Weekend Rebel Review, Nov 11th, 2023

Let's get ready to Rummmbbbllleee!

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required. Well the rain has killed any hope of doing anything meaningful outside today so time for a weekend review again this week. There’s a fabulous feeling about the market currently imo, although many may not feel it. When investors/traders sell off just because they cannot take anymore, when they just want ‘pain relief’ or 5% guaranteed from gilts looks attractive compared to fluctuating equities that may fall at times and not even pay a yield, you know there’s a lot not participating long in this market. So why do I feel bullish (apart from the fact that I am always optimistic and often get called a perma-bull) ?

Subscribe for free here:

Good day and thinking of all those that gave their lives or were injured in keeping us safe over the past 100 years – we owe every one of them or freedom, I hope this never gets forgotten or over shadowed by woke people that have never had to fight for their country in their life.

Warning: the following blog contains content from a perma-bull in a very bullish mood!

I notice my Substack subscription numbers hit 1500 yesterday, thank you to all who follow this blog and find it useful.

It has been another great week taking my rise to 11%+ in two weeks, and while the US never broke out that wasn’t a surprise. The S&P has had a two week solid rally and it would be rare for it to have the momentum that it has had to carry on right through a major resistance. So indexes tend to have a pull back then take a run up and go through then. Thurs was the pull back and Friday was the start of the rally. Resistance lines got broken late on Friday and that will be very positive for the coming week in my opinion.

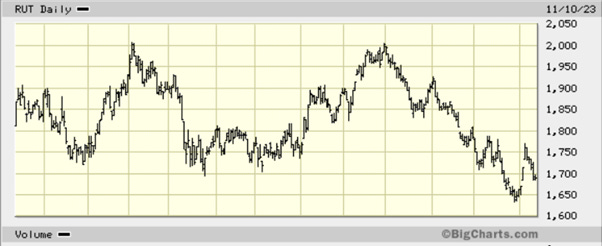

The VIX has fallen to 14 and the Russell 2000 has made what looks like a nice bowly bottom

The Russell 2000

Fear Greed has headed on up to 39 as investors get more confident.

Over the past couple months the FTSE 250 has struggled to break through this resistance line below. I expect this will be the week where it breaks out in style as the S&P breaks out. There is a great bowl here on the 250 chart:

With most of the macro out of the way there’s not much there to worry me. This doesn’t mean some event cannot happen but the indexes look and feels like the markets want to break out seriously here, and are going to rise quite firmly imo, possibly 1-2% on Monday and likely more through the week would be my anticipation.

What was the best performing UK index on Friday? Aim All Share. It was off 0.45% while the 250 was off over 1% - this is a rough pattern seen over the last fortnight quite often.

So let’s move onto the real stuff that makes money – the shares themselves. Many shares have been forming rounded bottoms or bowls, this is something you see when markets bottom. There has also been far more director buying in recent week.

Friday saw a good trading update from W7L which I’ve held for about a month. Now doing in the US what they did in the UK it has great momentum. There’s a good interview with the CEO on Youtube, via Sharesoc - very worth watching, if I had seen that earlier I would have bought far sooner. The founder CEO comes across as a very straight sort of guy with a strategy and he still has a large investment in the business.

I mentioned last week that WRKS had caught my eye just before their trading update and were extremely cheap and I had bought a small position ahead of the update. Well they were cheap for a reason – trading really is poor and they are really talking while on the back foot. My local WRKS is in a garden centre and it has been very quiet. In the past this has been a very good gauge of how the business was trading but for some reason I chose to ignore that, blinded a bit by Kelso buying a big stake. Well, there’s a lesson for you, well more for me really, when you have done research and it says things aren’t great, don’t ignore it. I took the hit and sold on the update, fortunately an easy position to get out of. I will never trade this stock again, it has bit me too many times!

Watches of Switzerland Group - WSOG – this has been a big buy of mine this week, it’s now 7%+ of my portfolio. I started buying last Friday and Monday at 531p average as I noticed a bowl on the chart days before the trading update. I was planning for it to be a trade but having read the results and read the ‘Long Range Plan’ they posted along side the results, and listened to the dial-in in the morning and watched the webinar in the afternoon it was clear to me this was a fabulous buying point in my opinion. These floated in 2019 at 270p. They did 8p eps in 2019, 28p in 2020 as the shares rose to 380p. on the trading update this week they were trading at below 520p with eps expectation of 52p. The compound annual growth rate of this co is 125% since floatation, they are doing double the earnings pre-covid.

I’m quite surprised (well no I’m not actually) at the number of investors/punters/traders, call them what you will, that were saying ‘why are the shares up, trading looks flat to me?’. The market doesn’t look at what you have done, it looks at what you are going to do!

WOSG achieved these earnings despite several key Goldsmiths and Mappin & Webb showrooms being closed for upgrades and trading from pop-up locations during the quarter.

In addition, they have acquired 19 Ernest Jones stores recently and they will be up and running as part of WOSG from the new financial year. They have also recently started ‘Certified Pre-Owned’ where Rolex take used watches in, service them, certify them then return them back to the stores for resale. This is going down really well and sales are up. Pre-owned sales are up 80% on last year but Certified Pre-Owned has only kicked in in the last two months and it is proving very popular. All of this means scope for a much better, stronger H2 with sales growing whereas in H2 last year it was declining. Sales in the US are growing strongly at 11% but the really interesting thing is sales per capita are 40% higher in the UK than the US and there seems no reason why this should be other than the fact the US has been underserved. The business is also moving into jewellery more too, so that’s even more sales opportunities. Basically this looks like the inflection point that recovery play hunters look to buy on, tho this isn’t really a recovery – this is just a stock that fell out of sentiment when rates started to rise and earnings momentum slowed. The next move in rates looks like being down now and when that happens one of the best places to be is high end consumer cyclicals imo.

WOSG chart - note the recent little bowl on the chart - there’s nothing like that anywhere in their previos chart timeline

To add to my confidence, the directors including the CFO who were selling right near the top have now been buying heavy in recent months. I bought last Friday because the chart was showing a great short term bowl. Add that to the positive update and the director buying and there’s a lot there that I like and as sentiment improves, I expect these to rerate. The Co published a new Long Range Growth Plan yesterday which may have whetted investor appetites, forecasting a doubling of sales by year 2028. Remember this is Financial year 2024 that we are in so doubling sales in 3.5 years. It’s easy to dismiss this and say yeah, but they are just ambitions, but they presented a Long Range Plan in 2021 and they are currently £200m sales ahead of that plan, so their words are more than matched by deeds imo. They have doubled sales since 2019 while earnings have risen 10 fold so if they can double sales in the next 3.5 years earnings could get to some heady new highs imo. The major point I am focussed on is that Certified Pre-Owned has kicked off strongly, sales are now increasing and demand still outstrips supply. With sales on the up there is likely to be PE expansion too and on a PE of less than 10 for the coming year the downside seems extremely limited – these were trading on a PE of 30+ when the market was excited. If they increase earnings at a fraction of what they have achieved from doubling sales in the past, then over the next 3 years these could get to new highs and possibly a lot more – it would be fun watching it travel there as a shareholder imo. Most importantly there has been no dilution since float. The co will publish its interim results in 4 weeks’ time on Dec 9th.

Watching the webcast from July for the full year is something to be recommended as the start of anyone’s research, and make sure you do your research, I am never right all the time by a long shot and assume that I’m wrong until you a certain you know better.

On a better note, my second largest holding, MKS, which I highlighted last weekend, came out with a stonking H1 set of results. PBT and EPS together with sales came in miles ahead at 12p eps. I watched the results presentation on results day and it is extremely revealing. They said earnings will be weighted to H1 this year. This has to be nonsense imo and just expectations management – they would need to do less earnings in H2 this year than they managed last year despite having grown strongly. I feel it’s nonsense. Watching the presentation, Chairman Archie Norman does his best to suggest H1 was lucky as competitors were struggling, the weather was good……….blah blah. Then Stuart Machin does his bit and he can hardly contain himself, listing reams of places where they can and will improve. I have bought more and a director also bought another 50k on Thursday for £124k. Shore Cap has raised guidance by £100m pbt “"The group’s house broker Shore Capital said the half-year profits were 39% ahead of its prediction and that it was upgrading its expectations for full-year profits by 12% to £646m." Consensus prior to this upgrade on Sharepad is £546m pbt and 19.2p eps - that has to be 22p eps with scope to beat by some way imo “To misquote the great and recently retired Michael Caine, AKA Charlie Croker of the iconic British movie The Italian Job, M&S ‘blew the bloody doors off’ in [the half-year],” the analyst Clive Black said in a note. I could add “Not a lot of people know that”, but it will dawn on investors that M&S forecasts are very conservative in the coming weeks and I expect broker upgrades.

I’m convinced these will be a lot higher after the Christmas trading update in January and with cashflow rising, debt falling and a divi reinstated then the credit rating will soon be back up to investment grade and that will trigger big institutional buying and PE expansion imo.

In my opinion, MKS will do 25p eps this year without breaking a sweat If they do, that will mean 30p eps very likely next year. That would be 50% eps growth this year. I expect on that growth they will command a fwd PE of 15. That would produce a share price of 450p a share, nearly double where it is today and that doesn’t require too much of a stretch of the imagination.

As a ‘Bull Case Scenario” how about they do achieve the normal 40/60 earnings split this year? That would be 30p eps this year and likely mean 35p eps or more next year. On that momentum a 15 PE would produce a share price of 525p a share, but that sort of growth may produce an even higher PE. Remember they will be doing the store refurbs and roll out for a further 2 years which is boosting earnings – this has been stepped up to two years, it was going to be 3 years but the returns are so good Machin has upped the pace. So there’s loads of “self-help” to get the business growing faster.

In 2016, on just £10bn sales, they were doing 35p eps and paying an 18p divi and the shares were trading at nearly £6. There’s 20% more shares now so the equivalent share price was really about 490p then. So they were trading on a PE of 17 back then when growth had pretty much stalled. As these become investment grade again the funds will chase the stock up and expand the PE again imo.

Speaking about Ocado, Machin said they would get a return out of this over 2-3 years. I suspect they buy the other half of Ocado retail in a couple of years when all the refit spend is done – this could be the next exciting leg of growth.

Remember this is all just my opinion and I’m no analyst, just a private investor with impostor syndrome. Do your own research, it is like packing your ow parachute!

Coming up over the following week – some of these dates are guesses based on last year:

13th BPT trading update approx

14th HILS trading update

15th EYE Finals

15th DX. Finals

15th CARD trading update approx

16th SGE trading update

17th KIE trading update confirmed

17th MTO interims

20th CER finals

Have a great week next week, I suspect it could be a bit good, especially if inflation numbers on Weds are better than expected.

Rebel

I appreciate your 11th November sentiment. Perspective!

I like WOSG but isn't there an elephant hiding behind the curtains? The SP dropped 30% in a day in August when mgmt were cornered into a defensive statement concerning Rolex's surprise move into direct retail, Rolex being materially essential to WOSG's trade and meaning it could be perceived as competing against it's own supplier. Personally I think in hindsight that it's bear market jitters but a change in the landscape not yet fully resolved. In my view Rolex won't want to give up WOSG and was only defending an existing sales channel in making the buyout. Better if WOSG had bought Bucherer though! Condensed reporting from Thomson Reuters, 25th August:

"WOSG.L shares fell almost 30% on Friday, on course for the

biggest one-day drop on record, as Rolex's purchase of [luxury watch] retailer

Bucherer raised questions about Watches' prospects.

"Inevitably the market is debating today the extent to which

the news signals a growing risk of a weakening future relevance

of WOSG to a key supplier for the group," Jefferies analysts

said in a note.

Bucherer owns more than 100 sales outlets worldwide, of

which 53 distribute the Rolex brand."

Anyway, I held at the time and bailed for an unpleasant clip around the ear holes. The recent bowl is forming after that day of summer madness and in my view you've bought in at a price point that is back to pre-Covid levels so hard to imagine it will go lower again than it's recent bottom. Maybe I'll revisit and maybe the update says something about Bucherer, I've yet to catch up.

CARD price seems be be recovering this last week from its sub £ lows and ahead of the update.

Thanks for being the guinea pig for WORKS, very decent of you.