The Weekend Rebel Review, June 28th, 2025

Breakouts everywhere. #SAGA #OTB #FTC #KLSO #WRKS #THG #LIO #TIME #LIO #LIKE #KIE #KITW #CURY #WOSG

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

Expect some spelling mistakes – I’m dyslexic and in a rush to get this out on a Friday so a bit of a task at times.

Pretty amazing ah? The US bombs a middle east nuclear facility at the weekend and the S&P opens up 30 points on the next trading day. Like I said last weekend, I wasn’t selling on the Iran news and mot many others were and this weekend, punters are buying on the first sound of bunker busters. Private investors have got smarter, they have seen all the past wars and incidents and know any selling is likely knee-jerk and short lived, we have become desensitised to these things. That isn’t to be totally complacent about them, but to remember, panic selling provides opportunities in many cases. If Iran retaliates, they are going to get an almighty hit from the US. The mullahs that give out the commands from their deep, James Bond style underground lairs are no longer so safe now they have seen what bunker busters can do, hiding might no longer be an option if the US know where you are, even if it is 300 meters below ground. Things seem to have settled down and by Friday the S&P had made a new all-time high.

One thing I would pay attention to is the £ v $. Over the past 6 months the £ has appreciated v the $ by 10%. Any businesses that purchase in $ are likely doing well out of this or hedging their forward purchasing at a much better rate than last year imo.

Meanwhile shipping costs priced in $ have fallen by 25% since the start of the year – a double whammy win for retailers perhaps.

On Thursday, the FTSE All-World made a clear break out of the rolling trend – for me this is a very positive macro indicator and seems the s shrugging off the eventual outcomes of Trump’s tariff deals. TACO been priced in? (Trump Always Chickens Out).

I was asked a question this week, how long to hold a share. I’d say I hold as long as I feel confident and as long as I can’t find anything better. At times when the market is wobbly, cash might be that something better. Until then I try to run stocks as long as I feel confident or something changes. I occasionally short term trade but the spread, dealing and stamp all eat your gains away if you trade frequently. Trading requires too much stock-watching too. Poor news for a share can make it into a trade rather than a hold for me though and news is one thing that always makes me focus on how I feel about a stock and whether I add or reduce. I rarely buy or sell in one go, spreading your way in and out averages your buy and sell price. Selling the whole holding in one go is for proper bad news and then I usually average out over a day. Stocks are like carrots, if you keep pulling them out to look at how they are doing, they never grow into prize winners. If you do research, you know what you are buying, you can place your valuation on it. And you are confident then you have to try hard to buy and hold for a decent timeframe imo.

Onto Stocks

I highlighted the bowl forming on the chart in the June 7th Rebel Review.

June 7th

On Tuesday, Saga posted their trading update:

This made a very welcome update for many I am sure – each highlight was positive and there were no ‘however’s. The CEO of 1year 9 months, Mile Hazell has arrested the decline in the share-price and since Euan Sutherland has left and Hazell has been in charge, the company looks a far better bet imo. I have never been impressed by Sutherland, and never will be I am sure.

Net debt has fallen a further £30m on a year ago. The insurance broking arm is now run by Aegis, also remains on track – this has been a multi year lead weight around the company’s neck, now it can hopefully move forward.

Decent bowl on the chart though there are stronger bowls elsewhere imo. The shares rose 4p (2.3%) to a 28 month high.

OnTheBeach, OTB, a regular on here, received a strong broker upgrade on Tuesday:

RBC STARTS ON THE BEACH GROUP WITH 'OUTPERFORM' - PRICE TARGET 340 PENCE

The Right Honourable Justing Greening, non-exec, former Tory MP bought 7483 shares at 265p a week ago – lucky Tories 😊

I note it because there is a huge bowl on the chart and it is attempting to break out and was testing the previous recent high on Thursday:

Filtronic, FTC, posted their trading statement on Wednesday.

You can read the rest where you read your RNS news.

Yet again they are ahead of forecasts, beating on EBITDA by another £400k, there has been multiple beats throughout the year and this adds to those and all the raised guidance over the past 12 months. A year ago, the earnings forecast for this year was 2.6p, so they have basically doubled those forecasts over the year.

The conundrum is why are forecasts showing a drop in sales for 2026 and much lower eps forecasts? They have doubled sales this year. They have also recently doubled they manufacturing capacity and won their biggest ever order from SpaceX. The recent win from SpaceX was worth £24m on its own. They are now diversifying more with contract wins with Leonardo, ESA and Airbus too. My belief is they may start putting the products into payloads (satellites) this year but uncertain timing means they are playing cautious and want to beat and put out upgrades this year too.

I think this company has the scope to do multiples of the current EPS with the satellites communication and defence being top of the pops when it comes to demand and Nato committed to get European defence spend up to 5% over the coming decade. Defence and communications are only just realising how much FTC can do for widening bandwidth and reducing latency imo.

To me, Filtronic feels like one of those potentially great UK tech co’s. unique tech, done right.

Obviously I hold, I am biased and would say that, so don’t go by what I say, do your own research as ever and satisfy yourself this is right for you.

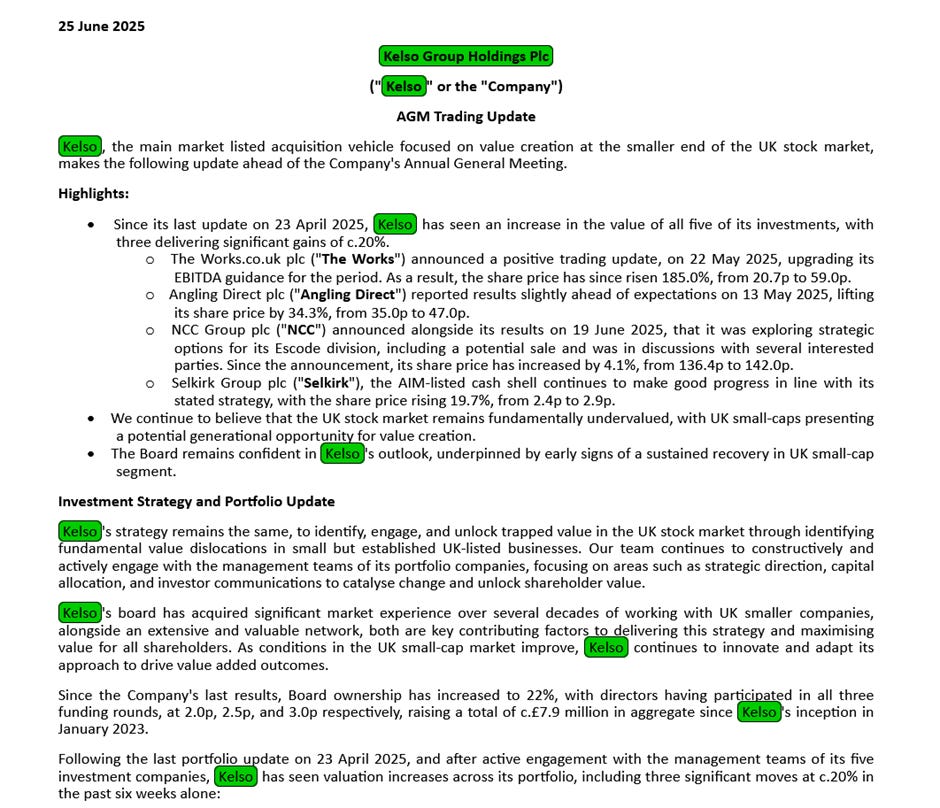

I mentioned in the May 24th Weekend Review that I had bought Kelso, KLSO. On Wednesday they posted their trading update.

You can read the rest where you read your RNS. Kelso is a very narrowly focused investment co with a spread of just 5 stocks currently, The Works WRKS, Angling Direct ANG, NCC, THG and Selkirk SELK. The trading update covers each co performance recently so worth a read. It is potentially a risk into 4 recovery plays and a cash shell. In particular interest to me is what they say re The Works so holders should make sure they read that imo.

The shares have risen over 50% since being covered here. Small and illiquid but it is on the main market rather than Aim.

The full comment regarding the Works (WRKS) from Kelso

Formerly “The Hut Group”, THG put out its trading update on Wednesday.

Two businesses basically but after floating at 650p in Sep 2020, during Covid, it earned notoriety as a pump and dump and accusations the float had been grossly inflated. Much protestations by Matt Moulding the CEO and 5 years later, the market has been proved right. The shares hit 23p recently despite issuing 5% more shares in April at 32.3p. There has been about 25% share dilution since floatation.

In April, after the fundraise, Selkirk made an approach:

“The Proposal ascribed a headline value to Myprotein of £400m - £600m on a cash-free, debt-free basis. The majority of the consideration offered was in the form of newly issued Selkirk shares, and the remainder of the consideration would have been payable in cash from a new equity and debt issuance, which was largely unfunded and without appropriate detail on its source.”

THG sounded sceptical. However, everything has a value and a price and that approach showed these may be significantly undervalued here imo. Added to this, Mike Ashley has acquired 12.6% of the company recently.

I highlighted THG and bought based purely on the bowl on the chart which suggested something positive was happening. Can’t say I love it, can’t say I will hang onto it, it’s likely a trade for me but I’ll keep reading what gets said there.

This is a recovery play but doesn’t meet my normal criteria. There hasn’t been the board changes I require to commit with any passion. It is an interesting situation though with Mike Ashley involved. Probably a ‘watch that bowl’ type of investment or ‘punt’ for me and not something I’d invest the niece’s savings into but perhaps investors with a more racier less risk averse attitude they may find it interesting.

Definitely don’t just follow me blind here and do your own research, I don’t even feel I have done enough research myself, it’s just a bowl that has come good for me.

On Wednesday, Liontrust, LIO posted their full year results:

This is a stock I have followed and held for the yield, which recently hit circa 20%. The question has been, could the co keep paying that 72p divi p.a.. It seemed unlikely, but the co had said it would do so and could do so up until later this year at least. Today we learned that in future they will pay half the earnings in dividends going forward while paying the full 72p divi this year. Based on this years earnings the divi would now be 28.4p, or 7.5%. So for people buying a yield, you can buy as of Weds @ 380p. If you net off the 50p final divi you are buying @ 330p and going forward get an 8.6% yield with the divi netted off, if earnings don’t decline further.

So that’s the question – can they maintain or grow earnings. They haven’t been great at it up until now so the jury is out. Less attractive after the divi cut but still a good yield if maintained.

There’s an old saying that says ‘You can’t buy time’, well actually can.

Time Finance, (TIME), is a finance company providing loans for Assets, Vehicles and Invoice Factoring. Formerly known as 1PM, bringing all subsidiaries under one name. Shortly after in Jan 2021, the Chairman stepped down, then in February, Ed Rimmer took over as CEO, 20 years in finance and Time’s previous COO.

In October 2022, Time announced their “Own-Book Lending Portfolio reaches all-time record high of over £145m”. From this point on, the shares have progressed excellently, rising from 15p, to 65p at the start of this year.

On Thursday they had their trading update:

There’s an old saying that says ‘You can’t buy time’, well actually can.

Time Finance, (TIME), is a finance company providing loans for Assets, Vehicles and Invoice Factoring. Formerly known as 1PM, bringing all subsidiaries under one name. Shortly after in Jan 2021, the Chairman stepped down, then in February, Ed Rimmer took over as CEO, 20 years in finance and Time’s previous COO.

In October 2022, Time announced their “Own-Book Lending Portfolio reaches all-time record high of over £145m”. From this point on, the shares have progressed excellently, rising from 15p, to 65p at the start of this year.

On Thursday they had their trading update:

You can read the rest of the update where you read your RNS News.

Stand outs for me were revenues £37m, this is £2m ahead of consensus according to Sharepad and inline with next years forecasts. PBT of £7.9m is £400k ahead of the £7.5m forecasts. Assuming this tweaks the eps number, they should do something like 6.3p eps I would imagine, placing them on a PE of 10.

There has been no share dilution since 2019.

With PBT margins improved 300 bpt to 21%, PBT up 34%, Lending book at a record £217m.

I like the way things have improved since Rimmer became CEO from 2021 onwards:

Director buying:

Tanya Raynes, Non-Executive Chair of the Company, purchased 10,000 and 1,898 ordinary shares of 10 pence each in the capital of the Company ("Ordinary Shares") at a price of 55.00 pence and 52.675 pence per share respectively.

James Roberts, Chief Financial Officer of the Company, and Tracy Watkinson, a Non-Executive Director of the Company, purchased 9,433 and 18,231 ordinary shares of 10 pence each in the capital of the Company ("Ordinary Shares") at a price of 53.00 pence and 54.85 pence per share respectively.

The CFO now holds 663k. CEO Ed Rimmer has 920k

Stocko has them with £2m net cash, Sharepad says £5m net cash.

Forecasts have risen 20% over the past year:

Looks a decent co with all the metrics going the right way I thought and cheap for the performance, just needs a divi to start being paid.

All just my opinion, do your own research as ever, you know your own risk v reward criteria.

On Thursday, Volex posted their full year results:

You can read the rest of your results where yo read your RNS News.

These result came as a bit of a surprise to me. Over the past year, their shares have slid away where investors were just not interested and this was compounded by the Trump Tariff fears. Anyone who grabbed them at £2 on that tariff fall have had a result, with the shares nearly doubling in 10 weeks.

Underlying eps @ 36.3c, while the forecasts were for 33.2c, so a strong beat. Sales were $30m ahead at to $1086m so the $1113m sales for 2026 looks much more doable and eps forecasts are now below what they have already done this year so their should be a hefty upgrade to eps imo.

Probably the stand out comment in the Outlook was:

“trading in FY2026 to date is very good, creating a strong start to the year and maintaining the momentum seen during FY2025”

I bought a small amount back on the on the news, after they have nearly doubled 😊, based on the outlook statement and upgrades looking likely. Not my best timed purchase but still below where I sold in 2021.

Te webcast on investormeetcompany on Friday was very informative – definite par of your research imo:

https://presentations.investormeetcompany.com/conferences/57c7479cc206/bigroom

The chart leapt north and broke through the August 2024 high:

Likewise (LIKE), the flooring company posted their AGM statement on Friday:

I highlighted these in the May 24th Weekend Review. The trading update looks very good imo. They seem cheap to me and momentum is building. The Chairman bought 500k(£100k) in May. I hold so I would say that – do your own research as always please. A nice bowl on the chart, the shares rallied 10%

A few stocks to watch this week:

Kier Group (KIE), I have held from around 90p. I first highlighted these in the Sept, 2023 Weekend Review at around 82p when I first bought

So cheap, they looked like they might easily double and so they have and more, in fact if you had bought on the Trump liberation day dip 10 eeks ago and caught the bottom then, you have doubled your money in those 10 weeks.

Yesterday, as they continued to soar they were up 6% on 200% normal daily volume by lunchtime. Perhaps something going on and needs to be on the watch list?

Kitwave: KITW – results Tuesday

Currys: CURY – results Thursday:

Watches of Switzerland: WOSG results Thursday

So that’s been my week, much busier than it has been.

Enjoy your weekend, another busy week next week no doubt, now we will be in July.

Rebel

Twitter @rebelHQ

Agree, I was long them late last year. COST is another one

Yes, attractive here and should benefit from the weaker $ imo.

On my watchlist - a buy perhaps when I have some cash spare.

Thanks