Weekend Rebel Review Nov 8th, 2024

Trump excites the US Bulls, but what for the UK ?

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

November is here at last, we seem to have got through the dreaded October if not totally unscathed, at least better than it could have been. The budget was bigged up beforehand and as it turned out, for CGT it was a lot less bad than it may have been. Reeves has got her eyes on Inheritance tax though and I’m sure her grubby hands would have been dabbling into our pension pots were it not such a complicated issue. SIPPs are already held in trust so that creates complications in bringing pensions into IHT but I’m sure Labour have the power of their financial brains 😊 working on it going forward and they’ll raid them in the next year or two as soon as they have worked out how it can be done cleanly. CGT selling should have dried up but quite a few will be thinking it’s time to have their 25% cash lump sum still, before she reduces the amount that will be tax-free. Trying to make 25% is going to take a while to do under this government so many will not risk leaving it there, especially if they had retirement plans for it. That will be a constant small drain on socks going forward for a while and won’t help the market, especially Aim imo.

They have hit farmers for IHT, they are raising the tuition fees added VAT to Private Schools and I’m sure there are more delights on the way – all these things suck money out of the consumer and put it in the hands of the government who spend it for us. That won’t get invested in the consumer sector so that’s greater pressure on retailers and service industries. So for me, retail isn’t a sector to be invested in at the moment unless the co has strong self help ability and changes like M&S. Here’s a couple of retail charts from retail greats first is Frasers:

Look at the chart all the way up, spikes, up and down. Then you get to the far right and the chart changes, just rolls over, the opposite to a bowl. That looks worrisome to me.

Here’s another – Greggs

Good growth, good track record, but a PE of 20 and they are going to see wages and NI rise, plus the cost of energy due to this government’s energy policy. Can a retailer maintain a PE of 20 with those mountains to climb? And a weaker consumer? That chart looks like a roll over too imo.

I shorted FRAS and GRG in my November Stockchallenge on Monday.

https://www.stockchallenge.co.uk/

M&S looks about the only retailer that may have upward surprise in them but they are on a high and will need to find £200m in NI and wage rises going forward. And remember, it doesn’t matter if most of the staff earn above the minimum wage, if the minimum age rises, some will fall below it and need a pay rise. Differentials need to be maintained, you can’t pay a new member of staff with no skill or experience the same as those who have worked there some time and have the know-how, they are worth more, so their wage needs to rise too. Aside from M&S and perhaps Next, it’s hard to find a positive consumer chart. JD Wetherspoon, JDW said this week that the budget changes will cost them £60m. That would wipe out 75% of this years pre tax profit forecasts. These are not one offs – they have to make this up and more each year. Many more high staff businesses are going to feel some pain imo.

I am heavy cash still, 65% approx, but I’m prepared to get long fast in the UK starts to look anything better than negative. In Sep2021 to Feb 2022 I saw the FTSE250 rolling over and ignored it to my cost. Here is the FTSE250 – it shows the FTSE250 roll over then and what I see now:

There is a chance that nothing more becomes of that roll over I have marked recently as there are a number of support levels quite close but what would be the catalyst for the chart to turn up? Well the US election win for Trump may mean tariffs and price wars with the US but it also means a better business outlook for the US and if Elon Musk can cut their spending for them, the sight of US borrowing starting to come under control would be a big positive. Under Regan they had strong growth and paid down debt, imagine a repeat of that.

The FTSE250 has big support around 20100

One positive that I would take is the fact shipping container prices have fallen 50% since June and diesel/petrol is down 15% too roughly – that will reduce a lot of business costs going forward and will help offset the NI and minimum wage costs. Need to watch the £ falling v $ though if that continues.

Here's my issue – markets dislike uncertainty. Gilt yields hit 16 year highs this week, higher than when Truss had her melt down. The government is taxing people to an extra £40bn – that is a drain on the consumer. They are going to spend £25bn on the NHS and going to borrow a whole lot more cash and spend it – that will be a stimulus. So where is inflation and growth going, they are two opposite forces and it is hard to calculate. The Bank of England sees a weakening pound and the gilt yields on the 10 year and must be wondering what they should be doing but they are suggesting a lot higher growth over the next two years, inflation hitting 2.7% before it pulls back in the latter years of this government. Now we have Ed Miliband saying that we are going to have black outs, actually saying the public are going to have their energy rationed and we’ll be asked to reduce consumption. That’s a lot of new factoring in to work out where compaines stand.

The momentum is weakening globally as you can see in the FTSE All Word Index. You rarely if ever see this roll over on a chart then see a sharp upturn, there is nearly always a big retrace first but we have Trump in now and the stock markets of the world did ok when he was last in so perhaps this will perk up.

On a really bullish side, for the US at least, the S&P has been breaking out through a very long term resistance, which you rarely see also, but usually indicates a much stronger rise – gulp! Perhaps AI is going to make a huge effect much like the tech boom did?

S&P

The other US indexes are doing similar. The UK has really under-performed compared to Germany’s DAX and France’s CAC so there may be a lot priced in already. In addition to higher minimum wage and NI we also now have the highest electricity prices in the world.

With this in mind, I am looking for co’s that have high overseas business, both staff and factories. These co’s will be avoiding a lot of the wage rises, NI and paying far less for energy – how do you compete in the UK with such high energy prices? And they want to build a huge solar farm at Botley, 3 mile square, the size of 1300 football pitches – did you know in the last 12 days England saw just 20 mins of sun in all that time, not even per day? We will all be subsidising these things by paying more for energy.

So at the moment there are a number of macro factors affecting businesses in some way so it is important to watch where you invest and take these things into account. US charts are hitting long term highs on the trend lines, but they look like they are breaking through them, the UK is seeing added costs but they may be priced in? Either way there will be a lot of positive and negative surprises likely to show up in results going forward imo .

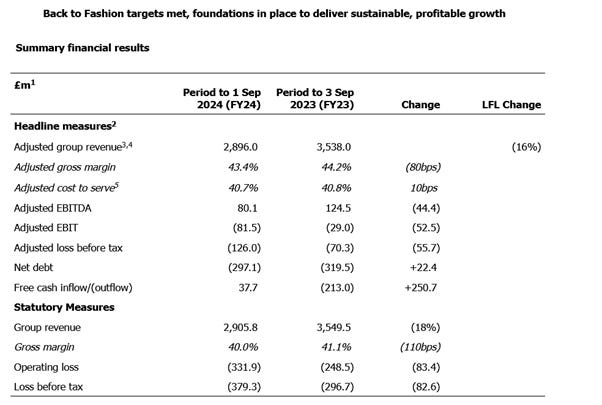

Asos is an online retailer I watch quite closely. Having had board changes and director buying it has been even more in view. The new board have been disposing of tons of out of date stock to get their stock levels down. They claim to have a new business model of sorts,

“Back to Fashion targets met: Stock clearance complete, new commercial model embedded, Test & React scaled above 10% of own brand sales, flexible fulfilment doubled and unit economics transformed with variable contribution per order now +28% on FY22. Foundations of more agile and profitable business now in place.”

It’s going to be another wait and see as the results were pretty dire:

There’s lots of upbeat sounding stuff in the results about inventory levels, newness, margins, EBITDA and the rest of it but these really are not investable until I see tangible improvement in numbers, not just promises. Is an online clothing model still viable or do they remain a place where people buy cloths, wear them then send them back? Rewarding those that don’t return stuff is one way and punishing those that do return a lot is another but the best way is to have accurately describe clothes and clothes that are the size customers order, when they arrive.

The shares tanked to what was nearly a new 20 year low. One to watch and look out for news from but not yet investable imo.

On a similar theme, Sosander. SOS announced they have won a license agreement with Next. Next is extending its partnership to licensing the Sosandar brand to develop a homeware range.

What is this company doing? A bit of focus surely? They have started opening clothes stores to enhance sales as up till recently they were online only. I am not against this but it will drive up costs compared to being pure online. Now they are going to start doing homeware which they have never been involved in, in a licensing deal. Do Next really want homeware designed by a co that has no record of designing homeware or are Next designing it all and just badging it with the Sosandar name? The argument for Sosandar was that the joint CEO’s came from the fashion industry so they knew what clothes more mature women want. But what do they know about homeware? They don’t appear to be cash generative and say they have reduced sales forecasts for this year slightly.

Why don’t they stick to what they know and get that running well first and generating cash before getting involved in homeware? Possibly it costs them next to nothing if Next are just badging it as Sosander but it seems odd that Next are paying for something that they are putting all the work into if that’s the case. The sceptic in me says if they start a homeware side they can say they need more cash and have yet another funding if they go into homeware too.

They need to impress me a lot more before I’m a buyer, sorry. A somewhat strange deal.

M&S, MKS released interim results on Wednesday, in a market that was roaring away from the Trump win.

The results were very good in my opinion:

Not much to complain about in that lot, Stuart Machine and Archie are doing a fab job. Both food and clothing growing. Overseas, a small part of the business saw a 10% decline. Ocado had a £16m loss. M&S now have 500 lines on Ocado.

The company says it is investing in a complete new IT system to make it far more efficient compared to the legacy system.

I’ve noticed the food side of things looking strong in-store with them rebranding and introducing improved higher price products. Store renewal hasn’t gone as fast as the co wanted but they have recently acquired 10 new prime sites so that will help boost store renewal and sales growth going forward. Most wage rise costs have been offset by cost savings.

H1 earnings were up 20%, that puts them well on course to beat the constantly rising consensus forecasts.

I obviously sold a bit too soon recently but better too soon than too late. I don’t mind banking profits before news to play safe and don’t mind buying back a bit higher after the results for that safety. One baggers in a year are going to be harder to find than in the past two years so I will have to hold shares that look solid earners to a greater extent here. I bought some back around the intraday lows on Weds and first thing Thurs at just under £4, it cost me 20 points trading out and back in. The market will likely see a little pull back on profit taking as often seen on results but I think there’s a lot more in them and will keep buying through the pull back. I thought Machine sounded more positive in the results webcast than I have ever heard him.

Brokers clearly liked the results:

Really positive is that despite the rise in minimum wage and NI in the budget, M&S broker consensus is rising, a 3-5% rise right after the results so that’s very positive imo:

It is well worth watching the company presentation in my opinion, when you watch them regularly you can see and hear the body language each time:

https://engine-3.sharepad.co.uk/SSWeb/app.do;jsessionid=0B8F1FFCAC33CB3466E11F481F4D822F

Stuart Machin CEO

Rolls Royce put out a very good trading update on Thursday.

“Trading update to 31 October 2024

Our current trading is in line with our expectations and the Full Year 2024 guidance provided on 1 August 2024 of underlying operating profit between £2.1bn and £2.3bn and free cash flow between £2.1bn and £2.2bn remains unchanged. We continue to strengthen our balance sheet. This has been recognised by the ratings agencies, all of which now hold us at an investment grade rating, and all with a positive outlook.”

One of the stand out messages was this imo:

“In Civil Aerospace, demand remains strong across business aviation and widebody. Large engine flying hours grew by 18% year-on-year to 102% of 2019 levels for the 10 months to 31 October 2024. Our expectations for the full year 2024 of large engine flying hours at 100-110% of 2019 levels, 500-550 OE deliveries and 1,300-1,400 shop visits remain unchanged”

All in all a good read and inline with expectations especially that free cashflow which stood around £500m at the last annual results. The investment grades from the rating agencies are likely to rise which should lower the interest they pay. Nuclear is something that is going have to be embraced here if we are not going to have gas as a back up to solar and wind here and abroad and when this picks up there’s even more to drive RR. I’ve had some RR. back on the dip too.

Travel

Reading the statement from RR. re flying hours reinforced some thinking of mine. I did think as soon as the Reeves started looking for tax revenue that people with pensions might take their 25% tax-free lump sum early to avoid any tax changes. It seems many have done this. My thought was what would they do with the money? That cruise they had promised themselves was my first thought, perhaps a new retirement home or a holiday home. Carnival, CCL has certainly seen a strong performance recently and the chart has curved up to break out through multi-year highs:

CCL

One I hadn’t thought about was airlines, I can’t imagine there’s enough people taking lump sums to make much difference there but airline charts are strong too I see, making nice bowls and multi-year highs:

I don’t know the reason for this strength, it may be the fact that the price of oil has declined 15% or so over the last 6 months and improves their hedging costs. The middle east hasn’t got out of hand as many may have feared earlier in the year so that may be having a bearing too. If RR. civil airline travel numbers reflect the entire industry then perhaps things are busier than expected in air travel. I posted the charts on Twitter this week and I bought JET2, IAG and CCL mid week, the charts were too good to ignore. They may just be a trade, I haven’t done the research I should, but I will likely hold for now. I’ve just bought the charts so do your own research and if anyone has another reason why these three are so strong I’d be interested to know. As luck would have it, IAG had their Q3 trading update today, Friday and it was rather good – I hadn’t realised the t/s was due.

The full RNS can be read elsewhere but it’s a solid update which beat broker expectations, leading to an opening rise of 6%.

Jet 2 interims are on Nov 21st so will be worth watching out for with a chart like that imo.

Lastly Burberry. BRBY

I highlighted the bowl on the chart recently:

The shares have gained around 20% since then and the chart is strengthening. I don’t know what is driving it but this is a rare chart strength compared to most. There has long been talk that BRBY could not realistically remain independent and the Likes of LVMH or similar would come calling at some point. I don’t know if anything like that is driving it but well worth keeping on the watchlist imo. Results are on Thursday.

That’s what has been creating interest for me this week. With the budget and the US election done and dusted, investors can invest with greater confidence now so I suspect there may be some interesting moves on results and updates going forward to look out for. Investors/traders have been very focused on the maro, as we go through the coming months, individual stock performances will come into the cross hairs and create big surprises imo. All in all I wouldn’t say I feel bearish, I think I’d say, to paraphrase Stuart Machine at M&S, ‘positively cautious’ :-)

One more buy for me this week - The Gym Group, GYM - I’ll try to do a write up next week. Big volume today and a director buy yesterday - it’s about the cashflow imo

Have a good Remembrance Weekend.

Rebel

yep, with the £ falling and the US markets strong, I think a lot of UK money is in the US. Will be interesting when some results here emerge.

Well she's had all the other balls I've got so why not? :-)