Weekend Rebel Review 6th Dec 2024

CRL, OTB, CAR, BOOM, CARD, W7L. IAG LIO

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

Last week was the highest reads in one week for my Substack, 6.9k – thank you to the 3300+ subscribers and those that have passed the article on to others.

Last week I spoke about how I think the mind works. In life, either you control your mind or your mind controls you, you cannot let the latter be what guides your trading and investing. I said last week I feel an air of positivity coming into the market as a new year approaches. You have to get to know when people hate a share because that is without doubt the best time to buy. 10 years ago I use to post on ADVFN. I used to be amazed at how many people used to get excited on these threads as shares moved up. In America, with pyramid selling, they call them ‘sizzle sessions’, named after bacon frying and getting everyone’s taste buds excited. They have some water softener or cosmetic or whatever, they gather lots of new people to come to the presentations and there, the longer standing sales people, higher up in the pyramid, brag about how much they are making, how these things fly out the door, how you, the new average guy or gal can make loads of money like them. Hype to the max. Punters would go round ADVFN hunting down what was active, what was moving, what was being talked about the most. They are looking for instant gratification, buying and being in profit the same day is far more important to them than buying and making huge profits over months or years. I can tell you if you try jumping onto a stock that’s red hot, you are likely to get burnt and be the bigger fool that buys the stock right at the top. I know, because when I was younger, I did it too. And after getting burned a number of times I got into doing proper research. I would look for shares but things that had no sizzle. Part of my research would be to go onto the threads on ADVFN and I cannot tell you the joy I used to feel to find what looked like a great opportunity and then discover few or nobody was talking about it in months – zero sizzle! Chances were much greater that a given stock with little buzz about it was good value.

Later on I started to actively look for shares that were bombed out and created a recovery watchlist. Better still and with more experience I looked for hated stocks. Hated stocks are the crem- de-la-crem. These are the stocks that have so regularly let investors down that if they said the company had managed to grow gold ingots out of the CEO’s backside the share price would still fall due to lack of trust and huge hate.

But sometimes bombed out companies change. They get a new board or a special situation comes to an end and the fortunes change, but investors hate these companies so much they can’t even bother to read the news. I know, I have been there. These are the companies that bounce fast when you find them.

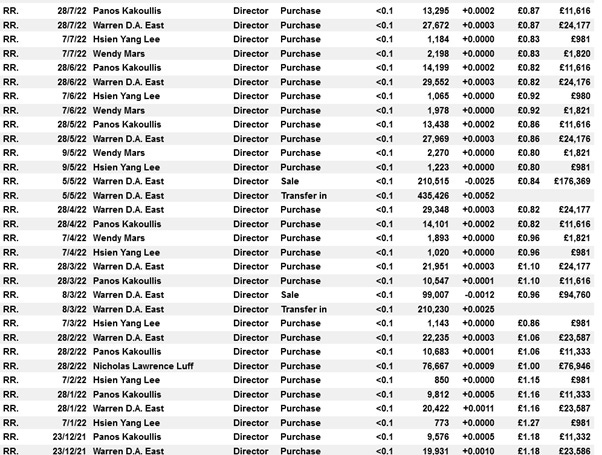

Look at this list:

This was the director buying in the first 7 months of 2022 @ Rolls Royce Plc. The shares halved while directors bought like they were going out of fashion, fund managers had been dumping them, they couldn’t buy a kiss on the cheek.

Two years after that low they have gone from 70p to 570p

I had ignored them, they were a big co that wasn’t on my radar that close, and what I had read from them looked like jam tomorrow. I bought when they had one bagged @ 140p when I had finally ditched my preconceptions. The market is full of shares like this now. The FTSE250 has gone nowhere in 6-7 years. Yep, we have had Covid, we had Brexit, we had Ukraine and we have had a couple of governments that have been useless. But now I feel Labour have got the message – they have been clearly told that if they are going to lump NI and greatly higher minimum wage onto business, business is going to pass it on and their actions are going to come back and bite them on the backside with inflation.

So for me, I feel that a lot of well performing companies are about to reveal themselves in the January trading updates. A lot of poor ones will reveal themselves too but I expect many of them may not fall much on mediocre news while good results will get rewarded. Time to be a bit braver before the crowd because when co’s do start posting great results the crowd will jump aboard and chase the stock higher imo.

It’s not just the stocks, it’s the macro too. I cannot imagine there are many investors out there that are over optimistic for the market in general, with all what Coco the Clown at No10 and Billy Smart’s Cabinet that help him run the show are doing. Starmer has the worst approval rating ever, all squeezed into 5 months, anyone investing in the UK cannot feel great, chipper or over confident. That’s another great indicator that many businesses here are lowly rated. Of course, things can always get worse and if overseas and the larger macro were to turn bad, it could drag the UK down further.

It's interesting that as the US is breaking out through decades high resistance, the FTSE100 is doing so too, that is one big positive to cling to imo:

The FTSE100 hit 7k at the turn of the millennium and took another 12 years to break that level but now the 100 has moved on up beyond 8k even with a government hostile to fossil fuels.

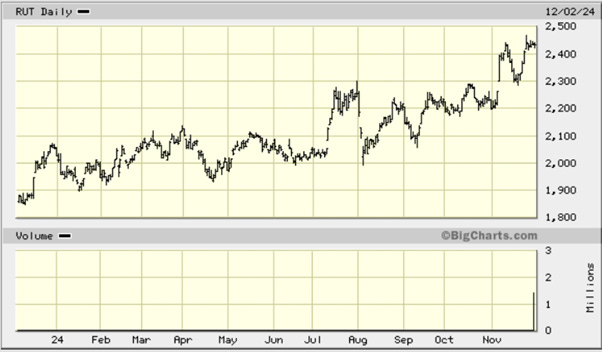

Still on the Macro theme, it’s good to see the US Russell 2000 Small Cap Index hitting new highs – a positive for small caps here imo, and if you follow the lows they are curving up which means they are gaining momentum, cash moving from Fangs to small caps perhaps?

Meanwhile, the FTSE250 and Small Cap Indexes have been creeping out and up from what looked a roll over potentially, that’s positive.

These could still fall and the roll over carry on but they have bounced off support.

When markets bottom you get the big one day bounce but often there is sharp profit taking. This is normal, many traders/investor have been losing money for months and the temptation to bank a profit is huge. As you start getting more frequent decent up days, the profit banking turns into regret at not holding on, so investors start to get more confident and hold longer. This is how bull markets are birthed. If we start to see more and more firm days, off more and more OTB type beats (more below) on results, then a bull run or a bull market will likely occur. We shall see.

Lastly, if ever there was an index in a trading range it’s Aim If this breaks out it really is a bull market starting:

And so onto stocks.

Creightons published their post results presentation on Tuesday, it is well worth watching imo:

https://www.piworld.co.uk/company-videos/creightons-crl-interim-results-presentation-november-2024/

Lots of the slow moving brands have been curtailed and new brands coming along on the branded side. They have dropped a number of Contract manufacturing customers who looked shaky and are replacing that with fast growing business, higher margin business from Private Label.

Pippa looks very confident and all over the products and the business, better than Johnson used to be. I don’t think they want to over-promise after he had his crazy year too.

An apology – I said last week Blossom and Bloom were a Creightons brand, I think I was thinking of Feather and Down – it’s so long since I used a good foundation 😊

I’m pleased with progress and suspect they will rally when everyone least expects.

I have been saying that there will be some big upside surprises for stock with the way they have been ignored. I pointed out the bowl for On The Beach, OTB, here last weekend, ahead of the results on Tuesday. You can’t say this co name without thinking of Chris Rea. I was once asked to leave my restaurant table quickly because he had come into the restrarunt and wanted a table! That story is for another day, I digress. Results were inline, with PBT up 25% and the shares up 25% in a day too – which was very nice, and sure enough they closed up 20% on the day.

You can read the full results wherever you read your RNS. With profits up and margins increasing together with a newly launched share buyback post the results, and a 3p divi for the year, the shares duly soared 25% on very heavy volume.

With 18.1p eps forecast for the coming year and a £25m share buy back reducing the shares in issue, then @ 209p they trade on little over a PE of circa 11. for this current year and order book at record levels. On current trading, with nearly 3 months under the belt they said this:

That all sounds very confident. The company has doubled its addressable market and moved into Ireland after settling it’s legal dispute with Ryanair. With profits rising at 30% and on a PE of 13, at 240p a share for the current year, that’s very strong growth for that PE without any upgrades, in fact going forward it looks even better - 13.9p eps just achieved for 24, means the 18.1p eps for 2025 now forecast is 30% earnings growth this year on a PE of 11, that's a PEG of 0.36, extremely low if you follow Slater’s PEG valuation. The shares have a bit of a fan club and tend to rerate pretty quick on positive news. The next trading update is in 7 weeks time around Jan 26th, so it would be my bet these are in demand as the next update approaches. Possibly a very decent one to hold here with a 3p divi for the year, great cash generation and cash balance too with NET CASH of £96m, and share buy backs.

Have a look at the chart above. The first circle in early 2023 the eps forecasts were for less than 7p eps and no divi. Where I have circled today, hardly any higher than 2 years ago, the eps forecasts are for 18.1p and they will be doing £25m buy backs and paying a 3p divi. Historically these are massively cheaper than they have been in the past still, even after the rally this week.

The great thing about recovery plays is they have a history. Look at the chart, OTB’s highest ever eps was 21p in 2017 – the 18.1p eps forecast this year isn’t far off and next year’s eps of 21p+ and matches that highest ever eps. Just 25% share dilution. That would make the old high around 500p in new money. By Thursday OTB were up 40% on last weekend’s bowl highlight. There’s a lot to like here, I suspect these could easily be an OBIAY even after this week’s rally if the market behaves in general going forward. The co also said this:

NOTE: Medium term ambition

The Board is pleased to set out the Group's medium-term ambition to deliver:

TTV of £2.5bn.

EBITDA of £100m (40% of Revenue).

Adjusted PBT of £85m.

If they do this they will hit 35p eps, nearly double this year’s estimates. To hit £85m pbt in 3 years say, would be 30% compound eps growth over those 3 years.

I built a 10%+ position in these over the first three day after results which isn’t easy while the stock was just rising relentless..

Don’t take my word that these are cheap though, do your own research, I’m biased having bought last week and added more this week, I’m already miles into profit so don’t trust me blindly – do that due dilly and feel comfortable with what you buy, buying is your decision remember.

Carclo, CAR, posted their interim results on Thursday which read very well in my opinion:

You can read the full statement where you read your RNS news.

I was rather pleased with the results, eps in H1 was 0.7p v a 0.5p loss in H1 last year.

Debt was down by over £4m to £25.25m/

They are still making payments into the pension deficit. A big headline was “Return on capital employed (ROCE) increased to 17.5% (HY24: 8.6%), underscoring continued discipline in capital expenditure and working capital management.”

You cannot account for jumpy traders in this stock and the share price came off 8% at the open. I don’t suppose they had read the Liberum note that came out with the results raising their target from 32p to 47p.

The presentation at 9am on the same day was more enlightening. It is worth watching, they are firing on pretty much all cylinders. There is still a lot more modernisation needed but as they increase EBITDA and reduce debt they should start to see a multiplier in the financial gains.

The pension triennial revaluation finalises in March, that is expected to reduce they said at the last update.

Liberum now forecast 2.4p eps for this year, 5.2p eps 2026 and 8.3p eps in 2027. That is strong earnings growth and from a low base it has scope to grow for some time at a decent clip imo.

The traders selling on the news will dry up and the shares should then firm. I’d watch the presentation on investormeetcompany, it was very good in my opinion.

CAR has been a great hold, anyone that got the lows in April are up 300% still in 8 months so there’s going to be peeps that want to bank great gains, especially as the market seems to be firming.

https://www.investormeetcompany.com/investor/companies

Audioboom, BOOM

Audioboom Group is a Jersey-based podcast publisher. The Company’s advertising and monetisation platform underpins a scalable content business that provides commercial services for a network of 250 top tier podcasts. Audioboom technology platform connects advertisers with content and distributes to audiences globally via Youtube, Spotify, Pandora and Apple Podcasts. Here is one helluva potential recovery chart for you:

I have kept a watch on these for some time, two and a half years in fact. These are not my normal thing but having watched and held them in the past I know what they do and it’s a simple business model, they provide the tech infrastructure for podcast and earn from the advertising. These got to making a profit in 2021 but some onerous contracts caused them issues during lock down that had certain minimum guarantees. These legacy contracts come to an end at the end of this year I learned this week watching the video below.

Watch this video with Paul Hill and Laurence Hulse who estimates it could be worth 4 times the current valuation but take that with a pinch of salt till you do your research:

This was quite interesting to watch and a few bits that I wasn’t aware of are on there.

What I actually had noticed is that the co is now expected to do 11c eps with the recent upgrades after ‘ahead’ trading updates. Interesting because they lost 8.2c in H1 so to meet expectations as they say, they will do 19.2c in H2, making the 13.2c forecast for next year look very doable. They said by Q3 they had done $1m EBITDA, by Q4 they said $2.8m EBITDA, that’s $1.8m EBITDA in Q4 alone when they are expected to do EBITDA of $3.49 for the whole year ahead. The co has a year-end trading update mid-January. While the co has net cash of circa £2m, and the Chaiman, Michael Tobin has regularly bough circa £10k shares almost on a fortnightly basis for the past 3 years, he now owns 5% of the £45m co and lacks no confidence. His top buys were at £18 a share and he has continued to average in constantly on the way down. The shares are very illiquid and can be volatile so know your risk reward and do your research. I have built a moderate position to see what the Jan update brings.

One stunning bit of news this week came from Cardfactory, CARD. The company announced a strategic acquisition in the US which will be paid for out of existing cash and some debt. This wasn’t the stunning news though, it was the trading update that came with it:

CARD was trading at 140p in September and plummeted on results because the H1 profit numbers looked weak despite the company saying things were inline. UBS had raised their target to 180p from 116p just the day before so the crowd were expecting fireworks. Immediately traders dumped the shares, trigging a big fall. CARD has picked up a big retail following from private small investors too and fear spreads fear.

If CARD are inline then they are set to do 14.4p eps this year and 16p eps for the year ahead that begins Feb 1st. That puts them on a fwd PE of 6.1 and a yield of 6.26% and trading at near half UBS’s 180p target here.

Mad markets and frightened investors often create superb bargains. There is one heck of a bowl on the chart too;

I bought back in a week ago and increased my holding this week after the trading update. Even after selling out I never once thought Darcy was anything other than a great CEO and posted that here too. Sometimes you just have to go with the flow on the way down and on the way up when traders leave or return en-masse.

It’s worth remembering CARD said this at the interims:

“HY25 Adjusted PBT was down £7.6 million to £14.5 million, reflecting substantial increases in National Living Wage, plus freight inflation and phasing of strategic investments. As previously guided, the benefit of our strategic investments and robust programme of productivity measures and efficiency savings in FY25 are weighted to the second half of the year and we have already seen these positively impact the cost base.”

They haven’t disappointed regarding performance, punters just over-reacted imo and never even took the above into account – shoot first and ask questions later, as traders often do. Well worth researching in my opinion. As a side note, the CFO bought 21k this week, after the trading update.

IN BRIEF

After pointing out the rising charts for travel co’s like JET2, CCL and IAG a few seeks ago, the chars are all breaking out nicely. IAG, which I highlighted the bowl on at 240p got yet another two upgrade this week from JPMorgan and Bank of America:

“JPMORGAN RAISES IAG PRICE TARGET TO 5 (3.40) EUR - 'OVERWEIGHT'”, that is the equivalent of 414p, 50% above the existing share price.

“BOFA RAISES IAG PRICE TARGET TO 370 (300) PENCE - 'BUY',” That is 70p over the target price they announced of 300p, a month ago, up from 240p prior – that’s a lot of brokers upping the targets significantly, by 50% over a month from both of them. The curve up is a chart to die for.

Warpaint, W7L are to acquire Brand Architekts for £13.88m They announced on Thursday. Brand Architekts seems to have been run fast less efficiently and likely offers an opportunity for W7L to increase that significantly bringing it into their business model. W7L are raising £14m @ 510p a share, rather good and not much of a discount to the market price. The co also gave a very decent trading update:

The shares have been bouncing off a great support level her and I bought a few back at this level:

Watches of Switzerland.WOSG had an HI trading update this week too. While the co said they were inline, with expectations. With H1 down on last year re EPS that looked a bit of an ask so I ignored the rally to my cost. It has had a strong rise and broker upgrades. I’ve been watching the Rolex price charts and they are still falling which makes me cautious but well done to those that caught the rally.

The past couple of weeks has seen real positivity in some consumer stocks, HFD, CARD, OTB, WOSG, IAG, to name a number. Perhaps the market is working out that hitting business with higher NI doesn’t hit the consumer till the next financial year, so perhaps enough growth between now and then for escape velocity to be hit with consumer stocks? I don’t know but there may be more big positive surprises from consumer stocks if so.

And finallly……….Bowls of the Week - Liontrust, LIO:

Results that were much more upbeat two weeks ago, immediately followed by the CEO and CFO buying 100k and 50k respectively, £380k worth. A PE of 7 and a 15% yield that has been maintained @ 72p ”Our confidence is reflected in the fact that we are targeting the same dividends as last year and have announced a share buyback programme.”

Bowl of the Week II - Sabre Insurance SBRE

A capital markets day on Thursday said they were inline, directors have been buying. Nice bowl on the chart and a great yield with the special divis they pay - £37m net cash, no debt.

And that’s it for another week.

One of the most encouraging things this week, was, CARD and W7L acquiring in the US - they will compete against ELF and American Greetings – It’s UK parking it's tanks on America's lawn for a change! 😊 And why not, it makes sense, be more exposed to US growth and taxes than here in the UK which has a government that doesn’t understand business.

It has been a great week, up over 3% this week after giving back 8% over the past few months, that hasn’t happen much recently. I hope some of you caught OTB last weekend before the results and the 40% increase this week, that was one bowl to ride! SAGA from last weekends review rose 10% on that bowl too, just CAR with a short term trader scalping being the disappointment but they can’t all be instant winners.

I will be doing Vox Markets Live on Friday at 9.30am if you want to watch, always good fun I find.

Have a great weekend

Rebel

Hi Mark,

I am going to disappoint you but although I know about it all I just don't pay attention to banks and financials usually because they are too complicated as a business to understand unless you specialise in them. I try to stick to simple tuff like consumers, manufacturers, builders, simple models where yo can full understand them. How banks earn their money seems very divers and complicated so I just give them a wide birth.

Sorry I can't help any more than that.

Hi Laneo74

You are right, I do both. On occasions where the stock might look everyone is aware of and it starts moving up I might just pile in and keep adding as it goes up.

If the stock is quiet and I have some time, I try to buy so much that I don't move the price, than I average in, whether that is averaging down or averaging up, I just prefer to average as it stops me buying at too high a price then seeing a pull back.

More and more when I feel I I have found something very good like OTB I try to go in as big and as fast as I dare or else these things get away before I can get a sizeable position and averaging up destroys a great initial buying price.

Always try to average up on dips, even if they are only intraday,it make a big difference imo

Richard