Weekend Rebel Review Sat 26th April, 2024

The week the market started to bounce back?

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

Well it has been a very decent week after two strong up-days at the start of the week, with the FTSE100 making a new all time high. Two weak days following which dragged the FTSE100 down below that all time high at the close each day but Friday it finally got up there and stayed up there. Like the FTSE250, the FTSE Small Cap Index broke out, pulled back and has been testing the high again at the end of this week and making a stronger break out on Friday and the bowl called it weeks ago.

Aim has rallied a little but it’s still lagging the 250, and Small Cap Index. Aim has risen roughly 3% this April. Last April it rose 10% approx. When you look back and see some of the big short term moves, then look at the recent meagre short term moves, it really is chalk and cheese, but it will return at some point in my opinion. I think it’s partly down to the number of good businesses getting taken over and leaving the dross behind to some extent. If you shop around there are some good co’s on Aim. The market feels like we are about to start a decent leg up here, there is a lot of results out and trading updates in May. As we had a month or two ago, good news was causing 20%+ rallies everywhere, going forward I expect that to repeat, more whole heartedly too.

The VIX topped out at the 23 I pointed out last week and we are now back in a down trend where we have these ever declining spike up every 6 months or so – so the trend continues imo.

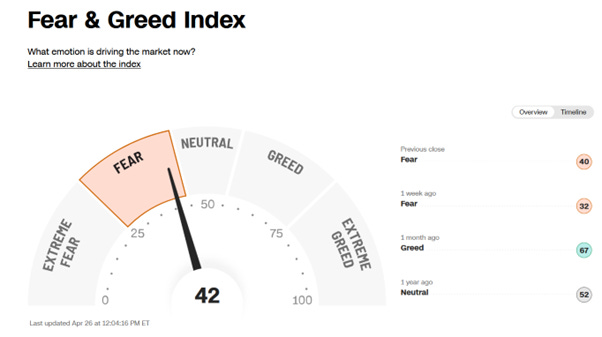

Fear/greed has firmed but still well in Fear, which is good for bullish sentiment.

Inflation refusing to fall as fast as expected spooked the mkt mid week as interest rates priced in the first rate cuts a bit further out. I sometimes wonder what’s in the yanks heads, if you have inflation at just over 3%, interest rates up around 4.7% and unemployment historically low and 2% growth, it isn’t a disaster in my book. And when rates do come down there’s a big Brucie Bonus at some point, of higher growth. Better to have steady 2% growth than lurch from 2% to 5% then see rates and volatility all over the place imo. There’s a positive to higher interest rates and that is the erosion of pension deficits in many cases, something the market seems to have forgotten a bit, more later.

It has been a good month in total. I was up 10.7% for the first 3 months of the year as I said in March. April had a lousy first 3 weeks where I gave back 2.6% roughly but the final week redeemed things with 4.2% up, 2.7% of that on a stonking Friday. So 12.3% up for the first 4 months. I need to make 28% from here till October if I’m going to do that 100% in 12 months from the low of last October now. That will take 5% a month from here, tough one, but it means something like a 12% rise in the FTSE250 between now and mid October for me to get there, perhaps less, which doesn’t sound too bad. CMCX is my largest holding and that has made a huge difference recently, having nearly 2 bagged since my first buy in December.

Monday kicked off with a bid for Tyman, TYMN rising 30% on a 400p cash and share offer for the co. Another FTSE250 co bites the dust on a PE of 10. With bids and de-listings, we will be lucky to have a stock market much longer, small cap choice is getting very limited in the fully listed arena, if you ignore investment co’s on there. EAAS announced a £5.2m contract with Spire Healthcare, SPI. I watch the contracts they win now because a lot of the hardware for their contracts come from LUCE. This has always been more my interest in EAAS than the co itself but a few more wins like that and they should see a positive reaction. Tuesday was busier, with more news but perhaps the stand out of the day was the FTSE100 breaking out to an all time high. It was going to happen at some point but for once the market carried small caps higher too. Up until now they have been dragged their feet, kicking and screaming but on Tuesday we had a whole hearted 1% rally across the board nearly. Sentiment is changing in my opinion, at the moment some investors are buying in on belief the market is going up but the real moves come when FOMO starts to kick in and punters rush in to avoid missing out. With broker upgrades to both MKS and RR. early in the week, they both played their part in dragging the FTSE100 to a new high. Meanwhile, on Tuesday I think I had just one stock down and 90% of my holdings up.

Wednesday opened flattish after a big rally in the US on Tuesday night. The star for me on Wednesday was Warpaint London, W7L, which I hold. They were blow away numbers

Group sales for 2023 grew by 40% to £89.6 million (2022: £64.1 million)

Gross profit margin increased to 39.9% (2022: 36.4%)

Profit before tax was up by 136% to £18.1 million (2022: £7.7 million)

Earnings per share up 123% 18.1p (2022: 8.1p)

It’s a manuscript of fab numbers, positive forward outlook and one of the best growth stories I’ve seen in a long time. While the shares are up 145% in a year, the earnings are up 123% - basically, the shares are valued little more than they were a year ago based on a PE basis. You pay for high growth because that growth erodes the PE so fast, 100% growth halves the PE if the share prices doesn’t rise. In reality, the share price usually rises somewhat inline with the growth or often better as the PE expands thanks to more and more reliability of earnings. Walmart has been gained as a customer in the US and they are now talking to them about supplying them year round. I would read the results because they are so filled with excellent news of progress. Q1 has started well with sales at a record high, up 28% on last year. They have built up a high inventory of stock for a very strong H2 that they are expecting. I can see these doubling in a year again possibly but even 50% would be nice. Definitely watch the webcast provided by ShareSoc this coming week. The shares, even after a strong run, closed up 20p to a record high. These really remind me of the likes of BooHoo and Asos 10 bagger+, years ago, when the market got excited about the interest from young customers – as the old saying goes ‘invest in what the kids are buying’.

Thursday was a rather boring day with the market pretty weak but Friday was far more interesting. MPAC announced winning a £1.2m order to deliver a SiSTEM pilot battery assembly line secured by funding from the Automotive Transformation Fund, partnered with Ilika, Agratas and The UK Battery Industrialisation Centre. That is 3 battery companies which MPAC are working with to develop automated battery production. Agratas hasn’t been mentioned before to my knowledge, they are part of Tata Group. MPAC have stolen a march on battery sector imo. When these co’s start ordering follow on production lines, it could be simply huge for the co. They did underlying eps of 6.5p in H1 and 19.7p in H2 so there is momentum and based on H2 they could be extremely cheap imo. None of the Freyr or the other battery business has any earnings factored into the forecasts. The other exciting point is MPAC has long been regarded as ‘a pension with a business bolted on’. The deficit is eroding in significance as profits get larger but when they don't have the deficit to pay too, then the cash generation soars, investment increases and comes just at the right time for the battery line scale up imo. Adam Holland, CEO, suggests in the results webcast that the pension deficit will be sorted in two years now that interest rates are back to normal levels, hopefully sooner and was chuffed with the job the pension managers had done

I added more MPAC on Friday.

While it hasn’t been confirmed by RNS, CMC Markets, CMCX replaces Wincanton in the FTSE250 on Monday after it was taken over. I expect tracker funds and Mid Cap funds to need to buy CMCX going forward to rebalance their holdings. I doubt many investors had realised this as there has been no RNS or press coverage, it will only be the data-diggers and wide awake club that were expecting this, ahead of the normal re-shuffle imo.

Stocks:

Over the past two weeks I have been buying Premier Foods. PFD. I took an interest in these when Alex Whitehouse took over as CEO (I’ve looked but the CFO isn’t called Mortimer sadly). Whitehouse came with a good CV having been with Reckitt Benckiser plc, for 18 years and also at Whitbread plc, with experience of significant senior international, marketing, sales, strategy, innovation and general management, gained across multiple geographies. He’s seems a decent guy to listen to and has had a baptism of fire joining just before Covid. He has halved the debt to sub £200m through some tough times, even if they benefited from Covid for a while. One of the first things I noticed was there is fairly modest dilution compared to 2006 there were 370m shares, so 130% more than today. To get back to the previous high you are looking at around £9 a share in new money.

Whitehouse has done well in his time there since 2019. At that time, net debt was £470m, at the interim results it was down to £273m from £337m in H1 last year and flat will the year end, but as most of the cash comes in in H2 then the £274m net debt last year may well be some way below £200m this year.

They have also seen the pension scheme perform much better than expected:

“Premier Foods has announced that it reached an agreement with the RHM Pension Scheme Trustee to suspend deficit contribution payments from 1 April 2024.

The suspension of future funds will take place earlier than expected due to the “strong performance of the pension scheme”, Premier Foods stated.

As a result of the suspension, the group said it will benefit from £33m increased free cashflow for the financial year ending 29 March 2025.

The group anticipates no further contributions to be payable after this date, subject to the results of the next triennial valuation.

The last actuarial triennial valuation of the scheme, as at 31 March 2022, showed a surplus in the RHM section of £665m and a deficit of the Premier Foods section of £368m.

Administration costs related with running the scheme of circa £5m per annum and the dividend match mechanism are both currently unchanged, it added.

Premier Foods chief financial officer, Duncan Leggett, said that “significant” progress in the “funding position of the pension scheme” enabled it “to take another important step to expected full resolution of the scheme by the end of 2026.”

With more cash to play with as far as acquisitions go, they could put this to good use. They have recently made two small acquisitions:

FUEL10K, which takes them into the breakfast arena where they currently don’t have brands and The Spice Taylor, both of which are performing strongly.

Add to this that they have some new exciting product that they are keeping under their hat and they are upgrading some of their production lines for greater speed and capacity then there looks a lot going for PFD here imo. In the interim results presentation Whitehouse suggests that with debt down and the pension sorted, they can now look at larger acquisitions.

In March last year they upgraded their forecasts “Q4 to be at least 10% ahead of the prior year.”

In July they said trading would be “at the top end”

In January they said “Well on track to deliver on previously upgraded expectations for full year”

Since then Colin Day, Group Chair, purchased 50,000 @ 153.8p and Phillipa Rose bought 13k @ 151.8p

You can see from the current forecasts they look cheap imo:

Earnings momentum seems to be picking up, they have less debt and more cash going fwd and I think they are nearing an inflection point where the pace of performance will step up a gear.

Jeffries raised their target from 150p to 200p last week.

With 13p eps forecast and a fwd PE of 11, I think there’s scope for more upgrades here.

Obviously you make your own decision after doing you research, this is just my diary and not a tip, but I would say if there’s one area I’m pretty up on, and can hold my own against most people, it’s cake. I’ve been buying from 147p-151p approx..

That’s a huge bowl on the chart imo, if a very protracted bottom, but little dilution compared to the fall. The sort of recovery chart that you dream of getting into and it coming good. And in this case the business is already thriving unlike a normal ‘recovery’ in the real sense of the word.

My second buy this week was Funding Circle, FCH.

Funding Circle provide funding to small businesses and SMEs, typically £100-£250k. FCH floated at 440p a shares in an IPO in 2018. A month ago they announced results which said they were disposing of the US arm of the business and have several interested parties. They also have £170m of unrestricted cash on the balance sheet after raising £300m in the IPO. I had questioned as to whether this was fully unrestricted net cash for the company to do what it liked with and to confirm it I did contact Tony Nicol Group Finance Director and got the reply “Yes that's correct - the £169.6m unrestricted cash is net cash“ The market cap was more like £100m on the day of the results in March, now it’s nearly £200m after the shares have doubled, so basically the business is being valued at just over the unrestricted net cash on the balance sheet. The shares got away without me noticing as I was too busy elsewhere on the initial bounce and I waited too long for a pull back, but I bought in after they had pulled back still, and started nibbling in from 46p just over a week ago and I have been buying up to the middle of this week. What is interesting is they have a new CEO of 18 months ago who has moved up through the ranks, Lisa Jacobs. She has been running the UK side and it is profitable, it’s the US where the losses have been. The UK made £6.5m pbt in 2023. Over the next few years they expect to grow income at 15-20% CAGR and pbt margins to 15%. The US side of the business lost around £20m excluding a $7m write down on a property in the US. They had a choice here to throw a lot more cash at the loans business in the US or to concentrate on the UK. I’ll let you do the maths but if they grow income at 15-20% and have a PBT margins of 15%, then I think you’re looking at PE’s for 18 months time of around 7ish perhaps, less with the share buy backs done imo.

All in all, with the UK making £6.5m pbt and that US business being sold and saving the circa £20m pbt loss next year (well half of it in H2 next year, it will still be part of FCH in H1 and loss making), then going forward it could be a very profitable business with cash as high as the market cap. They are doing £25m in share buy backs and it would be nice if most of this is paid for by the sale of the US business which they say they have had several expressions of interest from acquirers. FCH don’t use their cash to provide the loans, they are provided by institutional investors. FCH act as the intermediaries. Their loans are issued using their own proprietary software to gauge credit worthiness rather than use credit agencies. This has proved far more reliable and they can give a business a loan agreement in principle in 10 mins, all online.

I think news on the US sale is likely to come around the end of H1 in June so they have a clean H2 or as clean as can be, as a guess. The chart looks a screamer of a recovery play seeing they have all that cash in my opnion.

Aside from supplying loans, FCH have introduced Flexipay, a sort of corporate credit card, FlexiPay transactions almost quadrupled to £234m in 2023 compared to £59m in 2022. This looks like it could be big going forward imo. All in all it looks a cheap stock with potential high growth, soon to be totally UK focused and run by the CEO who has made the UK profitable. They also had a new CFO a year or so ago so some decent board changing.

They get great reviews on Trustpilot:

https://uk.trustpilot.com/review/fundingcircle.com

Well worth listening to the results webcast imo

https://corporate.fundingcircle.com/investors/results-reports-presentations/

If you get a blank screen, just hit the back button.

Obviously this isn’t a tip, it’s just my diary for amusement. These are Aim, illiquid and volatile so do your own research. Putting it at it’s basic, you buy the shares here and get your investment back in cash and the US business which should be sold. The UK business that should be profitable, and very profitable going forward, you get for free – to my way of looking at it.

So that’s been the week for me. The S&P is screaming away as I type, the UK market is going to follow them more and more imo, as investors realise how oversold the UK is and especially the small cap sector – the FOMO Bull is beginning to snort away at the gate 😊

Remember, I’m just a bullish investor, I own the stocks I’m talking about so I’m bound to be biased and not as objective as possible so do your own research before buying anything.

Have a good weekend

Rebel

Thank you Dan

Great stuff as ever. I always look forward to reading your weekly round ups.