Weekend Rebel Review – Easter 2024

Nest Eggs having a cracking fortnight.

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

A short week this week with Easter upon us, so instead of looking at the macro, which hasn’t changed much, I thought I’d ramble on about how I manage my portfolio.

I was looking at various Twitter posts recently, where people have complained about their performance of late. We all invest differently and have to invest how best we feel comfortable and what gives us the best results. I’m pretty happy with the return I get. I expect to beat the FTSE250 and the Small Cap Index by double what these indexes rise at, at least over the year. I also expect to lose less than half the rate they lose at over a year, in poor years. Sometimes I’ll do a lot better than that, but I have never done worse than that, annually, since turning pro. Anyone doing this professionally should be beating the indexes by some way in my opinion, after all, you should know what you are doing if you do it for a living, you should have eliminated all the likely dross and you should be avoiding the sectors that have the least best outlooks. That on its own should mean you beat the index average.

My method is pretty simple. Invest well in what I understand and understand what I invest in well. I try to buy stocks that can grow very strongly and try to keep the number of holdings as near to a dozen as possible. At the lows of the market, where we are in now say, I’m looking for stocks that can one-bag in a year for them to be regarded as long term investments. As the bull market get’s longer in the tooth, one-baggers in a year become harder to find, so I’ll likely need to curb my ambition to half baggers in a year as the bull market ages, although there are always one-bagger recovery plays and special situations to be found.

I used to breed tropical fish years ago, South and Central American Cichlids, and had a method for finding the best, fastest growing, prize-winning fish. I’d watch carefully at a brood of around 1,000 fry or more, tiny little flea-like dots in the water. At the point of say two weeks old, they all look the same. As they feed and grow they start to establish themselves, some grow faster, they start to establish territories and bicker and fight. I’d separate out the biggest, strongest, most colourful hundred or so to concentrate growing on. Out of this hundred, you could not rely on the biggest 10 staying the biggest, you needed to watch for the dominant and those that might have the best colour and often there was never one that had the best of all features. I’d eventually whittle them down to 20 fish, some would be the best size, some the best shape, some the best colour. Eventually I’d end up with 6-8 that were the crem de la crem. These would go into my aquarium of breeding stock and that was the only way to be sure of getting the best, prize-winning fish rather than randomly keeping a dozen fry.

Picking a portfolio, I do similar. I can pretty much cull all the miners, pharmas, resource companies and stocks that I don’t understand and have no hope of understanding. Then I can cull all the penny dreamer dross on Aim that have no money, no director buying, loads of promise but little delivery and no near-term hope of being profitable and cash generative. There may be some big winners in here but for every winner there will be 20 losers. The odds are against me. If I miss a 10 bagger then so be it, I’ll also miss 20 wipe outs in all likelihood. I’d sooner let something grow to a point where I can see the size, colour and shape of the fish and know it’s breeding quality than take the too random approach when things are so small or difficult to understand.

So let’s say I have a dozen main holdings. These will all be potential multi-baggers in 12 months, at this stage of the market, a bear market turning to bull market. These dozen should be growing well but as they grow, their one-bagagability will be reducing, they will unlikely be able to double year on year for years. I need to be watching for new stocks, fast growing colourful new fry. These crop up all the time. A company has promise but has yet to show genuine signs of delivering. or a recovery play has seen a new board established, but no tangible signs that they are in recovery or can recover. I will likely buy small positions in some of these when they occur or at least create a watchlist of them. It may be after an RNS and news that catches my interest or a chart starting to turn up. I will likely then do new initial research to see if it has genuine potential. If the research looks good, I may add to the position. I’ll increase the research and delve deeper. If I find something that says the stock isn’t for me then I’ll likely ditch it as a trade whether that’s a profit or a loss. If you are trading, it doesn’t matter about selling at a loss if it feels right. You are likely selling other trades at a profit so you need to look at your trading average, not whether you lose on the odd trades. All the time I’m looking to hold a dozen one-baggers that I’m very confident of, but trying to find a few others that I can get increasingly confident that they might out-perform the winners I already have. Eventually, one of these will be clear and it will mean selling down what I feel is the most ‘up with event’ and more ‘spent’ holding and replacing it with the new, higher growth youngster. This way I can hold a dozen great growth stocks as core and a few ‘potentials’ in small amounts and gradually rotate. I know I am often selling stocks with a lot more left in the tank, but I’m looking to maximise performance from a restricted number of stocks. Adding more and more stocks just gives you an index tracker performance. Adding a new fast-growing stock with a 3% position and just increasing my holding numbers isn’t maximising the potential gains, I need to clip the runt of the shoal. It’s very much a Darwinian approach, survival of the fittest. Sometimes I’ll get it wrong. WOSG was a case in point and cost me 3% of my portfolio over-night. I remember though, as a small investor, I have one great advantage over fund managers in that I can likely close a position pretty instantly and build one fast. I rarely invest in small caps to an amount that I cannot get out of in a day or two. Fund managers need to build and reduce over weeks and months so private investors usually have a nimbleness advantage and you need to use your advantages. If I add a new stock and I think or discover I have made a mistake I am happy to reverse the decision, sell the new holding and buy back the previous one if it feels right. If you know you have made a mistake, reverse it. The worst thing you can do is make a mistake and compound that mistake by doing nothing about it other than holding on and hoping in my opinion.

So for me it’s about finding the 12 best growth stocks I can, taking into account reliability and risk, and weighting those 12 holdings to the ones with the greatest combination of those features and potential. Meanwhile I am always keeping an eye out for the up and coming stocks for the stable (aquaria, stables….it’s a ruddy menagerie here 😊 ) investing in what I find easy to understand and that means not just the business I invest in, but what is hidden out here with the competition. Keeping it simple, not being scared to dump a good holding if I find a better one but also not being afraid to reverse that if I get it wrong. I won’t be right all the time but using that method has got me growth at way over the main index performances and better than most fund managers if any. You do need to constantly do research though, things do change. There’s no free breakfasts unless you do the work, but if you learn to enjoy it, it’s not really work is it?

I’ve tried many ways to fine tune my investments to maximise my gains and this works best. A few will flunk it and get dropped, possibly at a loss. Some won’t be one-baggers but they will do well and make decent gains. Some will one-bag, but I may well sell them before they get there because something even better and faster will turn up and finally some will multi-bag. Some will multi-bag in a year or two. The harder bit is finding those stocks that can be one-baggers in 12 months and perpetuating that cycle. I’ll save how to find them for my book or my seminar 😊.

So onto current trading and the markets. The FTSE250 is firming but it really is like wading through treacle. The 250 has been creeping through resistance with little conviction but the buying is picking up. As the buying does pick up and fear reduces, will we see FOMO (Fear of Missing Out) ? I think there is a good chance. If shares do start a run up then I think funds are going to ‘panic buy’ to an extent, along with the punters. If you are a stock picker then there are always buys to be found.

RR. is up 40% since the start of the year and as it’s over 15% of my holding, that alone has added 6% to the portfolio on its own since the start of the year. CMCX which was 8% of my portfolio has one-bagged since January and that lovely bowly bottom. It’s now over 12% with the growth and having added more this week too. AVON and AT. are up over 20% since the start of the year and YU. is up 20% since the results 10 days ago when I bought. A couple of others are up 10% and I banked 10% on GAMA. TIFS this week was a let down on the secondary placing hitting the stock10% and BMY hasn’t stayed in profit for now. M&S is down about 4% from the start of the year but tons of bounce in it since a fortnight ago, bouncing 15%. All of that is all the more pleasing as the FTSE250 has gone little more than sideways since the start of the year. Making up the wallop from WOSG in January has been pleasing.

I’ve been holding GAMA for a month or two since they broke out and they posted results on Monday - 9 consecutive years of earnings growth, averaging around 20% per annum, £134m net cash, performing very well. I like them, but they are not going to one-bag in a year I suspect so sold mine to bank 10% over a month – I think I can find better, faster, stronger stocks. The cash went into more MKS, RR. and YU. If I can’t find a new potential one-bagger in a year and I’m not ready to increase my existing holdings then I often park cash in decent short term trades like GAMA, which I can just sell if something comes along.

I missed Journeo, JNEO presentation At Mello while I was on the stage with Andy Brough but reports back at the time from those that were there sounded interesting. They were very illiquid so I bought a small few a week or two later. The shares tanked shortly after, ahead of the trading update so I sold, not having yet had time to get really au fait with the company. They posted results on Tuesday and I couldn’t help but think I should have ignored the dip. The three year eps growth of nearly 100% p.a., very reminiscent of W7L and AT. Better researched I decided to enter here again, a little over where I sold and a bigger position this time to what I had a month or so ago. Very good results imo, and I have highlighted some of the headlines below.

JNEO are an information systems and technical services business focussed on public transport and related infrastructure solutions. They work with and provide solutions to local authority, Passenger Transport Executive to fleet operators of coaches and train transport. They say:

“We leverage the Internet of Things (IoT) and open data standards to support them as their new and legacy systems converge to a more efficient and sustainable future.

We work with a global supply chain of market-leading equipment manufacturers, niche specialists and support this with our own in-house research and development capabilities to deliver safe, secure and scalable solutions.”

Basically, they create and supply all the software and tech for transport co’s that coaches and trains need to supply data on passenger numbers, arrival and departure times, timetable display boards etc, everything which makes travel easier and more enjoyable for businesses and ultimately the public.

This is the 4 year eps growth. 2.26p , 4.47p, 9,8p, 17.96p. That puts them on a PEG well below 1 and net cash of £8m.

That looks a cheap stock on a PE of sub 14 and a PEG below 1 imo. The CFO added 8.8k on Weds @ 282p

It is very illiquid but it looks solid so I’ll likely add more to average in as the time looks right. Nick Lowe is the CFO – “I Love the Sound of Breaking Glass” 😊 You need to a 70’s music fan to remember that one.

Worth watching the final results webcast imo:

On Tuesday Luceco LUCE (pronounced Loo-see-co) posted results. I’ve held these before but sold recently. I’m not overly impressed with the company’s RNS saying a concert party had split in two so that one party could buy more shares without having to make a bid. I’ve not seen any RNS to say any one of them has added but I did see big trades go through after that RNS. Was it a pump to let someone sell out a large amount? I don’t know. What I do know is XPP and DIA have been struggling and LUCE seemed to be saying the Red Sea issues may affect them but other parts of the business were compensating. That wasn’t a compelling statement imo. I’m currently not holding. I think I can find better, faster stuff at the moment. There will be a time for me to buy back in I suspect, but I need better sentiment and a bit more faith in the co.

Ocado OCDO posted their trading update on Tuesday. “Volumes (total items) grew 8.1% year-on-year, driving Q1 Retail revenue growth of 10.6%, to £645.3m.” was the headline but what interested me was this:

We are delivering improvements in our proposition for customers, across unbeatable choice, unrivalled service and reassuringly good value. During the first quarter, we stepped up our efforts: enriching our product range with the strong growth of core M&S grocery lines …

The market liked that too – the shares soared 10p on the day. I think there will be a trading update from MKS soon.

Looking forward to this new ITV series about M&S too – 6 episodes, 6 hours of TV exposure.

https://www.theindustry.fashion/marks-spencer-to-launch-tv-series-to-find-uks-next-top-designer/

The bowl on the chart just looks great imo.

I mentioned having bought TI Fluid Systems TIFS last week. Sods law this week the largest shareholder, BC Omega, decided to sell 50m shares in a book build. Leaving them with. This was done at a share price of 135p, reducing their holding from 37% to 28%. I actually view the sale as positive as they no longer have such a large stake which could allow them to take the stock private without much of a fight from shareholders. The 135p is a crazy price tho. Now trading at circa 146p, that puts them on a PE of around 6 and a 4.8% yield. I cannot see them staying down here once the institutions that took that stock have sold what was bought to trade. But, the directors haven’t been buyers in TIFS shares. I’ll be looking to see if directors have picked up shares in the dip or took any in the placing. If they never then I’ll likely take the loss and move on at some point.

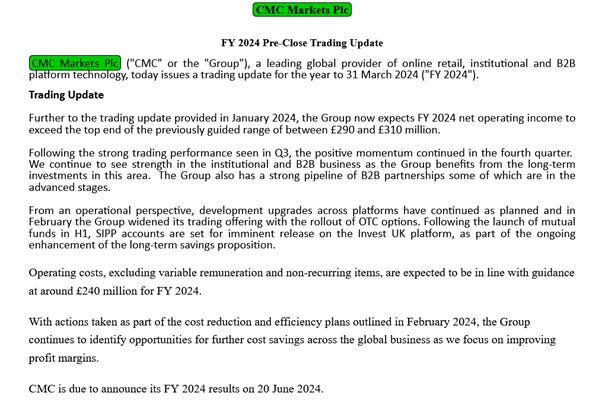

On the same day, CMC Markets, CMCX, the spread betting co, put out a positive trading statement.

The shares duly gained 12% on the news. CMCX had already said they would be ahead, then announced £20m cost cutting via job reduction a few weeks later. The thing to bear in mind is CMCX is hugely operationally geared. Saving £20m in jobs will likely add far more than £20m to profits. As sales grow earning grow even faster too. When you add that lot up, the current forecasts look like they may be way too low. On a fwd PE of just 12 for 2025, the reality may prove to be an even lower PE. In November they said this: “Interest income increased by £13.2m (464%) as a result of the rise in global interest rates.” This looks like a potentially well under-estimated stock imo. They made a small loss in H1 and are expected to do 10.2p eps for the year, so 10.6p eps in H2 before today’s trading update? 4.1p divi forecast for 2025 but could be higher imo with trading ahead? With the £20m savings going forward, even after 1 bagging in 3 months, I think they can one-bag again in another 12 months if not sooner, hence increasing my holding.

Lots of the new business is coming from a ‘strong B2B pipeline’ and the bit about introducing SIPPs being imminent and further cost cutting also looks very interesting and if markets pick up then who know what they could do? In June 2020 they did 30p eps on sales of £252m, they will be doing £310m+ sales this year and there’s 2.5% less shares now too. I added more on Wednesday and have now one-bagged those I bought in early Dec as that bowl started.

It would be remiss not to mention AVON just for the chart. It has broken out finally and the H1 period ends this weekend so perhaps some trading news not far off. On the 15th, Jefferies raised their price target to 1295p from 1150p with a buy rec. Half way to one-bagging these in 5 months – 1250p the next chart resistance:

There’s an old saying, “don’t put all your eggs in one basket” But the Warren Buffet saying is better imo “Do put all your eggs in one basket but watch the basket carefully” .

So it has been a great fortnight, from the start of the year I’m now up over 11%+ compared to just 1% or so a few weeks ago. I started the year needing a 40% gain by October to double the portfolio in a year. That looked a big ask a few weeks ago after WOSG hit, now I need less than 30% growth over 7 months to get there – it looks a lot more doable now. It’s a great value market here in my opinion – with AT., W7L and JNEO all with eps growth of circa 100% p.a. for three years running, I cannot remember ever having three stocks with that sort of growth rate let alone on PEGs so low, which makes me confident a lot of shares will see a step change in price before long in my opinion.

This is the point where I say do remember, I’m just a private investor winging it so you cannot trust me, you must do your own research as it’s you who hits the buy button, I am biased and talking about stocks I own, I’m not objective.

Have a great Easter and don’t get caught out on Easter Monday when people tell you the UK market is open this year – It’s April 1st 😊 And don’t forget to put the clocks forward on Sat night – Yipeeee!

Rebel.

Thanks for the Journeo link to the presentation Richard. What a very compelling case for investment! Looks like an amazing growth opportunity. I like the management too.

Straight talking seem to know what they are doing.

Happy Easter 👍🏼

Have a great Easter break Rich. Cheers, Whymps