Weekend Rebel Review 23rd Nov 2024

#BOY #AVON #CMCX #JET2 #CRL

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

Well the first snow here for 2 years which is very early, something you don’t see often this far south – must be global warming 😉

Out a tad early this week as we are dinner partying tonight.

Tough markets can grind you down but it pays to reduce your expectations and focus on beating the market as much as you can in my opinion. If you can set yourself a benchmark to beat then you can decide how you are performing on a personal level and whether you are doing the right thing. I’ve always set myself against the FTSE250 and the FTSE Small Cap Indexes as these are the main to areas where I invest. If you can beat these indexes on the up and control your declines enough to out-perform on the way down then you know that longer term you can beat these indexes significantly as a whole. Over time you should do well on that basis, especially when you take into account compounding.

Year to date the FTSE250 is up 4% - hardly exciting especially when you take inflation into account but if you have invested in the right sectors and avoided the poor sectors you should have bettered that. The FTSE Small Cap is up nearly 6%. Both indexes do have a lot of divi payers though to offset that inflation at the moment. Charts are good for telling you what sectors to be in in general imo – investing in sectors where the trends tend to be going up and avoiding the sectors which are trending down can usually help you beat the index. Invariably there are outliers though and having a spread of stocks helps prevent you being unlucky and having all your eggs in one basket. For beating the indexes even more, nothing beats research and finding an outlier to the upside. Over the past two years the stand out for me has been M&S and Rolls Royce – without going heavily into those two my performance would have been far more mediocre. The difficulty is finding these outliers early as they are quite few and far between in a difficult market. This is why I like recovery plays because they have the greatest potential to surprise when others have written them off. There is always a wide field to search for whether they are long term decliners or companies with short term issues but it takes a bit more research to sort the wheat from the chaff. Try pitching yourself against your nearest index to how you invest in my opinion.

Markets like this are tough. If markets are clearly falling you can just sit it out. If markets are racing away you can just go all in. If a market is going sideways there’s enough to tempt you because there could be some sparkling rallies but there’s also the likelihood of getting slapped. I call it a ‘Burlesque Market’ – it shows you enough to get you interest but the clothes never come off completely.

Inflation data was out on Weds, CPI coming in higher than expected at 2.3%, while 2.2% was expected, already above the 1.7% for the previous month. Not good for the government but retailers do a lot better in an inflationary environment imo. With retailers wanting to push through the NI rise, they’ll do it easier with inflation already picking up imo.

As much as investing is about research and knowledge, you need an element of luck too at times. Last week, luck was against me having sold out of Burberry before a 17% rally. This week the swings and roundabouts worked more in my favour.

You can read the rest of the statement where you read your RNS announcements. At first glance it might not sound that exciting but the shares have been bombed out when the earnings forecasts have hardly fallen. Listening to the previous results presentation, the co had had a huge write down on their ERP software being implemented by SAP and they had cancelled the order which had been ongoing for something like 5 years I think they said. Circa £26m write down was large. Going forward though, I guess that’s £5m a year or so that won’t be spent. What they do about their upgrade to ERP then on is the next question, is this a short term cost saving that needs meeting head on again at some point? They also highlighted the strength of their aviation business. With a new CEO at the helm and the Chairman recently increasing his holding with a £200k share buy they seemed worthy of a ‘punt’ with the shares off nearly 30% since April and a small bowl forming on the chart. Thus I was pleasantly surprised to get a trading update that was inline. The forecasts are for a 10% rise in eps on last year @ 49.3p compared to 43.9p last year. A PE of 12 falling to 10 is historically very cheap for BOY imo. With a divi yield of 4% and share buybacks ongoing. I will have to see how long I hold, I wasn’t expecting to be holding them a week ago so haven’t done the research I need to feel comfortable but I’m in no rush to sell at the moment. Up 7.5% on Tuesday statement, it will be a short to medium hold if anything.

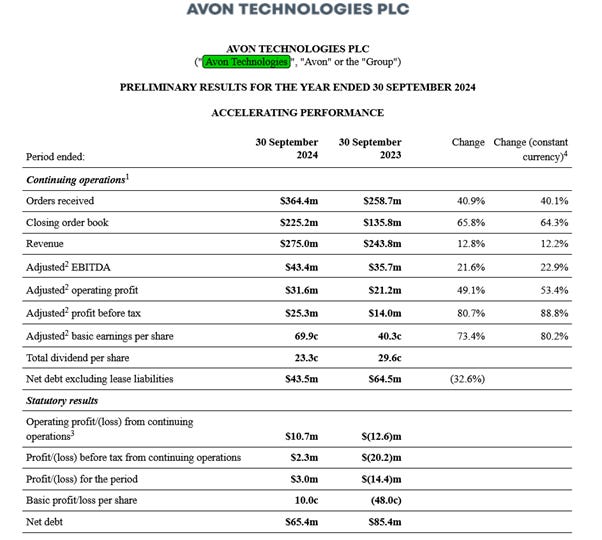

BOY wasn’t the only bit of luck this week. Avon Technologies (formerly Avon Protection) has been a great holding for me in the recent past having bought sub £7 in November last year and sold out between £13-14 in the summer when they doubled and the share price looked like peaking. As luck would have it I saw Avon rallying strongly into the close on Monday, ahead of their results so fortunately bought a number late Monday. Pleasingly the results were excellent, leading to a 9% rally by 10 am.

The full results can be read where you read your RNS and I would definitely watch the results presentation on the company website, it is an excellent and very positive watch. With record order books they are clearly doing well but listening to the factory changes, reduced foot print and the change in production from batch production to constantly moving production line working.

There was a lot of adjustments with all the factor changes and the new ways of working but listening to the presentation and after they went heavy on capitalisation this year then there should be minimal adjustments going forward from what they say.

With the global tensions and the civil unrest in places, as horrid as all this stuff is, there’s some great sales opportunities for the company. They are also a pure ‘defence business’ in as much as they only make defence products, not offensive products so conscience wise they are not the potential ‘killing’ equipment that many defence co’s make.

The whole presentation was upbeat and positive and the increase in the final divi was a statement of confidence imo. They also allude to doing share buybacks in due course

The shares broke out to a 3 year high on Tuesday, there has been no dilution since that high @ £45. Having done 69.9c adjusted eps this year, which was forecast for the coming year, they seem to be well ahead on the face of it.

Note the change of name from Avon Protection to Avon Technologies – I think that leaves them to enter a greater scope of products rather than sounding like a rubber protection business which the name always seemed like to me – let’s not get onto contraception ah 😊

Selling out of Avon and buying back in after 6 months has worked for me on this occasion, offsetting the missing of that BRBY rally last week – and that’s how it goes, you win some, you lose some but you need to keep playing the game if you want to win longer term imo.

I posted a Substack in January regarding AVON, it has risen 70% since – it can be found here:

https://cockneyrebel.substack.com/p/avon-protection-plc-avon-f35?utm_source=publication-search

CMC Markets, CMCX – a stock I sold after one bagging in under 12 moths this year, posted interims on Thursday:

The results were strong and the bowl on the chart hit an initial new recent high before punters decided to sell off. I’m not sure what was disappointing in the results other than punters expecting even more from H1. EPS of 12.8p was well above half of the forecast 20p eps for the year. Seems an odd reaction but Thursday was rather strange for selling, it seemed like a day where there was almost punter panic selling in the market. Perhaps pensions have been getting squeezed a bit again by the higher gilt yields and inflation coming in higher than expected? The stock came off 15% through Thursday morning which seems crazy. I had bought a few back the day before the results and doubled my holdings down at the lows on Thursday. I’m not sure but the market is starting to feel decidedly volatile this week and the FTSE250 is rolling over more but still on that rough support area:

I posted the chart for Jet2, IAG and CCL last week – all three are travel shares. IAG I have already covered and the 6 recent strong broker upgrades, it has been performing strongly. Thursday saw JET2 release their interim results.

You can obviously read the full results on the RNS but suffice to say while full year earnings growth was forecast to be 4%, H1 eps was actually up over 20% meaning the trailing 12 months are now way over the current forecasts for the year. The company says it is trading ahead of forecasts.

The cracking bowl on that chart telegraphed the good news in my opinion. The shares raced up 150p or 10% before pulling back to 6% up.

I covered Creightons, CRL last week. A couple of interesting points before the results on 29th Nov.

Firstly, the recently gained M&S as a customer. Two of Creightons’ products featured in the M&S for their £300 cosmetic advent calendar, one Blossom & Bloom and one Emma Hardy, as shown in the picture above which I grabbed from the TV on Weds M&S programme on Ch5:

Also Emma Hardy products are now on the M&S website and get a lot of 5 star reviews

as does Blossom & Bloom

So I’m expecting CRL to have decent news with the results on 29thNov.

That’s it more or less. I see Argentina have turned a $888M trade surplus in October 2024, rebounding from a $442M deficit last year. Exports soared 30%, fueled by agriculture and manufacturing, while imports grew 4.9%. They have done it by cutting government spending. We really are out of sync with where other economies are going and prospering in my opinion. The issue is so many young people today don’t remember Thatcher let alone Callaghan and Healey. It’s all very well having the wokey stuff, the higher living wages, taxing business and thinking they won’t raise prices but we are already starting to see job losses across the country. Job losses harm confidence and weak confidence causes recessions. The retail PMI numbers were very weak on Friday

Time to watch the macro. I really don’t think Labour understand basic finance and confidence isn’t bolstered by learning Reeves wasn’t an economist, just a back office girl in a bank. Watch gilt yields and the pound imo.

It’s a difficult time to make money investing and if you are finding it tough, try playing with a much smaller holding for a time perhaps, until you start making money again and then increase your size perhaps. The FTSE250 and the Small Cap Indexes aren’t looking that healthy, with big roll overs, so play safe until those indexes make a clear change imo.

That’s it till next weekend, Have a good weekend.

Might be a shorter issue next weeks as we have builders here starting work so I need to break them in.

Rebel

A CMCX comment today that might explaIn the fall. At CMC Markets, we are proud to partner with StrikeX, a dynamic and innovative leader in blockchain technology. We believe strongly in their vision and the transformative potential of their solutions, including advancements in self-custody, tokenisation, and blockchain infrastructure through StrikeX Labs.We would like to address a recent news article which misrepresents our commitment to StrikeX and its strategic objectives. The write-off of our initial investment is purely an accounting decision and does not reflect our belief in StrikeX's technology or potential, nor does it indicate any change in our partnership.On the contrary, we continue to integrate StrikeX's services into our offerings and see our relationship deepening further as we collaborate on Web 3.0 developments. The team at StrikeX has made tremendous strides in this fast-paced industry, and we remain excited to grow alongside them, supporting their mission to reshape the future of finance.CMC Markets is committed to fostering innovation and partnerships that deliver long-term value, and StrikeX remains a key part of that vision.

When very well thank Pauls, great night, loads of bubble :-)