I write, just before Christmas, having given back the dealing costs to buy back in and having had a few that have come back a bit recently, offsetting a lot of gains from the likes of BOOM, OTB and IAG recent purchase. I also made just over 1% in divis, CMCX being the largest.

Going though other stuff that never went so well, I decided to sell Synthomer SYNT for a decent loss after they promised more and more and delivered less and less. Could have been great, may still be, but it has taken too long. I traded Luceco, LUCE a number of times, taking a loss or scraping the tiniest of profit each time. There was a number of other small duff trades, mostly offset by modest winners like FDEV, SAGA and others. I took a loss on CPI, no point trying to buck a trend like that. It now looks like making a bowly bottom so might be time to re-enter much lower than I sold out – do I want to though when there are lots of other great buys showing up?

Some that I was long before selling up, I have not bought back like GNC and FTC. Even if they are near highs I feel there’s betters foxes to chase now and I’ve been buying newly discovered potential OBIAYs for going fwd. FTC eps forecasts on Stockopedia seem to have been marked down recently.

That has mainly been all of the eventful trades and investing over the past year I think. Aside from holding CAR (reduced) and filling my portfolio with IAG mid November, just ahead of the break out, which are already up 35% after an absolute stream of large brokers upgrade – one cracking curve up on the chart:

Over the course of the year, I like to pitch myself v 2 indexes, the FTSE250 and the FTSE Small Cap Index, which is where the bulk of my investing is done. The FTSE 250 was up 4% this year, up until Christmas, as I write, The Small Cap Index up 6% approx. Without doubt, the last two years have been a stock pickers market in the UK, the likes of which I have never seen in 25 years. If you can find good stocks there’s great money to be made. If you have bought indexes or funds you will have likely struggled in most of them. It has been about finding the right stock in the unloved sectors where things have been aggressively sold down. I think it will be another similar year with a number of shares surprising to the upside when sentiment for shares has been so negative across the board.

News from the Christmas period

One I have multi-bagged in the past is Shoezone, SHOE. I wasn’t holding thankfully, when they put out a huge profit warning in the run up to Christmas. The co blamed Rachael Reeves’ budget, the rise in minimum wage and NI. I am sure this has had an effect and more so with SHOE as from my research their pay levels seem very low in the first place, compared to other retailers. I think Store Managers can earn as low as £17k or so, which doesn’t seem much for the responsibility.

The shares have been weak prior to the budget, in fact the shares have been sliding since March so it’s not totally down to Reeves. The co has been moving away from high street stores to ‘big box’ out of town stores. They have said there will be a number of store closures, I suspect these will be the poorly performing high street stores they have been targeting anyway and this has hastened the closures. These may be a great buy down here but timing will be key. I sold out before the peak in March in the twos, it’s tempting to buy back at nearly a third the price. I had heard rumours about a spat between the Smith brothers who run the co and own over 50%. The Brothers bought 1.6m shares in May 2021 @ 80p. They have had around 38p back in divi’s since. They have a hell of a lot of skin in the game and I’m not sure any row can take the focus away from the business for that long. They say “As a result, the Company now expects adjusted profit before tax for the financial year ending 27 September 2025 to be not less than £5.0m, down from previous expectations of £10.0m” At least £5m+ pbt is still a lot and 8p eps forecasts now for 2025 – you would hope with the Smith’s experience as a listed co now that they are guiding cautiously. I don’t believe people want to buy their shoes from China – have you ever bought clothes there? I have. A 3xl from China is a medium in the UK, it’s pure guesswork. You might be able to live with a top that’s a bit small perhaps but shoes are another thing. I would say shoes are pretty China-proof what with the disappointment and hassle sending them back.

Goodwin, GDWN posted some great results on 17th. I had bought into the shallow recent bowl a few weeks ago and added on the results. It’s in my nap list below so you can read more there.

Goodwin is extremely illiquid, volatile, and has a wide spread very often too so it isn’t the steadiest stock short term, you need to be prepared for frequent 10% moves, up and down, on a daily basis, on very little volume. Do your research – there is more info in the Naps below.

My Magnificent Seven Naps for 2025

As always, the shares I want to hold are those that have the potential to double in 12 months or One Bag In A Year (OBIAY I call them), if I can find them. That isn’t a forecast, it may not happen, but they have to have the potential to do it. If four of them missed by 80% and just one was to one-bag, the whole five would be up 36% for the year in total, that would be a decent miss to live with but hopefully they can do far better. Remember these are just my picks for me that I am highlighting. I know my risk v reward ratio, only you know yours. So please do your research and satisfy yourself that you know what you are buying and you are happy with the risk v reward you are taking on in any stock you buy. I’d hope to do even better by weighting my investment to the stocks I feel could do best.

Nap 1 = On the Beach, OTB. (OBIAY potential)

On the Beach is an online beach holiday, travel agent. An end to Covid saw an unprecedented resurgence in holidays by the UK public after being in lockdown for 18 months or so. People were taking 2-3 holidays a year or more. Inevitably that cannot keep up once paying for the holidays and the credit card bills rack up. But after a brief lull, unaided by the war in Ukraine, holiday makers are chomping at the bit once more. Pretty depressing news here and a lack of weather has also boosted the get away sector with IAG, CCL and Jet2 all hitting recent highs off of broker upgrades or co’s raising guidance. On Friday, 20th Carnival Cruises, CCL announced strong trading. IAG have seen 8 or more huge upgraders and JET2 has seen forecasts rising strongly.

What makes me like OTB ? Well they are way off their previous high and have been in dispute with Ryanair for selling Ryanair holidays without Ryanir’s approval. Ryanair were claiming OTB had to refund travellers when Ryanair cancelled flights and it was clearly Ryanair who where at fault. Ryanair lost the court case, common sense has now prevailed and the co’s are now working together. OTB have signed a “transformational partnership agreement with Ryanair, improving OTB's customer experience, simplifying operations and enhancing scalability.”

The dispute is over and OTB and Ryanair have made up, kissed and started working together. They have now also entered into providing holidays in Ireland. OTB describe this as a transformational deal and say the Irish market makes up the equivalent of 15% of the UK market for size. Initial trading seems to have been encouraging.

So having achieved 11.6p eps in 2024, they are forecast to do 17.8p eps in 2025 and 20.9p eps in 2026. That will be a trebling of earnings in 2 years to a record high, the previous high being 21p in 2018, when the shares were at a 455p all time high, allowing for 30% share dilution since. This performance is greatly improved and largely down to the new CEO Shuan Morton and CFO Jon Wormald who joined in early 2023 in my opinion. Recovery plays need to see tangible results from board changes in 9-18 months in my opinion and these two are delivering.

From the results on Dec 5th:

So this year, On the Beach are trading at nearly half the price they were trading the last time earnings were here which goes to show investor sentiment in the market in general, but this will change at some point and I believe OTB will rerate. With approx. £76m net cash of their own, not customer deposits, they are doing £25m in share buyback, about 6% of the co share which will also boost dilute eps by around 6%. Over the first few days of the buybacks they have been buying £1m worth a day nearly, they will have all the buybacks done before their Jan trading update at this rate. They paid a 3p divi this year, 2.1p in H2, I would expect the divi to rise in-line with earnings. The shares have curved up sharply.

Post Covid, I think people are valuing their enjoyment time much more highly and the sector is going to do well going forward, OTB looks like the prime beneficiary and growth candidate in my opinion. The last results on Dec 5th are well worth reading.

In short, the shares bottomed 18 months ago when Shuan Morton got the CEO job, promoted from CFO.

EPS :–

2023: 6.4p,

2024: 11.6p.

2025 18.1p forecast

A ridiculously low PEG falling from 0.8 this year to 0.4 next year (Stockopedia) I make it lower still.

A 3p divi xd Jan 31 (2.1p final divi)

Very strong earnings growth on a PE of 13. Order book up 25%. £25m buy backs currently being done (6% of the co shares approx.) at a rate of £1m a day will increase eps 6% in addition. £76m net cash, unincumbered with a further £108m customer deposits ringfenced. Earnings set to have risen nearly 200% in 2 years. Currently valued far more conservatively than in the past.

19p+ eps this year after the share buy backs? Near record eps and share price half where they were when doing 21p eps 6 years ago. Has a somewhat Jim Slater Zulu stock feel under the new management imo and has most if not all of Slater’s zulu requirements..

Next trading update end of January

Nap 2 = Cardfactory. (OBIAY potential)

Cardfactory has been a long term on and off investment for me. I’ve never lost faith in the business, I think it has one of the best CEO’s in the country. I have sold out though on a couple of occasions. Having averaged in around 60p I sold a year or so ago while Teleios, a major shareholder with over 20% relentlessly sold down every time CARD neared 110p. I bought back when Telieos were completely out and the shares then rattled on up to 140p+. I sold out again in the last trading update when CARD announced interims. Again, I didn’t think there was anything wrong with the results, H1 was expected to be weak on cash and earnings as there were a particular high front end cost for current asset build up which would get paid back in H2 but the market just didn’t believe it, even though CARD said they were inline. Current assets were up nearly £7m, that likely had a retail sales value 3 times or more if it was a stock build for H2 sales. CARD sold off massively from 145p down to 80p but sometimes markets can be very irrational. Brokers have not reduced forecasts and having sold out, I just waited for the shares to look like they had bottomed and so I bought back in around 90-93p as it made a bowly bottom. A few days later the company put out news of a nice acquisition of Garven Holdings, a card and decoration supplier in the US for a sum of $25m out of existing cash and debt facilities. These have never been a sell since Covid in my opinion, I suspect many like me just felt if everyone was selling why stay in there?

More interestingly, they also said trading was inline. This is interesting because broker forecasts have never been reduced since the interims, in fact UBS had put out a very bullish note on CARD with a 163p target. I believe the market just panicked due to general low confidence in the run up to the Reeves budget and CARD has a big private investor following, a lot of whom don’t research what they are holding/buying. Since the update the CFO has bought 21k shares and the CEO bought 49k shares. This business has amazing cashflow. Being vertically integrated, they design, print, manufacture, distribute and sell the cards themselves either as retail or as wholesale to the likes of Aldi exclusively throughout UK and Ireland. This means their margins are way higher than any competition who either print and manufacture cards for others to sell or who buy in cards to sell retail.

Current forecasts are for eps of 14.4p for the year to Jan 31 and 15.9p for 2026 year starting Feb1. That’s a PE of 7.3 falling to 6.4 and a forecast yield of 4.9% rising to 5.5%. This seems crazy for one of the best retailers on the high street who excluding leases, had net debt of just £34m at the year end. I expect that to have dropped a lot more still at year end, excluding the fact they have just made an acquisition from cash. I think these could possibly give a huge wake up call before too long. I think the co has been a victim of circumstances, a large shareholder sell down and a complete misunderstanding of the results by investors. We will see how big a wake up call there is but I think these have the potential to one-bag in a year.

CARD have also been revamping all their stores which brings in higher footfall and they have just gone from supplying 500 Aldi stores with cards to 1000 in the UK, on an exclusive basis. This will all be in place before Christmas.

Here is the CARD chart – they were doing 19p eps and a 9p divi at that high. The year starting Feb 1 they are forecast to do 15.9p eps and a 5.7p divi. They are not far of record earnings and yield but they are trading at a quarter of where they were when they did that.

There has been next to no share dilution.

When the market wakes up to the cash generation here and what they can do with it, like buying Garven this month without issuing shares, and these acquisitions boosting earnings going forward, then I suspect there could be a huge bun fight for the shares, hence this is still one of my favourite stocks.

And that is the point, if you are organically growing earnings at 10% say, but you generate so much cash that you can buy in more earnings with acquisitions which don’t require more shares, it all gets a bit strong and exciting possibly, as things compound. There is a free Edison note to read here where the make the case for a £2 share price based on a discounted cashflow model https://www.edisongroup.com/research/confident-on-fy25-outlook/34019/.

Next trading update mid January

Nap 3 = Audioboom, BOOM (OBIAY potential)

Audioboom is a Jersey-based podcast publisher. The Company’s advertising business is a scalable content business that provides commercial services for a network of 250 top tier podcasts, with key partners. The company website says: “Audioboom is a leading global podcast publisher. We connect podcasters and advertisers with engaged and passionate audiences.

We make podcasts accessible and profitable for podcasters, advertisers and brands by combining technical support, production savvy and ad sales know-how into one user-friendly, economical experience.

Advertising: Podcasters meet advertisers! We match top talent with advertising agencies and brands, helping them take advantage of the unique benefits offered by podcast ads. Whether it’s host read endorsements, dynamically inserted ads, sponsorships or branded content, our ad sales team manages the process from beginning to end.

Distribution: Listeners want to access and discover podcasts on the devices and platforms of their choosing, which is why we partner with leading distribution platforms and streaming services. Plus, our sleek embeddable player allows podcasters to share content on their own websites and via social media

Production: In addition to hosting, distributing and monetizing content, our studios in London, Los Angeles and New York produce original content for the Audioboom podcast network and as part of bespoke production deals with well-known personalities and brands”

Podcasts are increasingly popular and very easy to listen to a podcast while working, I listen to more and more. Substack offers the ability to podcast as do many other platforms. Audioboom make it easy for people to monetise their podcasts, they simply use the Audioboom platform and accept they have ad breaks during their podcast that Audioboom provide. You use Audioboom to podcast and when you want to be paid you hit the button to monetise, rather like Substack. Audioboom provide all the ad content that is appropriate to your subject matter. So it’s all very simple for the users and probably the reason why Audioboom are the leading podcast company in the US. It is easy to see how scalable this is and how fast for BOOM to generate revenues. This is a pretty simple model to understand. I am not a fan of tech, someone tells me that a company has a unique AI plug in cloud generated app specifically for algorithms of a certain type that will do this and that……………….snooze! I don’t understand all the geeky stuff, I don’t understand the competition out there for the geeky stuff either. Important to me is understanding an investment to a decent extent so that when the shares fall I can look for what has caused it and assess how serious it is to the company. Audioboom is pretty simple to understand. They get very high popularity ratings and distribute to audiences globally on Youtube, Spotify, Pandora and Apple Podcasts. I’m a tad out of my com fort-zone compared to retailers and the like but the recent improved performance means I cannot ignore the potential and it really is easy to understand as a media enabler with a simple, low cost model. Audioboom saw a huge spike up during covid when podcasts took off They signed up to some onerous long term contract that have become an albatross around their neck but these contracts all end in December. From then on their margins should escalate. It is already starting to show in the numbers imo.

In H1 the co reported $34m revenues and EBITDA of $0.3m. By Q3 they had done $52.9m sales ($18.8m in Q3) and EBITDA of $1m. Since then they have posted two ‘ahead’ statements and say EBITDA will be at least $3.1m, that’s $2m+ EBITDA in Q4 alone. With $3.96m EBITDA forecast for the year ahead, that seems very conservative having done $2m in Q4 and all the onerous contracts out of the way from the start of the year, even if Q4 is their biggest quarter.

Michael Tobin, Chairman, has been a constant buyer from the high, regularly averaging down with circa £10k+ fortnightly buying. I am focussed on sales growth and increasing margins and the pace at which that happens, which I think could be very firm with the onerous contacts coming to an end. Broker forecasts have doubled this last 10 days, the current year from 2025 from Jan 1st is 18c eps, more than doubling from the 8c forecast in September. That makes a PE 25 for the current years. For a business growing eps at 100% and with earnings forecasts likely to be raised as the year goes on, that looks very good as a valuation imo, especially if this sort of growth or something like it is expected to be maintained for some time in my opinion.

Next trading update mid January

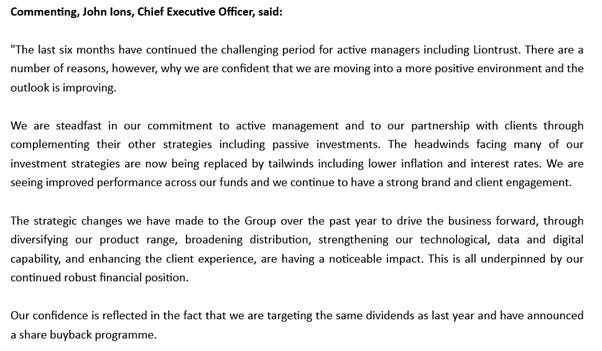

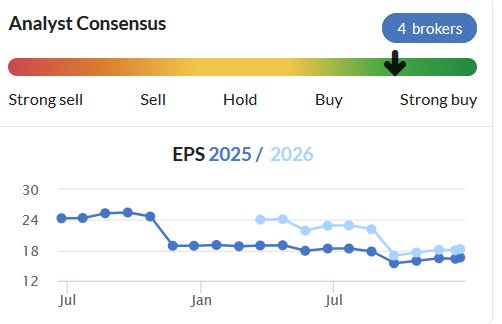

Nap 4 = Liontrust. LIO (potential OBIAY).

I rarely invest in investment co’s of any sort. But Liontrust is so cheap I cannot ignore it. It has a PE of 7.3 and a yield of 15.3% at a share price of 469p. It’s a simple question – can they maintain that divi?

If they can then this is one of the cheapest co’s around. At the interims the CEO said this:

Immediately after these results the CEO bought 100k shares for £450k. The CFO bought 50k shares for £225k – not inconsiderable purchase.

The company presented on investormeetscompany and said they had the ability to maintain that divi for a further 18 months. So will the market improve within 18 months? The company seem to be saying they are seeing improvements, the CEO and CFO have voted with their pocket. The dilute eps will be enhanced by nearly 2% from the share buybacks too. All of that seems uber-confident and if things do improve and that divi is maintained, the shares are going to rerate rapidly and drive that yield lower as punters snap up 15% income that looks secure in my opinion. Less than 10% dilution since 2020 making that previous high around £22 allowing for the dilution. Where can they get back to when this stock is no longer hated? I like buying the hated.

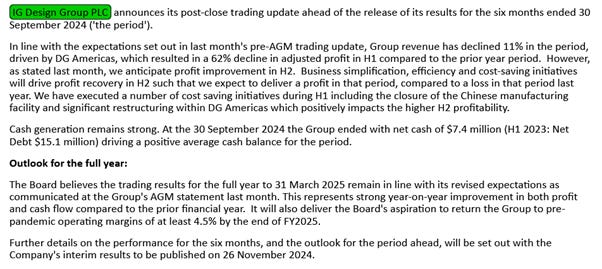

Nap 5 – IG Design, IGR (potential OBIAY).

When to buy a recovery play? Well I always think it’s when a stock is hated and IGR are currently hated at the moment in my opinion.

IGR design, manufacture and sell Christmasalia, if there is such a word, like wrapping paper and Christmas ‘stuff’. I bought these 20 odd years ago when they were 30-50p and they became a cracking investment under the stewardship of Paul Fineman, the then new CEO. He ran the co very well and expanded it exponentially but when he sold out in 2019, that was the cue for me to sell too. Integrating all of these divisions has proved a bit challenging to say the least. The shares tanked from £8 in 2020 to 48p in May 2022. In Feb 22, after a big profit warning, Fineman left abruptly, after 17 years, and has been group CEO for the past 14 years. In May 2022 Paul Bal was employed as CEO and in July Rohan Cummings as Chief Financial Officer.

Paul Bal

https://www.linkedin.com/in/paul-bal-a2630391/?originalSubdomain=uk

Roham Cummings

https://www.linkedin.com/in/rohan-cummings-a644144/?originalSubdomain=uk

Both seem very experienced.

They seemed to have things coming into good shape by June and the shares had risen 300% from the low but they were hit with problems in the US with DG Americas and warned with the results in October:

You can read that for yourself, it’s a case of do you believe them? The shares have come off £1 to 133p and forecasts are now for 16.5c eps, around 14% lower than April while the shares have fallen more than 40% from the high. Watching investormeetcompany recently, the directors seemed very confident of forecasts going fwd and hitting them and laid out in the Q&A why they were confident. They have net cash of $7.4m v a net debt of $15.1m last year.

In 2020 they had sales of £624m and operating margins of 4.6% making 32c eps.

Sales this year will be 20%+ higher at $763 so saying they will get back to 4.5% margins would likely mean they would do circa 30c eps or more going fwd, seeing there has been 20% share dilution since, versus 18.2c forecast for next year.

Brokers have been tweaking up consensus earnings too since September.

Getting back to 260p a share doesn’t look a tough ask if they deliver, so there’s the OBIAY potential and more in my opinion.

Taking into account the share dilution the previous high was around 640p

Nap 6 – Goodwin, GDWN – (outsider OBIAY potential)

From Jan 2023 to Jan 2024, Goodwin nearly one bagged. From the start of 2024 to the results this week they were up just 10%.

From July 2017 to July 2024 they nearly rose 6 fold. If you had bought these at 60p at the turn of the millennium they have 100 bagged. Goodwin is a fantastic family owned growth story. I bought then at 140p in 04 and held them to £14 in 2008 to 10 bag them and it pains me to look back. Investing is about timing though and since selling GDWN the money has gone into lots of good multibaggers so I can’t feel too sorry for myself. This is a growth stock hiding as an engineering conglomerate in my opinion. They have several divisions. They provide casting materials, they cast and engineer huge check valves that prevent backflow, in fact they are one of the few companies that can cast and engineer to this size and standard. They have 23 companies in total making slurry pumps and making casting powders for jewellery to large engineering. They make vermiculite and perlite for gardening and insulation and other stuff ending in ‘ite’. Easat Radar Oy Finland make radar system and is one of the more exciting divisions. This has, after a long time, got into profitability and seems to be gaining traction. The most exciting division they have is their relatively new business they have developed themselves with a lot of investment, Duvelco Ltd. Duvelco produce specialist Polymide Polymers under the name Ducoya. Goodwin invented Ducoya. The company says “Ducoya’s strong, technical performance lends itself to versatility across a wide range of applications. These include wear and friction performance, high temperature performance (>400°C) and exceptional purity; Ducoya is also highly durable and has an excellent strength to weight ratio and toughness.” The properties of these polymers are unique and perform with strength at high temperatures and are likely to get strong demand from the Automotive, Aerospace and Semiconductor industries. This looks currently like a world beating product.

Another exciting part of the business is their firefighting products. They manufacture mortar for buildings, coatings for materials and other products that aid fire-proofing. They also have developed a fire extinguishing filler for extinguishing lithium battery fires and while there is some competition out there, Godwin’s claim theirs is the best.

Goodwin posted interims on the 17th December. While sales were up 9%, earnings were up 30% to 155p for the interims. Having done 224p eps last year and the company saying H2 sales look set to be at least as good imo:

There are no broker forecasts but if I was to double H1 earnings they look set to do 300p+ eps. Taking into account Duvelco can now produce Ducoya on an industrial scale, Easat ‘coming into fruition’ and the fire extinguisher business looking a bit sexy too then the real growth drivers of the business look like they are starting to fire on all cylinders in my opinion. I have waited for the right time to go in with a serious investment, the bowl on the chart said ‘buy’ to me a few weeks ago and I doubled my holding after the interims. If they do more than the 310p eps I’m guessing at this year then next year’s earnings could be seriously higher in my opinion, putting these on a PE way below 20 perhaps, and one that has frequently one bagged in a year. Goodwin are a share to buy when earnings haven’t been so raunchy and to be long when these huge growth spurts happen in my opinion – hence I’m long.

No share dilution at all in the last 5 years, in fact I doubt there has been any dilution in the past 25 years and just 8m shares in circulation so it is very illiquid, often has a wide spread and can be volatile. All the directors have big holdings.

25 year chart.

1 year chart.

Volatile and not easy to trade, do your research and draw your own conclusions.

NAP7 Avon Technologies (formerly Avon Protection), AVON (outside OBIAY potential)

Avon Technologies are a defence company, pure defence, they make product that save lives, not offensive weapons. There’s 3 main lines, biological masks, helmets and rebreather apparatus.

CEO Jos Sclater and CFO Rich Cahin took the helm at AVON in Jan 2023. They took over after Avon had had a disastrous foray into body armour, buying the division from 3M and having several major testing failures which caused the business to be closed and a loss of $100m+

Sclater and Cashin have great experience having helped run GKN and Ultra Electronics, both being taken over at good premiums eventually.

Avon has biological masks which form very large, lumpy orders but the lowest margins of the business. Helmets are much higher margins and then there’s the rebreathers which are relatively new but gaining traction. Rebreathers allow divers to stay below water longer by recycling their air.

The whole basis of the investment is a recovery play. In the US they had factories that were competing with each other and not talking to each other when Sclater arrived. Since then he has closed a factory, moved all the production elsewhere in exiting factory floorspace in the US an improved production automation and efficiencies. He has put all the divisions and factories through numerous kaizens. The shares bottomed 6 months after Sclater arrived and from that bottom they have doubled in the past year.

Sclater says he’ll get the business back to mid teen operating margins.

In 2019m Avon did 109c normalised eps on $164m sales with operating margins at 7.7%

This year they are expected to do $291m sales. If Sclater gets to his mid teens margins that would represent a near doubling of sales and doubling of margins on their 2019 performance and should translate into far higher earnings than the 109c in 2019, bearing in mind there has been no share dilution.

The 70c eps forecast this year and 98c forecast next year look like they could be very conservative and earnings forecasts have risen nearly 10% since September:

The shares are trading at around £14,70 a share, compared to £24.50 they traded in 2019 and way below the £46 high of 2021.

Avon have an AGM, trading update and presentation on investormeetcompany.com on January 31st. The chart has been making a bowl and breaking out this week.

Helmets look set to have a good year, rebreather are picking up in sales following several sub sea cable attacks and bio masks are moving close to the next replacement cycle.

On a PE of 26, they may not look especially cheap but I think with a decent beat and the company moving from defensive and repair actions to more aggressive growth and domination of the markets they are world leaders in, the growth could be moving into an exciting phase.

This year could be more special than in a long time imo.

All the above naps are just stocks that I like and find attractive. They are not tips. As I hold them I am obviously biased and likely not to be as objectives as I could be so please do your own research and make sure the risk is right for you if you do invest in any of them.

I’d like to say thank you to everyone that donated to my village fund from the last issue, it’s nice to know some appreciate the work involved here each week, and encourages to keep it going. I discovered a while back that every bit of time it takes to natter is lost time to research so it’s getting a happy balance.

So that’s just about the year that was. There won’t have been a lot of news between now and next weekend so next weekend I’ll try to highlight the top bowls for the start of the 2025.

Have a great fun-packed, healthy and happy New Year.

Rebel

rebel@cockneyerebel.uk

Twitter @rebelHQ

Hi Stephen,

I wouldn't read too much into that, I think the director buys says more about what they expect than their words myself.

Have a happy and healthy new year and all the best

Richard

Hi CR,

A very humble analysis and report of your performance over the last year. It’s easy to think that professional investors and writers are always right and always successful. But, as you point out, that’s not the case! It’s about being correct and successful more often than not. And reversing that position quickly when things don’t pan out as you expected.

Regarding #OTB,

I’ve just come back from a week in Lanzarote and there were lots of empty seats on the EasyJet flight. The holiday was booked as a package holiday with EasyJet, who seem to be one of the cheapest when Googling a holiday. Although I do like the figures from #OTB.

#CARD,

I did look at the possibility of buying some before Christmas but had a lack of funds. It’s one I like and the US acquisition makes it look even more attractive. Some commentators on Stockopedia have also noticed early in December that they had sent shipping containers to the USA and they were trying to work out what the container weights would equate to in stock?

#BOOM,

I like this one and it’s one of the favourite holdings of the fund manager of ‘Onward Opportunities’ a very successful (last year) fund who also had a good holding of #WNWD and talked very favourably about them on VOX with Paul Hill recently, before they got taken out just last week! +70%

So all in all some good ‘food for thought’ from yourself! Some stocks I will do some more research on.

Hopefully you had a good Christmas and you’ll have a Great and prosperous New Year!

p.s,

How’s the collection going for the local Village Hall?

Take care and be lucky!

Gramwell.