June Stock Market - not all midsummer murder

June 21st, 2024

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

Well at last the sun is out and summer is starting to feel something like it should but will that spill over into the stockmarket? We need the weather because the football isn’t much relief from these slow markets. I thought everyone had come to terms with the fact that Labour were going to walk the election but the last few weeks feels like investors have only just woken up. It feels to me like we are at an inflection point, get the election out of the way and get the H1 trading updates. This week we have started to see the trading updates start to hit the wires. Synetics, SNC posted a $10m contact win and saw the shares rally 10%, back up to the recent highs. After a strong Tuesday with good volume, Weds was a bit slow with low volume and the market was more on tick over with the US closed. We rarely follow the US these days so why punters were on hold beats me. A bid approach for BVIC also shows the the sharks are circling- I think that will pick up after the election when buyers can have more certainty.

Wednesday saw the inflation data released:

The stand out was inflation measured by CPI was now 2%, hitting the BofE target and back where we were before Ukraine. PPI input and output month on month were also in-line to below expectations which bodes well for CPI going forward. The market chose to ignore the news with the FTSE250 off in the morning but the market is clinically depressed, it has been programmed by relentless press gloom about the election, the weather, global warming, the end of the world as we know it. If you let that lot control your thought process and over influence you, then you’ll miss the bargains in my opinion. Here are two examples where great stocks push on through any market sentiment – RR. and W7L.

Rolls Royce up 600% from the October low.

Thurs: GOLDMAN RAISES ROLLS-ROYCE PRICE TARGET TO 545 (524) PENCE - 'BUY'

Friday evening: JEFFERIES RAISES ROLLS-ROYCE PRICE TARGET TO 580 (530) PENCE - 'BUY'

Warpaint London up 400% since the September low.

Both of the above shares have been hitting new all time highs in the past week or so. Some co’s with real strong growth are bucking the market well but as an investor, the only way you are likely to buy and hold and not scalp way too early is if you know the company well through researching it and being confident. These just happen to be two I hold, I’m sure other investor have examples too. Remember the old adage, ‘let the trend be your friend’ in my opinion.

The FTSE250 is just drifting, slightly higher but no real momentum. I can live with that, there are winners to be found by stock-picking.

The Smallcap index is mirroring it, and also a bowl, so a lot of treading water but a lot of upside surprises out there imo.

Warpaint London, W7L. At the recent presentation to the US, CEO Bazini said they will have a small trading update with the AGM. The current forward PE for 2025 is 23. That may sound a bit racy but bear this in mind. Brokers are forecasting 18% sales growth. W7L did 28% in Q1.

Operating margins are growing with scale here’s the last 3 years operating margins:

7.63, 12.4%, 20.6% - the co says margins have improved.

Growing faster than “Eyes/Lips/Face” or Elf as it is called in the US, a very similar budget cosmetic co, ELF trades on a forward PE of 54. W7L would make a great earnings enhancing bolt on for ELF and have started trading shares out there which will draw attention imo.

That aside, a PE of 23 for earnings growth of 50%+ is great value for a debt-free co – and a PEG of 0.5. Watch out for the update imo. The AGM and trading update is on 26th June, - Wednesday.

Games Workshop also posted a trading update ahead of expectations. On a PE of 20 and a 4.0% yield, the Amazon licensing deal that is in discussions doesn’t look priced in here to me – another class act. JEFFERIES RAISES GAMES WORKSHOP PRICE TARGET TO 11850 (8700) PENCE - 'BUY'

GAW have doubled earnings in 5 years, they have net cash of £62m. I think for a business that has had such constant earnings growth, a PE of 20+ is reasonable, especially with a yield of 4%.

It is now 18 months since the company said it had an “agreement in principle to develop film and television productions”. On the current rating, nothing is being priced in for Amazon or next to nothing imo. I have taken a small position as I think any Amazon news could make them a one bagger in a year’ OBIAY.

Games Workshop, GAW.

How long do you invest in a stock? What makes you a long term investor rather than a trader?

Holding a stock for over a year for me is a long term hold but it has to be rather special to get there as far as growth goes. MKS managed to one bag in a year but the chance of it doing that again over the next year looks unlikely so I took my profits there (holding a few still) and put the money into stocks that I believe can double in a year still. That doesn’t make it a poor investment, I just feel I can stock pick well and find faster growth in other holdings. So for me it’s a constant watch and evaluation. As stocks look longer in the tooth I want to start reducing and using that cash to increase existing holdings that I feel can grow faster. That might not be right for investors who cannot stock pick so well are just don’t want the hassle. I try to increase in a stock that I have researched well and feel confident of, when I think punters are bored. Stocks that race away get punters excited, but punters also get bored quickly when they see other stuff rising, we all do to an extent. Trying to realise when a stock is at ‘peak boredom’ is a skill it takes years to acquire and which you never achieve fully, and always get surprised by. When everyone around you are feeling negative, it’s hard not to be swayed in my opinion, just as it’s hard to sell out of a stock when everyone is salivating and buying it. Investors and traders are herd animals, we love to all run in the same direction at once. The problem with that is that when one is wrong, you’re all wrong, and so the reaction to disappointment can be large in the wrong direction too. If you are the lone bull when the market turns bullish, or vice versa, you collect the big win. So I know I might get accused of being a perma-bull, but I’m not, I do my research and commit to a buy where I think I’m right and the market is under-estimating a stock. You don’t have to be right all the time, just most of the time – and very right if I can be. I accept one or two might not go to plan but that’s fine, I just try to keep the ones I’m least confident of in a smaller position. Doing your own research is the only way you can be confident enough to say “ I think I’m right and the market is wrong”. If you don’t do research you just have to go with the crowd and you’ll rarely get those big, life-changing gains imo. I keep re-evaluating all stocks I hold. It is too easy to become ‘comfortable’ with a share and take your eye off of what the potential gain could be for the risk involved.

The one advantage you have as a private investor is the ability to be nimble. Fund investors have to buy such large stakes they cannot open and close positions at will. Most private investors can, the average investor can decide to buy a stock in the morning and have a full position within the day, the same goes for selling in most instances. This makes it far easier to be nimble, to get in and out, to reduce sizeably or increase. Big holders cannot wait for what looks like the top to sell, they have to sell size so they may trim on the way up, private, smaller investors can hang in their longer. It is worth remembering this and using it to your advantage – you don’t have to hold on for a year if you buy a stock and it isn’t illegal to sell at a loss and make the loss up in a different stock. This is why I tend to run winners and sell losers.

One thing I did notice this week was Cardfactory, CARD, a past holding of mine and former one-bagger. They are now trading on a PE of 6.4 falling to 5.8 and a yield of 6.3% rising to 7%. That looks just way too cheap now. By full year 2026 they are expected to be net cash ex leases. They have done all of this while dealing with a huge rise in the living wage which I estimate cost them £6m p.a. Having sold CARD, I have always said Darcy Wilson Rymer is a great CEO and the only thing that made me sell was the fact there were better opportunities elsewhere and Teleios seemingly determined to sell. I think on this valuation though, Teleios will likely get taken out by a large investor. Next update early August. Punters seem to be bored in CARD now so I might take some shares off them cheaply I suspect. The Edison note on Research Tree this week drew my attention, worth getting hold of if you can, you should be able to get hold of it on their website if you register for free:

https://www.edisongroup.com/

Dunno if I want to add a new position, I’d sooner increase what I already hold I think, but never say never. If it firms I may buy before the next update.

Thursday kicked off with a couple of great updates for me – the first was CMC Markets, CMCX

These were 23% of my portfolio going into the results, my largest holding. The results were fabulous in my opinion.

I give this one a

These are just the summary, I recommend investors read the whole of the results. I noticed a couple of tweets saying these looked expensive – clearly those who thought that never realised all the earnings cam in H2

Basically the 16.7p eps hides the fact that they lost 0.8p eps in H1 so they have done 17.5p eps in H2. The business isn’t seasonal so no reason why they shouldn’t do double this eps in the full year ahead. But there is more, this year they will save £21m from cost cutting and job cuts which will boost margins. I pointed this out here a couple of weeks ago but the earnings are actually higher than I estimated.

Another thing to notice is that sales in H1 were £122.6m. Total sales this year were £332.8m. So they have done £210m sales in H2. Today the co raised sales guidance to £320-360 million in FY25 (Sharepad were forecasting £313.8m, Stocko had £329m). That’s a very cautious guidance having done £211m sales in H2 so I expect this to get beaten, the company guides very cautiously. All in all I can see 50p eps for the year being quite possible. I don’t think any of this is rocket science, no degrees in finance required, you just need to spend a bit of time studying trends and H1 v H2.

The company paid 8.3p divi this year and they will pay out 50% of pbt in divs. If they hit 50p eps then the divi could be around half that at 25p perhaps, 8% and soaring earnings growth. CMCX have been through massive investment to move into B2B. They have just signed a deal with Revolut and in the presentation on Thursday they said they were close to a deal with a large far eastern financial institution.

There has been massive cost cuts in this business and much higher sales which all adds up to much greater profits and higher yield imo. Operational gearing is high. Yet another flier on results, these rallied 13% on results day, with 300% normal daily volume.

I posted this bowl chart on Twitter on January 3rd showing the bowl forming:

Just to illustrate how big and fast bowls can follow through, 6 months later these have nearly 2 bagged.

I continue to hold and have added on the results – the stock goes XD on July 12th for 7.3p - our wedding anniversary – so that’s spent for me already then 😊

I’d say go onto the CMCX website and watch the recording of the results webcast if you never caught it live, and don’t miss the opening from Peter Cruddas imo.

A taster from him

“Am I retiring? No”

“I have never sold any shares and have no intention of doing so”

“I have a lot of skin in the game and I am aligned with shareholders”

He sounds as driven as ever imo.

WARNING – CMCX is my largest holding – of course I am biased, I’m going to say all of this. You won’t know if it is hype unless you do you verify anything I say. I can also just get stuff wrong, so please do your research.

Lazy investors make lazy returns. My current plan is to sell half my holding when they hit £5 in 6-12 months. Never any guarantees as life isn’t a pre-ordained set of happenings but I’ll hold and see.

Next trading update in July with the AGM.

On Thursday *RBC raised their target to330 (240) pence - 'OUTPERFORM'. I expect more and bigger upgrades.

There was a good article I found on Thursday with Peter Cruddas, he believes the rating is way too low and says he may take CMCX to the US in a year or two if things don’t improve here in the markets.

https://www.telegraph.co.uk/business/2024/06/20/lord-cruddas-london-investment-firm-america/

This stock should now trade on a fin-tech rating and it isn’t, but I believe it will re-rate eventually.

"It is going to be an exciting couple of years." It isn’t me saying that, it’s Peter Cruddas in the results outlook on Thursday.

Hopefully some others out there have done their research and were holding.

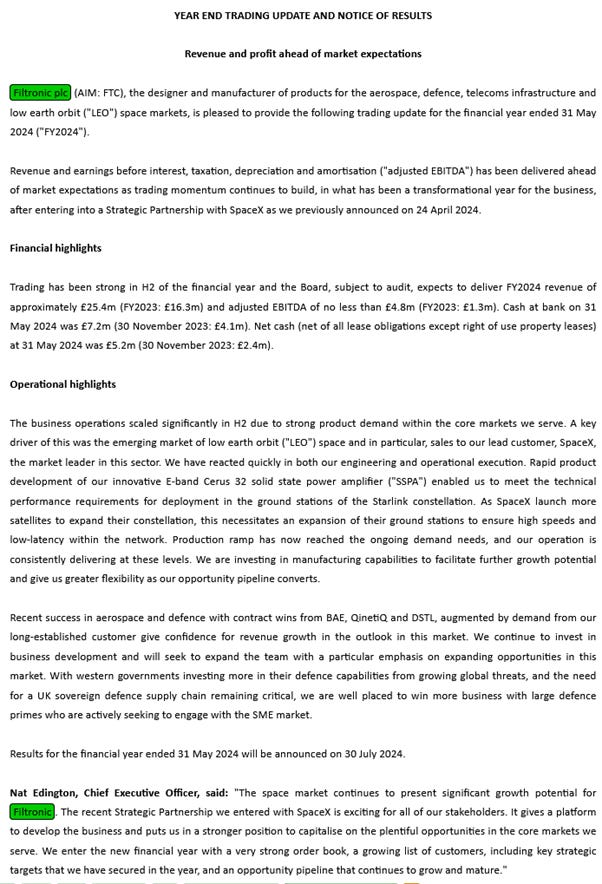

Thursday also saw a trading update from FTC, Filtronic. Filtronic are leading Radio Frequency engineers and this has come to the fore recently both for satellites, base station and defence. Satellite base stations need to increase, meanwhile satellites eventually fall out of ‘Low Earth Orbit” and need to be replaced. All of this has FTC as one of the few highly skilled specialist tech businesses in a sweet spot. Defence co’s like BAE and QQ. are more and more reliant of RF too – both these divisions have far better margins than the mobile phone antenna business.

This was a further 10% upgrade to EBITDA and I would assume will add around 10% to the current EPS forecasts. The real thing is the greater sales will likely generate much greater margins going forward from SpaceX and Defence which command much higher margin business and that’s where the sales growth is coming from. I continue to hold, the co is in the right place at the right time and I think forecasts will get raised as we go through the coming months.

For me this is a small cap tech with barriers to entry and the worlds top space company as a major customer who has taken a share in the co via warrants. They are net cash, they are growing (from a low base) eps by around 600% this 2024 and forecast to grow eps 100% this year (2025). I expect eps forecast to rise near to 3p this year giving a PE of 23 for growth of 100% but it could be far more.

£24.4m sales for 2024 just ended, £35.6m sales for 2025. I think the operational gearing will mean 3p eps is very conservative, especially as the rise in sales will be down to a big growth in higher margin business.

EPS forecasts have grown 400% since January to 2.7p.

July 2023 £3.2m contract with European Space Agency

September 2023 £3.4m contract with SpaceX

December 2023 £4.5m Defence Contract win

December 2023 £4.8m SpaceX Contract win

January 2024 £2m Qinetiq Contract win

February 2024 £7.8m Spacex contract win

April 2024 £15.8m SpaceX contract win.

I make that £46m in contract wins that most should complete in 2025. That excludes smaller contracts that don’t get RNS’d

Brokers are forecasting revenues of £35.6m in 2025

Would this tech be trading below £1 in the US?

Next up for me will be IG Design, IGR – with annual results on Tuesday, and an Investormeetcompany presentation. There has been some big broker targets recently. This week the stock has made a new 30 month high.

With a new board led by Paul Bal, the outlook will be interesting to see. They managed 40c eps on sales of $588m in 2019, this coming year, 2025, they are expected to do sales of $829. If they can get margins back to where they were these could be very cheap even with the 50% dilution over the past 6 years. We shall see.

Friday proved to be a dull day for news again, as it and Monday usually is, next to no real news at 7am.

And so that was my week, with Thursday being one of the best days I’ve ever had percentage-wise, up just over 4%, With a 2% rise at the start of the week, that was 6% across two days, making up 4%+. I had given back in the first two weeks of the mont and was down 0.4% on Friday. That’s the sort of volatility I’m used to having with just 15 or so OBIAYs in my portfolio, but as long as the trend is strongly upwards I can ride the volatility. Only trading I did this week of note was to add more CMCX, buy some GAW and reduce some SYNT. I don’t know why SYNT has been coming off but as a large position I felt the need to play a bit safe. Update in July, I can reassess then.

So it’s been a good week but the hardest thing to do is not snatch short term profits. Your carrots never grow to prize-winners if you are forever pulling them up and replanting them.

Remember this is all just opinion and not advice - I am biased, I am talking my own book so you need to do your own research and know your risk profile.

Have a great, sunny and hot weekend hopefully.

Yes, if any license deal gets announced with Amazon imo. They have been talking for 18 month. The valuation has had good support just under £100. There is obviously something priced in for Amazon but any deal is 'think of a number' imo. Of course it may take more than a year to agree from here or it may not happen, so there is downside risk but I think with a 4% yield going fwd the downside seems limited while the upside looks potentially multiples of any downside.

Kids won't just 'stop' playing the games now either so again, there's a decent floor imo.

Just my opinion- if I found a 'certain' looking OBIAY elsewhere I might be tempted to use the cash I have in GAW to buy that instead but for now it's a speculative OBIAY with limited downside risk imo.

Hi Stephen, thank you.

With FTC it's growing larger contract wins and they are all on much better margins in satellite and defence so I think short terms took profits despite the earnings upgrade but really, any big upgrades are likely to comer in the coming year in my opinion.

SYNT - I just don't know. I noticed last night the consensus epd forecasts have been dropping a bit for this year but that may be due to the divestment in may and brokers tweaking their numbers, with 9 brokers covering it on Stocko, it only takes one or two negative brokers to lower the consensus. I am sure punters could have misread that slight fall or just got bored and been selling because the likes of CMCX, IGR and others have been motoring and they want to chase the racers. I am unsure, so it just seems wise to reduce for now until I see the update in July.