Weekend Rebel Review Sep 30th

Markets and Card Factory thoughts

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, Everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.Well the rain has killed any hope of doing anything meaningful outside today so time for a weekend review again this week. There’s a fabulous feeling about the market currently imo, tho many may not feel it. When investors/traders sell off just because they cannot take anymore, when they just want ‘pain relief’ or 5% guaranteed from gilts looks attractive compared to fluctuating equities that may fall at times and not even pay a yield, you know there’s a lot not participating long in this market. So why do I feel bullish (apart from the fact that I am always optimistic and often get called a perma-bull) ?

Subscribe for free here:

Well the return in September for a time to remember seems to have started playing out at the end of this week at least after a decent week last week. Indexes here are still sideways for the 250 and Small Cap indexes but that is greatly outperforming Aim which while possibly making a rounded bottom here has been mullared and isn’t out of the downtrend. So many Aim co’s putting out poor to mediocre updates is as bad as I’ve seen it aside from the financial crash although obviously there are decent number which are out-performing. Aim has lost a lot of credibility imo, therefore investors are requiring a decent discount to get involved compared to previous. Invariably Aim is the haunt of the small private punter in the hope of quick moves but a two year bear market has left punters thin on the ground and far more risk averse. I’ve actively avoided most Aim shares of late, I hold just a tiny percentage and always in small proportionate size holdings.

I highlighted a line on the chart on the S&P last week, the S&P seems to be bouncing off of it.

I wouldn’t be so arrogant to say I know this is another short term bottom but I think it’s a very good likelihood imo. What you need to remember is the S&P was just 5% off the all time high. It would be rare to keep sailing up and breaking out without a decent retrace in my opinion. So my best guess from here is the S&P rallies, breaks the 4600 in a month or two, another small retrace as it gets to the old all time high then through and away, probably over the course of the next 6 months imo. I wouldn’t be surprised to see the S&P re test that 4240 level again before tho. That’s my best guess. Meanwhile, the best I can say for Aim is that the decline seems to be slowing.

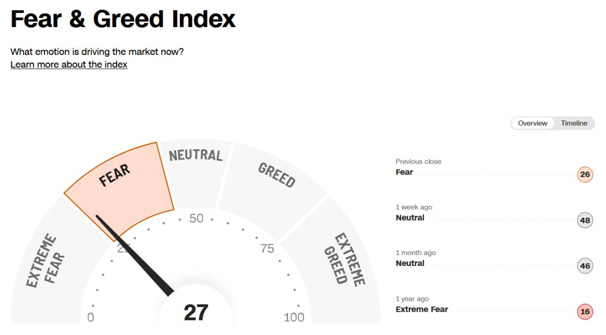

Fear Greed hit ‘Extreme Fear” this week and ticled back up to ‘Greed’. I like being a buyer in the extreme fear sentiment. Doesn’t mean this is the bottom but it is likely nearer the bottom than buying on Extreme Greed.

The VIX failed to break 20 and retraced, another good buy indicator as it never broke the previous major highs around the 20 level.

CARD, Card Factory

Well I, like nearly everyone I know who paid attention, was surprised at the CARD price reaction to the results. After spending a few days looking at the results with a fine tooth comb, to the best of my ability I have come up with what I think the craziness was about, and it looks nonsense to me if I am right. Too many traders, too jumpy, ill-informed and over-invested would be my guess. I’ve decided to go over this a bit more this weekend as I know so many that read this blog are interested.

Firstly I caught a headline from the Investors Chronicle

“Card Factory faces challenging Christmas as online sales fall”

Do the people who write this stuff know what they are talking about or read anything more than the headlines? The financial press see sudden share moves and feel it’s their responsibility to ‘explain’ the reason for it. Sadly, in many cases they don’t know immediately so they make a stab at it but are often very wrong.

What the co actually said was ‘Whilst we remain mindful of the challenging economic backdrop and the impact of the cost-of-living crisis on discretionary spend, we continue to be encouraged by the resilience of the celebration occasions market and the growth opportunity it presents.’

The company never said their own trading was challenging, they just commented on the market backdrop, which everybody knows! It would have been remiss not to mention it. It basically said “the economy is tough but we are doing great thanks” Card Factory’s trading seems far from challenging – look at the like for like sales over the last three reports.

Like for like sales - H1 - Store revenue saw strong growth at +10.5% LFL –

H1 2023 +6.1% LFL

FY 2023 +7.6% LFL

H1 2024 + 10.5% LFL

That is constant improvement and the CEO said that they are trading inline and expect a good year. Look back at past trading statements, Darcy doesn’t do hype, he is very much promise low and deliver high.

Now online sales.

“Online LFL sales were down 13% - that’s 13% of 1.5% of the business – Online is just £8m sales, now £5.8m – from total sales of over £500m, so about 0.2% of sales.

Online sales from Card Factory are tiny. A 13% fall of tiny is very tiny. The co said they expect H2 to be similar. What is the infatuation with online? All Card Factory need online for is click and collect. Sales through stores are massive, they have some of the best retail margins going, they generate massive cash. Why would you want to divert your energy and time to online sale while store sales are rising 10.5% LFL? How much cash would they be expending to chase sales that probably aren’t profitable from a business this small online? At best it would be lower margin sales. How much would that cost deplete your fabulous cash generation and margins? Why wouldn’t you just concentrate on your stores and when that growth starts to slow then concentrate online more? Moonpig are geared to selling cards online and they cannot get near to CARD’s performance by a country mile. What all these online businesses need are click and collect/return points. Look at BOO, ASC – their problem is the returns cost and lack of pick up and return sites. CARD have these. An online sale that has to be posted would be more costly than another instore sale. What CARD want is click and collect - it’s the nost profitable sale and cheaper for the customer like all online sales. If it was me running CARD I’d backstage the online, just keep making oodles of profits and cash from concentrating on the stores and just wait to pick up Moonpig for peanuts down the line because that business model is struggling without printing their own cards and not having click and collect. Think about selling cards online too. If people want them quick then you have to post them out first class, a 125p added cost to say a £2 card. Click and collect eliminates that cost, you can buy online and just pick the card up in your lunch break from one of the near 1050 stores across the country that Card Factory has. Moonpig are good at selling electronic iCards but do they have the appeal?

The next issue is the divi and punters not understanding the company’s financial year from the calendar year in my opinion.

Firstly, CARD’s Financial year runs from Feb 1st to Jan 31st and the financial year date refers to when their results are reported -May usually. So this years results will be posted in May 2024, next year, during their ‘Financial year 2025 which starts Feb 1st. So this current years trading is the 2024 financial year which closes the end of Jan 2024. The company says the earliest it will consider paying a divi is in the Financial Year 2025, That means they can pay a divi for this financial year (2024) and declare it in the results in May by which time we will be in their Financial year 2025. So they can announce a final divi with the results this coming May. Is that clear as mud? If you can’t get your head around it then watch the results presentation at the link at the bottom -watch it anyway imo.

Next thing is the debt. H1 debt is usually larger than full year debt because CARD make a lot of stuff and buy a lot of stuff in H1 then sell lots of stuff in H2 as they have Christmas in that half, that’s usually the half when debt falls as all that cash rolls in.

The company said at the interims this week:

“Strengthened balance sheet with a reduction in net debt (excluding lease liabilities) to £71.9 million (HY23: £96.6 million). £71.9m debt in H1 is down £24.7m on last year.”

Year end debt last year was £57.2m. So with a reduction in H1 debt this year of £24.7m the current annual run rate for year end debt this year should be £32.5m if they don’t reduce debt another penny in H2. Last year they reduced debt massively in H2 so I’ll leave you to estimate where debt will stand at year end but I’ll bet it’s miles lower than last year and way below expected/forecast imo.

Lastly, with EPS up 2.5p on last year in H1 means the trailing 12 months EPS should be 16.2p. Stockopedia say 15.2p but I question their maths there but still, that’s a PE of 7 , huge earnings growth, on their way to being net cash (ex leases) and about to reinstate a divi while generating massive, and I mean massive, cash generation. Another 2p eps growth in H2 doesn’t look a big ask and that would have CARD’s earnings getting up with the all time highs at 18p+ eps imo.

As for why lots of punters sold on the results? Well a combination of reading the above and not fully understanding it? I doubt if more than 10% of holders have read right through the results and watched the co results presentation. Lots of traders expecting a pop on the results to sell into and not seeing it, then cashing in quick? Others expecting Teleios to sell into the results? Others reading online sales fall 13% and not understanding that is negligible. All or a combination of these I suspect. This is why I say do your own research. If you follow others blindly you are a blindfolded sheep. You will likely panic when panic breaks even when it is unnecessary. Sadly I’d say 70% of punters or more do little research, everyone seems to want a tip from the press but then have no clue what to do down the line. Personally I do more and more research the more I like a company. I try to get to learn it inside out. I do punt and trade now and again but usually in much smaller stakes and fully know in those cases I don’t understand the co well, but I never make or lose big money on those trades. Big money is made from buying and holding stocks longer term and knowing more than most other people about a company which requires a bit of work. There are no free lunches on this planet imo.

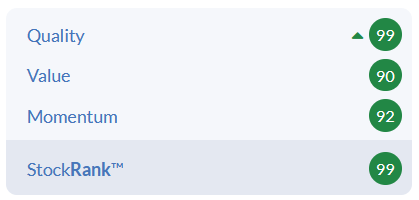

My research says to me in H2 Paperchase are gone from the high street and Clinton Cards are a bigger mess than they were last year. Matalan will have Card Factory concessions in every store before Dec 31st, 220+ stores. The redesigned layout in stores are completed in 700 stores now which produce greater sales compared to the old format of which they only had a few rolled out last year. Shipping costs half the price they were this time last year will help margins further. The company also said “Property costs reduced by 0.8ppts as a percentage of sales, as we begin to see the benefit of an average reduction in the rateable value of our Store portfolio from the start of the new rates year.” This should also benefit H2. They do have higher staff costs than last year so that clips some of the gains but then sales should be 10%+ higher than last year too. Stockopedia now have CARD as number 2 for the whole stock exchange in their Stock Ranking:

Little surprise with these ‘quality metrics - 15.32% operating margins are second in the retail sector only to Next on 18.5%

With all of this I am more excited about CARD than I have ever been, these oportunities come along once in a decade when the market has gone nuts imo. I will continue to hold with delight and let the less informed give back their profits trading in and out. I suspect CARD catch the market out with another whopper trading update before long when traders have gone off blindly looking to trade something else they don’t understand – for them to rush back to CARD again :-)

If you want to learn more have a watch of a great podcast from Iggy this week:

Lastly – why is CARD such an exciting recovery play? Look at the chart below and the 2016 high.

Compare then and now with the performance:

2016 2024

Sales £381m Sales £511m

PBT £82m PBT £60m forecast (conservative)

EPS 19p EPS £16.2p trailing 12 months

Net debt £123m Net debt £32m or less by year end?

Divi 8.5p + a 15p Special Divi ?

Share price £4 Share price £1

All of this just my opinion of course and why I have a large percentage holding. You will obviously do your own research and make your own decision.

Definitely watch the company’s results presentation imo

https://www.cardfactoryinvestors.com/investors/reports-and-presentations/year/2023

Interesting this week.

I noticed MORE (Hostmore) the TGI Friday Group publish results today. There’s a little bowl at the end of the chart I noticed today. They have a new CEO and CFO and a few non exec changes. The interesting thing is the CEO has instructed the house brokers to make regular share purchase and the instruction is irrevocable. I looked at the results today, quite a mess there but slight signs of improvement and quite a confident CEO statement and action. A lot of writing off has been done. One to watch for a recover from here perhaps, especially if the chart makes a bigger bowl imo.

888 – disappointing numbers this week. The chart has an ugly little roll over and I’d stay well away till that changed imo.

MAB - Q4 trading update was positive. They have net debt of £1.7bn but net fixed assets of £4.6b so I think it’s the assets rather than the performance punters like. I’d sack the board personally and get some guys/gals in who at least seemed to be motivated by owning a few shares that they had bought. Vintage Inns are just rubbish while Mitchell & Carter seem to be so much better and it has been like that for ages. Their update may have positive read across for other similar companies tho, like JDW which I hold – JDW results are out next week.

Great update from YU. this week but I’m surprised the divi is just 3p and there’s little dir buying or holding – just the CEO holding a big stake but a great performance over the past year.

This coming week’s updates worth looking out for:

DX. and TEP should have trading updates.

Tues BOO interims, GRG trading statement

Weds TSCO interims, TPT trading update

Friday JDW year end results

We now move into October. This is where we start to get a lot more results rather than trading statements and the point at which shares tend to react. Quite a bit of retail stuff this week to start to get the market juices flowing. Have a good weekend and a fun week ahead.

I can add one thing further to the CARD price fall. In my opinion everyone has overlooked that one of my daughter-in-laws is about to give birth and that my local Card Factory is closed for refurbishment. It's a race against time for the shopfitting team to get the store open so I can dash into town for a 15p new baby card, (+ 80p parking if I can't find a side street). Confidence in companies is everything when it comes to share price movements.

You'd think the Matalan roll-out was worth a few pence on the price in its own right. Take it from a shopkeeper, there are some things bean-stackers don't understand and would rather let someone else do, cards is one of them, too labour intensive. Being embedded, providing an opportunity for a retailer and potentially solving a headache is something I like, (much like MEGP and their photo machines, kiddie rides).

I'll also comment on TEP while I'm here, as you raised the prospect of an update pending, and have discussed them lately here and elsewhere. First off I've heard them advertising on radio as recently as yesterday, (Classic) which I'll take as another sign of the market opening up again. Secondly, comparing energy prices there's no difference (for me) between their unit (kWh) basic rates and for example Scottish Power, but their daily standing charges are lower, and it's this element that gets lower still the more you bundle TEP's other services. However, while not all services qualify for reducing the standing charge rate, adding a couple of services, (I played around with mobile phone and boiler cover) and you might save £50 a year. The problem is that in isolation their mobile phone and boiler cover rates aren't that competitive, (20% and 33% more respectively than I currently pay), the beauty therefore is in locking people in so that if they move away from (say the mobile deal) then their energy costs go up! TEP also provide fibre broadband but the coverage is limited so need to roll that out. There's also home insurance but it seems you have to already be a client to access that.

I learned all this from playing around on their website, any readers here can do that to work out deals with or without also contacting a local partner. It's a good time to do that right now because unit rates go down and standing charge rates go up, on 1st October. I then had a chat with TEP directly, that's not gone too well as I was due a call back on Friday which never arrived. The reason I got in touch with them may be of interest to readers here, there is a 10% energy discount for shareholders so long as you own 1,500 shares, that's beyond me but may be of interest to readers, see here for more info:

https://telecomplus.co.uk/shareholder-discount-plan

Mr Rebel has mentioned the Utility Warehouse cherry on the cake already, the pre-loaded Utility Warehouse debit card that earns a 1% minimum cash back, which in practice means direct reduction monthly from your monthly energy bill. The card costs £2 a month however so you do need to spend £200 on it every month to break even. I'd say for hard pressed families a pre-pay card is also a good budgeting tool. From memory it's 3 or 4% saving at M&S, (another of your holdings CR) and as you mentioned earlier in the week you could spend that amount in one trip to the foodhall.

Thanks for the CARD write up, much appreciated. [For transparency I hold all the above mentioned except MKS and am not currently a Utility Warehouse customer].