Weekend Rebel Review, July 27th, 2024

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.Well that’s the election over at last but really it’s just the start.

A bit shorter review this weekend as I spent a lot of time this week doing the Carclo Substack and it’s sunny, I can’t miss too much mankini time! One of the things I’ve noticed of late is, more often than not, I start the day weak and things pick up in the afternoon. That’s positive imo, it indicates investors buying into the close rather than selling, that’s optimistic trading rather than pessimistic. There’s a lot of giving back at times though, then getting the bounce, I definitely wouldn’t want to trade much in this market, buy and holds feel more comfy.

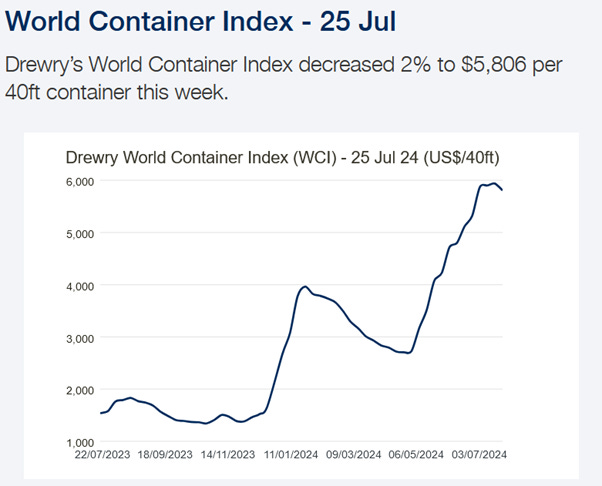

There wasn’t much major data this week that caught my eye. The Drewry Shipping Index has been rolling over a bit for the past few weeks. I would sort of expect that really, if companies haven’t booked most of their containers for Christmas stock by now I’d be surprised – that’s helped drive prices up imo. With prices having risen 200% then that’s likely helped to clip booking and stalling the container price. All this price volatility is just one more thing retailers have had to learn to cope with, which is why you tend to get great retailers and those that go bust imo.

Markets took a bit of a hit the past week as the S&P and Nasdaq sold off on disappointing numbers from Google and others. I love the way analysts work – they always say a company ‘never met their expectations’, they never say’ we over estimate what the company would achieve’ – classic blame shifting. Anyway, the S&P and Nasdaq were due a decent pull back so that’s healthy. The Nasdaq has given back around 8%, the S&P 2.5%, these are normal, pull backs. The good news is that’s taken Fear/Greed down to 39 – a nicer level to be a buyer.

There’s lots of EU inflation data next week and PMI stuff but very little from the UK aside from the big one, the BofE rate decision so that will be interesting. Ahead of that, the FTSE250 was firm on Friday, up over 2.2% and I expect small caps to follow soon.

After last week’s results from Carclo, CAR, the shares have motored on. I won’t bang on because I did a whole Substack about CAR this week. Suffice to say it was a great idea to ignore traders scalping on the results, the shares are up 50%+ from that pull back. Long term seller Equity First sold 2% and it looks like they were picked up by Schroders who already had 13%. Nearly a 4 bagger in 3 months so far, looking forward to further news from the company. Can’t imagine First Equity won’t be out completely soon with this demand.

Monday saw an RNS from Cardfactory, CARD with a holding notice saying long term share dumper and price destroyer Teleios had sold up. I’ve been waiting for this for 15 months. Even after selling out some time back I don’t think I’ve knocked the company and said that I really rate Darcy Wilson Rymer, CEO, as a top retailer. The shares took off on Monday, rallying over 10% and testing all those high over the past 15 months. A convincing break of 115p and the buyers will likely pile in in my opinion. With a PE of just 7.5 falling to 6.9 and a yield of 4.9% rising to 5.3% they look way too cheap for 10% eps growth each year for the next two years forecast imo. I bought back into what I think is one of the best retailers in the high street. There should be a trading update early August. Meanwhile, the acquirer of Teleios’s stake has been revealed as BBFIT INVESTMENTS PTE. LTD who’s founder is Brett Blundy, an Australian billionaire businessman. He is the founder of BB Retail Capital which owns companies such as Sanity Entertainment and Bras & Things. This makes CARD a whole new exciting holding on this low a valuation with a big retail investor taking a large stake imo. Cardfactory have long sold into Australia via the Reject Shop who they supply with cards on a wholesale basis.

A Google gets you various info on the guy but it seems in Jan he stepped up his global growth targets

Will CARD get a bid? Well I’m due one in my holdings - the last was Menzies nearly 2 years ago! If I were a retailer on the acquisition trail I’d personally be looking for great cashflow and on that basis CARD has always been a bid target imo.

Stockopedia:

Thursday saw CMC Markets post their trading update for Q1.

This is the Q1 update, it is only one month since the full year results so there was never going to be anything crazily ahead at such a short space since the results. Highlights for me was the increased cost savings to deliver margin expansion. The co has guided £320-£360m operating income.

In January they said this: As a result of this strong performance the Group now expects to generate FY24 net operating income of between £290-£310 million from the previously guided range of between £250-£280 million. If they hit the top end of their guidance they have hiked guidance and delivered £80m to £110m more in operating income than expected 6-7 months ago. That would be a 50% increase and growing margins from cost savings.

So traders of course scalped at the open because all they got was an ‘in-line’, but they were never going to get much better than that at this stage in all likelihood. The shares fell over 15p or 5%, then bounced through the day to close slightly up. I think with the B2B changes these have huge potential to beat and I’ll hold until I get the news whenever it comes.

Since November, earnings forecasts have been raised 150%

consensus raised nearly 10% after yesterday's update from 19.2p to 20.7p eps this year 2025 and 21.7 to 23.3p for 2026

In 2020 these were doing 30p eps on sales of just £252m.

So they started the day as my largest position and ended it there too, not a share sold – your carrots don’t become prize-winners if you keep pulling them up to see how they are doing. A lovely intraday bounce on Thursday, and a 7% rally on Friday. When you have researched your shares and the traders sell, you can stay cool and make a better decision.

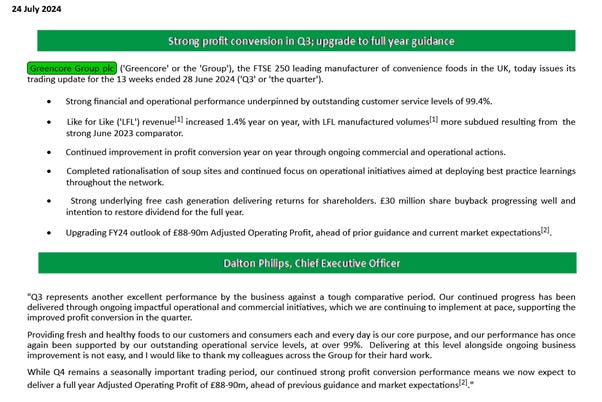

Greencore, GNC, posted a very decent statement on Q3 trading this week, stating that they were slightly ahead of forecasts:

The full statement is available on the RNS – the shares hit new 4 year highs on the news. First mentioned here in December they have since one-bagged, though I never bought and held till just over £1. I suspect these have a lot further to go but halved my holding to release some cash to go into other potential OBIAY’s that have greater scope to grow and recover faster, and to buy some CARD.

I did Mello on Monday and on the show was Alan Charlton who presented Spectra Systems, SPSY. I thought it looked a very low valuation and an interesting stock, in fact having held De La Rue a number of times I was well aware of it. I had always thought this was much more illiquid with only 8 mm’s up in 1k each but looking closer it seems far more liquid and some big volume moving through with ease. So I decided to take the plunge there with a bit of the GNC cash. Worth watching the Mello replay if you can get it. A 2025 PE of 7.7, earnings to nearly double this year and double next year after winning a huge contract worth $37.9 million to manufacture sensors for an existing central bank customer.

This week – results of note:

Filtronic CPI, have their annual results on Tuesday 30th July

Games Workshop, GAW annual results on Tuesday

Next, NXT and Rolls Royce, RR., Thursday

Capita, CPI, have their results on Friday 2nd Aug

Synthomer, SYNT trading update likely imminent and the shares were up on volume Friday.

So remember, I’m just a private investor talking my own book. I could be completely wrong, I am not an analyst. Do your own research and verify anything I have said for your peace of mind.

And so that’s it this week, a new high for the portfolio. The sun and dinner at the pub beckons - have a great weekend.

Cockney Rebel.

I dunno if it's an OBIAY, possibly, definitely a half OBIAY and depending on the performance, could be a lot more. It's a buy and hold for me, with bid potential, unless something far better comes along. Due a big re-rating as it has been stuck at this level for so long imo.

Thanks Richard

Must agree with the "starting weak and finishing strong" sentiment. At one point early on Thursday I was 1.9% down only to finish up 0.21%. Then followed by a fairly solid start to Friday which ended being up being 2.5%, the best day I have had in several months.......certainly helped by CMCX.

It feels like there is a positive swing happening