Weekend Rebel Review, May 32dm, 2025

Who dares wins Rodders

Well it has certainly been a good plan to sell up ahead of Trump’s tariff and buy back, it looks to have worked this time, but doesn’t always. I seem to have dodged a 15% fall and am up around 8% from the lows, taking into account the cost of dealing spread and stamp, 2% of that on Thursday.

The FTSE250, up 14% from the recent low, in a month. If I’m going to trade out, I make the decision and do it heavy and fast before the fall, when I think it might be coming. I know trying to do it when the market has already given back 6-7% will likely cost me, you have the spread and the dealing charges to contend with and also less to gain in the bounce. I suspect a lot of novices sold right at the bottom. I did that once in the 1987 Black Monday crash and learned not to do it again. If you have done that, try not to beat yourself up, put it down as a learning experience. Build a plan for what you will do next time, even tho these things are never the same, there are similarities. Buying back in in small chunks means you can average across the curve and not buy on a short term high. As soon as any of the shares I had sold had fallen 10% I started buying some things back and banking that saving.

Here is the FTSE100, up 15 days in a row by Friday lunchtime, the longest winning streak ever if it closes up today.

When the market bounces like this, there are lots of punters that will have FOMO. Fear of missing out can make you do stupid thing too. I really can’t say how you deal with that, because psychologically, selling at the bottom then buying back higher is pretty alien even to me. I think I would start by buying back anything that was lower than where I sold, if possible, or little higher, but I can’t tell anyone what to do in that situation other than perhaps trickle back in on a stock over several trades so you don’t buy a short term top but average in.

Here is the FTSE250, it is one huge bounce created first by overseas funds and private investors moving cash from US and overseas to UK in part. After that you get the FOMO buyers that sold out at the lows or near to there.

Markets always bottom when investors are at their most gloomy. So many investors have thrown in the towel or run to the US where making money has been easy. The abandonment of the value in the UK showed investors were not thinking straight recently and forgetting that value matters. The VIX spike and the extreme fear on the fear/greed gauge was the buy signal in my opinion, just as it was with Covid, when the last punters capitulate, the smart money is buying – and that always happens before you see the positive news. With the UK it has happened just before the heavy May results period as investors buy to catch the up and coming results that are highly likely to be better than expected in many cases because so much bad news is priced in. Remember when everybody is expecting bad news it is hard to be disappointed just as when everyone expects great news, how can they get a pleasant upside surprise?

US GDP came in -0.3% Q on Q while +0.2% was expected. The previous read was up 2.4% but that was likely boosted by co’s heading off some of the tariffs and trading early. Meanwhile all the other data, housing, income and spending came in strong.

Geed/Fear has soared to 35 from 2 – and the 12% the S&P has gained demonstrates that you buy well when fear is at its highest.

The VIX demonstrates that in a similar way – that spike was the buy point – it never feels comfortable doing it but it’s usually the point where punters are selling in panic at silly prices.

Note that fall in the VIX and how it is starting to make a curved bottom – the bulk of the short term gains are likely done and now this chart will likely curve up for a bit in a week or two, hopefully only small ‘after shocks’ as more data comes out. If it makes anything that looks like a continuing bowl I’ll trim some positions but won’t be doing an ‘nearly everything sold’ again – those trades are for big highs and when risk is being ignored usually for me.

There will be lots of uncertainty in the market going forward but I think we will see, in the UK at least, a lot of companies beating expectations by some way and that will create anchor points for stocks on the climb up.

I think the UK could do fabulous when results start being published – punters with FOMO and funds bringing cash back to the UK from the US, with their tail between their legs. We have also had election results that have clearly told Labour they are toast if they don’t change tack, that may be worth a premium going forward.

On to stocks

I pointed out we were about to get hit by a ton of results – and out they came this week, Wednesday was manic but I’ve tried to cover all those that have featured here over the past in any significant way. After a quiet Monday, the results and trading updates came out of the stabled galloping, Tuesday onwards.

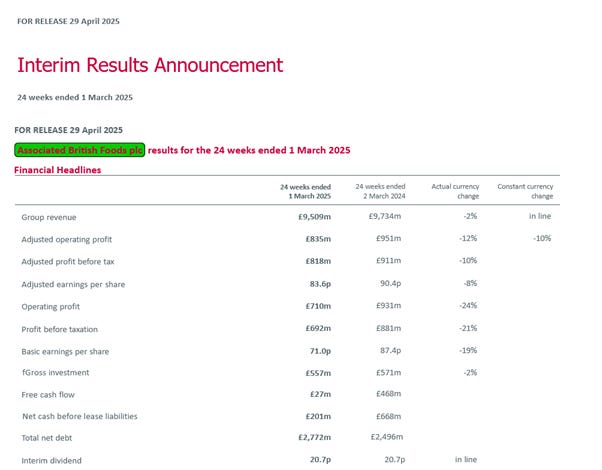

Associated British Foods, (ABF) posted their interims on Tuesday:

You can read the rest where you read your RNS News.

Sugar seems to be the drag while the company said retail had seen improvements in recent weeks. The retail side is the attraction if this has one for me, in that a stronger £ v$, lower shipping costs and perhaps a glut of capacity in China all play in that sides favour. I had only bought for the bowl and having accumulated over two dozen positions recently (far too many but there are lots of easy pickings at the moment). I decided to sell on the results and put the cash to work in other existing holdings, with the bowl pulling back, having already trimmed a lot:

They have a new CEO so that may be worth a bit of a recovery premium as investors hope/dream of better performance. I think the bowl has further to run but for now I’ve had the best of the rally and moved on.

I’ve been buying a few Aim co’s and adding to Aim co’s and small caps as I think this is the most under estimated sector of the UK. While mid to large caps rally strongest in early market rallies, the small caps then normally follow and these may be the most under estimated of UK stock. There is a lot of trash on Aim and even stocks that look solid have shown recently that they can spectacularly disappoint, but buying wisely for value, where directors have been buying and where I understand the business better than most other businesses, hopefully better than most punters for having done my research. That’s my aim here and there are lots with results coming up in May.

Watkin Jones (WJG) had their trading update for H1 on Tuesday:

I took that as a good statement. WJG earnings are very lumpy by the nature of doing large property sales and contracts. They are forecast to do 1p eps this year, 4p next year. That puts them on a PE of 8 for next year. Perhaps more staggering is the net cash which stands at £73m, £10m below he market cap. Gross cash at £87m is over the market cap! If someone was to acquire WJG today on their current valuation, they get nearly the entire cost of the acquisition back in cash which the company has, it’s like getting the business for free nearly. That is crazy cheap in my opinion, even with some of that cash required for cladding remediation, the fact is that’s been on-going and the cash has been rising at a pace, but punters seem to focus on just the PE. After being tipped in SCSW a couple of weeks ago, the traders jumped ship to chase other stuff racing away at the moment, like retailers. I like these a lot, there is huge potential for a bid with all that cash and the scope to put that cash to use could increase eps a lot. The new CFO, Simon Jones, has been doing a grad job since joining and both he and the CEO have been buying shares with their own real money. A superb construction sector holding for me and any rate cuts should benefit them greatly, which they have highlighted in their webcasts. I don’t think smart money will let these stay this cheap personally. The chart is one huge bowl and no share dilution in 6 years+. After the trading update the shares dipped but buyers moved in later this week and bought the bounce.

Of course I hold and I am biased, I would say all of this so do your own research etc and make your own decision.

Mpac (MPAC) posted their results for year end on Tuesday, which were inline with expectations

You can read the rest where your RNS news.

These results cover a period where MPC have made several acquisitions. They seem to be integrating well and forward forecasts are now pricing in the acquisition and the synergies. 44.4p eps is forecast for this year, a 30% rise in eps, putting them on a PE of 9.5. The order book of £118.5m is 63% up on prior year, helped by acquisitions.

In addition to this they say:

“Pension scheme valuation to June 2024 concluded with scheme valued at a surplus of £21.1m (June 2021 deficit £28.4m) and we are investigating options for the transfer of the scheme to a third party.”

With the acquisitions in place, MPAC can now deliver fully automated systems for businesses from the start of construction to the automatically wrapped pallet which should be very attractive to customers in my opinion.

Not having to lump out big payments to the pension in future would also help boost eps. Equity Developments have a share price target of £8+. There is a huge bowl on the chart too, which has had QITE A pull back from Trump’s tariffs in my opinion. There is a company presentation on VOX with Paul Hill and the co has put out a webcast on Friday

https://www.equitydevelopment.co.uk/news-and-events/mpac-fy-presentation-2may2025-

Do your research and know your risk v reward.

Jet2 (JET2) posted their trading update on Tuesday

You can read the rest where you read your RNS news. They said they continue to see late bookings which seems to be the trend these days in travel.

They also said:

The market liked it and the shares rose 179p a share to 1532p by lunchtime. The late booking comments boosted OTB too which has its interim results on May 13th. Well done anyone that bought the Tariff dip in early April. This seems to have been one of the first of the big rallies on results that I had said I’m expecting. Jet2 are up 50% in a month.

Warpaint London, (W7L) posted their year end results on Tuesday:

You can read the rest of the statement where you read your RNS News.

This looked a creditable set of results inline with expectations. Going forward they have the acquisition of Brand Architects to help increase earnings per share, currently forecast to be 26.5p eps and a PE of 15. The only question for me is how will their sales and profits and growth be affected by tariffs in the US? The company sees little direct impact but their may be counter party risk or knock on risk. This might be a bit of a drag but they are still net debt-free, and raised the divi from 6p to 7.5p. A PE of 16 for the current growth rate seems about fair value? Scope to beat though and that may be enough to push W7L higher.

Sticking with make-up - Creightons (CRL) announced the promotion of CFO Mohammed Qadeer to the board after 2 years at the co. It’s nice to hear the board are happy with the CFO at any time imo. Results are in July, directors have been buying in April just after the company year end. I tend to think directors have a good idea how they have done and what the outlook is like by year end. Pippa Clarke the CEO is a class act and has cut expenditure extremely well, she is also all over the subject when it comes to product knowledge having been brought up through the ranks.

The shares rallied 10% the following day. They did 1.6p eps in H1, if they did the same in H2 the historic PE is 10. They paid a 0.45p divi at year end last year, and likely net cash at year end. Perhaps a full year trading update soon before July results?

What’s the recovery potential with a bowl like this?

IG Design (IGR) posted it’s trading update on Wednesday – what a mess. I will leave the full RNS for you to read but here’s the sum up.

I came to the conclusion this board is economical with the truth at the last update, constantly trying to sound positive when things are way from good. Not a director buy in sight still. They ship from China to the US – they are going to get a groining from the tariffs in my opinion. I want to see a new board before thinking of revisiting having taken a whack from their unreliable commentary. Punters bought these on that update which tells me the bulls are in the market looking to buy small caps.

Carclo posted their trading update on Wednesday – here’s the outlook:

You can read the full statement where you read your RNS. What an excellent statement it was too, building on the pension news last week:

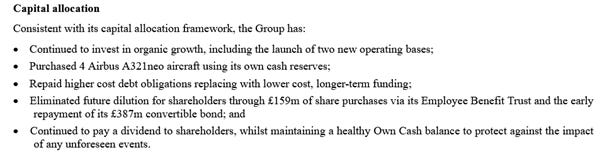

“Trading performance for the year ended 31 March 2025 exceeded management expectations, with strong margin expansion in the second half. Net debt (including leases) closed at £19.3 million, representing a significant reduction of £10.2 million compared to £29.5 million at 31 March 2024, reinforcing the Group's financial resilience and strategic flexibility.”

Was just one highlight. They also said:

“Key financial metrics demonstrate material progress towards our medium-term objectives, with notable improvements in Return on Sales (ROS) and Return on Capital Employed (ROCE) against our strategic targets of 10% and 25%, respectively. Cash generation remained consistently strong across the period, underpinned by enhanced operational performance, disciplined working capital management and strategic capital allocation.”

There’s a lot being said here without revealing the full results. As I said last week, I think Frank Doorenbosch is an excellent CEO and he looks like he may be delivering in spades. Should I have bought back last week? Definitely, but sometimes good news falls at poor times to receive it and I had got up to the gills in trades last week, I never wanted another small position. I have bought back in now though and will watch for the results the chart now looking rather exciting. That little bowl I ignored this time to my cost but never compound a mistake by not buying later, because your pride is hurt in my opinion. Looking at the forecasts, if they meet those then they’ll have done 3.2p eps in H2 approx.

They said last week they were paying higher interest on the refinancing but today, debt is down £10m so it will likely be on a much smaller debt. Margins much higher in H2 also sounds mouthwatering and inline with what CEO Frank Doorenbosch promised. The shares rose 12% on 500% normal daily volume nearly. I did my bit to assist that. The really interesting part of the statement is the higher margins, which was expecting, as they got rid of one US factory and moved production to another US factory so that seems to be a promise delivered. The other interesting thing they have, which Doorenbosch said they had started working on was their own proprietary products rather than making for others, this should boost margins even further when things start to flow.

A short term and a long term bowl on the chart.

Friday was a typical Friday results point with little to no real news of note – so that was this week.

Next week the real results will be out in droves and with co’s seeming to do mainly 3 day weeks as far as results go, then it will be some mad mornings with lots of reading to do so up bright and early, it’s the early bird……………………

On my radar for news this coming week will be:

7th CARD Finals

8th HTWS q1 trading update

8th NXT trading update

8th AAF finals

8th LORD final

Have a good Bank Holiday weekend, recharge the batteries, research those co’s and enjoy the coming month of results.

Rebel

Twitter @rebelHQ

A pleasure Jas, have a good weekend.

Thanks Richard. Always a fascinating read. Thanks for your patience in posting such a comprehensive and lucid article.