Weekend Rebel Review – May the 4th be with you. 2024.

CARD, IGR, LUCE, FCH, W7L,

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

The market is feeling evermore positive imo. I’ve been saying for a while that our market has to bounce soon just on valuation and the fact that foreign co’s will be swooping in and taking UK co’s out on the cheap. We have seen no end of that recently, WIN. SONG,……..are just two and two more bid approaches on Tuesday for AFM and TRIN – it’s like a turkey shoot for companies to pick other co’s off on the cheap. I also saw this someone highlighted for me:

Stuff like this breeds bullishness and bullishness breeds FOMO – some positive news to move the market and watch the punters pile in before they miss out, I’m sure everyone remembers the Covid FOMO bounce. This won’t be as steep but it will grow in momentum as punters get braver and then get greedy. That’s what I believe, a bit of negative news might delay some of that now and again, creating small pull backs but it will happen imo.

The expectation of interest rate cuts in the US got a set-back again this week after US data suggested a cut is further out. I’m surprised this rattles investors a bit because the US seems to be doing pretty well with rates where they are. If we went back a few years, the ‘experts’ were saying that as soon as we raised rates again we would have another financial crisis due to all the quantitative easing out there. But au contrair Rodney, au contrair. If you’d offered these central banks rates back up to normal 5% sort of levels without trashing the global financial system they’d have bit your arm off. There’s a lot of smart cookies out there but even at the top there are stacks of charlatans that are really winging it – some would point to the Bank of England, I couldn’t possibly comment 😊

Here in the UK so much bad news is priced in, down to a Labour victory in the coming election. It’s easy to fear what Labour would do if they get in but they are going to be governed by exchange rate. They have seen Truss the movie, they know how nasty that ended, they are not going to want to be the sequel soon after coming into office despite being financially inexperienced and naïve imo.

This means that most stuff that’s negative is likely priced in, in my opinion. Small Caps are back in fashion, The FTSE Small Cap, Fledgling and Aim Indexes are all breaking out. Chartsd are below.

Investing is pretty simple – find a system that works for you and hone it imo. I have done well over the years but I’m still honing things. I really try to keep my long term holdings down to a dozen but it’s a real task. I get into trades when I see obvious quick turn profits but kill these pretty quick and boost the long term holdings with any gains, but it really is a distraction and not all trades go well – my dozen or so long termers will be my biggest holdings. Time spent doing short term trades is time lost studying stocks. I gave my old chatroom up because that was such a distraction from my stole focus. Since then I’ve outperformed the market far more, discovered RR. and MKS early, things I wouldn’t have looked that hard at in the past. Hone and Focus. Some investors, perhaps older ones who want a regular income, may want to buy high yield stocks and just hold. I’ve always been a greedy investor. I’m mercenary. If I have a stock that looks like it could grow 100% in a year, I wouldn’t be bothered selling it if I thought I could find a potential 200% in a year, all else being equal. The market has changed recently. I’ve learned over time you need to constantly hone your investing method. You also need to max your holdings when market pace is strongest to get the optimum gains. Look at what you have been doing, see what has worked and what hasn’t. Cut down the stuff that fails and up the stuff that works. Basically, this is just how machine learning works – machines are not over thinking it, in fact they are not even thinking, they are just increasing what works and eliminating what fails. If you analyse, study balance sheets, buy deep value and asset rich stocks and just wait for value to out, and that works for you, then do more of it. I have my formula of what works and the more I focus on it, and increase it, and don’t get distracted by trading noise or silly social media nonsense, the better I do. I place a lot of focus on charts, on researching the company and the directors and focussing on a common-sense approach. The balance sheet I find dull, boring, difficult and to be honest, with most recovery plays, secondary. Beat up stocks rarely have great balance sheets. If you find a recovery play and a great balance sheet too, it’s a bonus for me. I’m more interested in the guys and gals running the show, their history, their experience, the company’s market, what has the co achieved in the past. Where did the stock get to before? Has there been dilution? Can they get there again? At the end of the day, it isn’t about how you win, it’s about making sure to the best of your ability that you win. Another thing I‘ve learned is to not keep chasing more and more shares. Learning to do nothing is the hardest lesson. I see a lot of small caps with great news these days, but unlike in the past, I often just let them go. Instead of chasing more and more, I prefer to increase the winners that I have, that look cheap, I’ve actually already done all the research on them. If something looks like short term news like a bid or just good news, rather than compellingly good, then I might buy the news and sell very short term, like that day or in a day or two. I much prefer to add to one of my 12 or so long term holdings, unless the news is so good from a co that think it could replace one of my long termers, then I would likely buy in more heavy.

There’s interest in small caps again and some are motoring. On that basis I’ve been trimming MKS and RR. While they are great growth stories, I don’t think they can double as fast as some small caps now. FCH up nearly 200% in a month, CMCX up nearly 200% in 4 months, FDEV up nearly 100% in a month, SYNT up nearly 100% in 6 weeks, these are early bull market moves. When these things move like this you have traders hopping in and out and you have stale bulls selling out on strength. But the real way to make good money is to buy and hold until something glaringly better turns up imo, for me it does anyway. The thing is, in a year’s time, from the start of a bull market, you’ll look back and these moves will likely have grown several 100% further, they will hardly show on the chart.

The upside surprises on results just keep coming, little wonder there are so many bids for UK companies. And the big risers on results are out there still, CARD up 10% on results day and IGR up 30%, both on the same day. After an uneventful but fruitful Monday where the market climbed well, Tuesday was the wake-up day as CARD was out with final results and IGR with a trading update. There was a common theme with these two, not the fact that they are both involved with Christmas greetings, but both companies had been quiet with their trading updates for months.

Thursday had plenty of news but nothing much to set my heart racing, until at the open D.Bank came out with a target price of 250p for FCH, over 230% above the current market price. I haven’t read the note but with roughly 70% net cash compared to the market and cashflow set to increase, and profitability likely to increase strongly (UK loans business made £6.5m pbt) then I can see where they may be coming from. I increased my holding further, they looks totally mispriced but that’s what happens in big bear markets when punters just throw in the towel. £25m share buy back going on and the sale of the loss-making US side all adds excitement to the shares imo. They bought back another 200k on Friday.

D.Bank also came out with a target of 182p for CMCX. I can’t see where they are coming from there. With 17p eps forecast for the coming year and that looking very conservative and with £188m in net cash, nearly 25% of the mkt cap, and eps forecasts rising at pace and with trading updates very positive, that looks mad imo. Perhaps a grudge there as they were pushing IGG as a buy the same day. I continue to hold as my largest holding.

Later at the close, Warpaint London announced the CEO ad MD Samuel Bazini and Eoin Macleod both intend to sell 3m shares each in an accelerated bookbuild. They both hold 19.45m shares each so it’s around 15% of their holding. I’m cool with that. They last sold about 6 years ago and the shares have doubled since. Directors have to sell some shares at some point and they are keeping a lot of shares still. Selling 15% of your holding each time the shares double seems a pretty decent plan if I was a director. Friday revealed the result of the bookbuild, 7m actually sold due to ‘overdemand’ and at a price of 450p a share. That was a 5% discount to the close the previous night which seems very decent to me. You have to take into account the shares have risen 300% in 18 months and it takes a brave person to buy a huge ‘lock in’ stake after that sort of rally imo, so there was bound to be some discount. W7L have a presentation this coming week which I’m looking forward to and I’m cool with the placing. In all these things your nose is more important than your eyes imo. W7L come across as a well run business imo – they aren’t forever giving themselves options and dumping them, they haven’t been selling in little bits, they don’t have placings to raise cash just to cover working capital, they are net cash and pay a divi, rare on aim imo. Some punters spooked at the open and sold but the price only came off 5p, reversing that and ending up 5p at the close. I think that says a lot.

Something I have noticed in my time, good companies see directors sell before good news, not before bad news. Lord Wolfson at Next is a case in point. If you are a director with a big stake and you decide to sell some, you want to do it before good news. This way, in a year or two’s time, when you might want to sell more, investors can look back a see that there was nothing iffy in your previous sale, that way you will find investors content to take large chunks from insiders. Mess around and sell before bad news and you’ll struggle to ever sell shares again. It’s not about the sell, it’s about what proportion you retain too, and this was just 15% or so of some big holdings.

On Thursday LUCE announced they had bought 1,000,075 shares at 159p for the co’s Employee Benefit Trust. The company has their AGM on May 14th, usually accompanied by a Q1 trading update, while they, in reality, will be 2 weeks from H1 end.

Friday finally saw a bit of life in the market and while the UK firmed through the morning off of Thursday night’s rally in the US, at lunchtime the US non-farm pay roll showed job demand weaker than expected. Bad news is good news here and that makes the case for an earlier rate cut more likely. Mean

while in the UK, Labour’s gains in the council elections may have spooked a few but the real data for me was UK Composite and services PMI numbers both 54+, strong growth and better than expected, The S&P and all the UK indexes were up well and breaking out clearly.

FTSE250

FTSE Small Cap

FTSE Aim

All of the small cap indexes are firming sharply, money is returning. Get better inflation data here and the hint of a rate cut and the small caps will fly imo

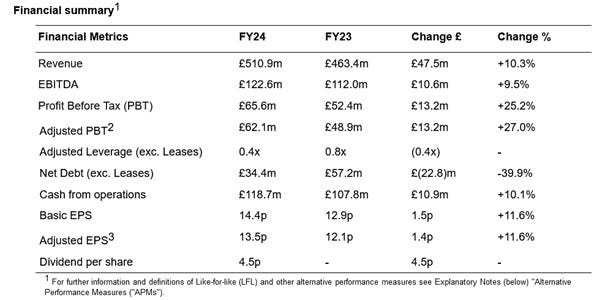

Cardfactory, CARD, which I had held for a couple of years up till late last year, put out final results which were better than expected.

that’s normal for CARD. All in all, investors were pleased and drove the shares 9% higher. At this point I hear share-buddies saying, ‘are you buying back in Cockers? Well had this been a year ago when winners were hard to find I would have done, but the market has moved on, bulls are in the ascendancy. With Teleios still holding 38m and looking like sellers I think I have bigger faster fish to fry but with the yield and cash generation, I’m sure a lot will like it in their portfolio. I think I can find faster better buys now, but Darcy has done a fab job in the face of higher interest rates and a big rise for the Living Wage which must have cost them. Perhaps a few institutional investors may take out Telieos after results like this and clear the overhang that seems to be there. I like CARD as a company, well run and by a very good CEO imo. Strangely, on Wednesday I noticed CARD short interest went from 0% to 0.5%. Who shorts these things and why? I can see no reason in the public domain that would make me think CARD are a good short.

IG Design, IGR published their trading update on Tuesday too. I and many others have been watching these for some time and the real bugbear again has been a lack of communication. Punters, traders etc, get the jitters when you don’t get the trading update this year, at a corresponding time to last years’ statement. One of the toughest things to do as an investor or trader is to prevent your mind conjuring up false demons. Sadly, in tough markets, many investors including myself, can ignore a bargain share if they feel uncertain or uneasy. In the event, while sales were down on last year, margins had improved well as the company targets much higher margins going forward.

“The Group has continued to make good progress on its turnaround journey of improving operational efficiency and simplifying the business. These initiatives have resulted in significant growth in profit and margin for the year. The Group expects to deliver adjusted profit before tax of $25.9m (FY23: $9.2m), which is ahead of market expectations. The Group's adjusted operating profit margin is expected to be c3.8% which is a further recovery of 200 bps on the previous year”…………

………………..Financial position

“The Group closed the year with a net cash balance of $95 million (FY23: $50m), a $45m year-on-year increase which is well ahead of market expectation. The Group was average cash positive for the year despite its traditional seasonal cycle of working capital movements. This improved cash position was driven by increased profitability and continued improvements in working capital management throughout the Group.

Moving forward, the cash position of the Group is expected to continue strengthening due to its financial performance and sale of freehold sites following footprint consolidation in the DG Americas division.

The Group expects to make a provision of c$5.5m* for potential liabilities relating to pre-acquisition era duties owed in the DG Americas division and is taking legal advice on the matter. Due to the historic nature of this issue, the results for the year ended 31 March 2024 will be adjusted accordingly.”

It’s worth reading the full results, it’s also worth reading the Canacord note from Tues morning, available on Research Tree. They suggest the forecasts eps for this year commencing (2025) will be 23c, or 18.9p at current exchange rates. So even after Tuesday’s price rise the PE is single digit. Canacord raised their price target from 275p to 325p and suggest a divi going forward.

I bought in on Tuesday, my bet is that the punters will be gobbling these up into the results in mid June. On Friday, broker consensus rose 20% on Stockopedia from 8.3p to 9.98p. The current year is unchanged so far at 18.9p eps forecast.

Worth reading the full results and the outlook, monster recovery potential imo

EAAS reported results on Tuesday, no fire-starters there but what really interests me is what LUCE gain from their 9% stake. They have been long standing supplier/partners to EAAS and now the contract sizes are set to grow much larger. LUCE have positioned themselves not to get out-competed imo. One such project was mentioned in EAAS results that LED supplier LUCE has likely benefited from

“Completion of new €5 million two-year project funding facility with Solas Capital AG to finance LED lighting projects in Ireland”

LUCE have their AGM which is usually combined with a trading update on May 14th.

Looking forward this week, after the bank holiday and a short week, the one I’ll be watching for is SYNT. Agm on Thursday, big bowl on the chart and on the current mkt cap it is trading at less than half book value according to Stockopedia so any sniff of better performance there and I think they could motor imo. A nice bowl on the chart.

I doubt I’ll be attending Mellow this month, a distinct lack of sun means I’d like to grab every opportunity I get to worship it this summer.

However, as readers of my Substack, you can have half price tickets to the event. Your discount code Rebel50 gives 50% off and the link to the webpage is https://melloevents.com/mello2024/

Mello are also offering those who have never attended an in-person event the opportunity to attend the event for £30. The code is NEW2MELLO24 if you are able to mention this, it would be much appreciated.

It’s a great event for private investors where you can glean a lot.

So that’s it for this week, looking forward to the coming week and the whole of May for results. As ever, all the above is just my thoughts. I’m not an analyst or financial advisor so do your own research, you are the one pressing the buy button. I hold many of the shares here and am biased.

Rebel

Looks a bowl, well bombed out, I was looking this am. If I wanted to increase my holdings I think I'd be tempted today.

Thank you Dinesh