The Weekend Rebel Review, June 21, 2025

Never sold in May, didn't go away – thankfully! WRKS, W7L, IGR, FTC, CORD

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

Expect some spelling mistakes – I’m dyslexic and in a rush to get this out on a Friday so a bit of a task at times.

Still a quiet week for news from companies, being June, but the portfolio has been screaming away so I’m happy I never sold in May and went away. Portfolio up 7%+ in the first three days thanks to WRKS, STAF, CAR, FTC in the main, which currently form a large part of my portfolio – I don’t think I’ve had 7%+ in 3 days since the tech boom. WRKS was up 40% on its own.

While the main TV focus was Israel and Iran, most other news of stock moving ability was thin on the ground until Thursday and the BofE rate decision. Even that was as exciting as porridge with rates left on hold.

I thought with less news about, I’d start off with a few words about keeping calm in volatile markets. Last weekend it was all kicking of between Israel and Iran. Issues like this often have a big negative force on stock markets but surprise, surprise, Monday saw the UK open and rise three quarters of a percent in the morning. Was that a surprise though? I am not sure it was. I wasn’t panicking or selling anything on the Friday and most others seemed to be doing minimal selling. I ended the day up. On Monday, small caps were strong, Israel seem to be putting Iran in their place, it’s a boxing match that wouldn’t be allowed under the Queensbury rules because Israel is a much heavier puncher these days and have demonstrated it. Of course this could all escalate and markets could react more negatively. But many shares are very cheap and negativity for share holders is often opportunity for share buyers. Iran may be threatening the if they attacked anything American, they would see colossal reprisals from the US which would likely definitely cause regime change imo. Meanwhile, once again BlusterTrump makes big threats then row back and has now given Iran 2 weeks to come to an agreement. Meanwhile, little Corporal Starmer allows himself to be filmed grovelling at his feet, picking up all the papers the BlusterTrump dropped on the floor – a perfect cameo.

The Drewry Shipping Index fell 7% this week despite fears around what could happen with the Straits of Hormuz with the Israel Iran conflict.

For those as long in the tooth as me, they will remember 911, the first Gulf War, the Financial Crisis, second Gulf War, Bird Flu, Swine Flu, Foot & Mouth, Brexit, Covid, Ukraine and all the other big incidents that have triggered market panic that I have forgot to mention. Each of these incidents had a sharp negative affect on the stock markets. However, if you look back on a long term chart, it is almost impossible to detect those falls from the rest of the chart volatility. If you can keep that in mind you can stay more rational. There may be times to sell out quite a bit but unless you are pretty certain there is a fall coming and you are pretty certain the fall will be meaningful and you can identify it early, then selling out in size is never easy to time and seldom worthwhile. I think in my 25 years as a professional investor, I have sold out in excess of 75% of my portfolio about 6-7 time. Around five were well worthwhile, a couple were a waste of time and cost me. The only great thing about it is you can sleep better, which does have a value. There has been little selling into the Israel/Iran war. It doesn’t feel like any escalation could be meaningful here by way of prolonging this war by Iran. Much of these incidents are just great adverts for US/Israeli weapons technology, it’s too easy to forget the lives that are lost.

There may be days when there’s something that spooks the market and I might be down for the day, but I never take much notice of the daily falls. I prefer to pitch my performance v the FTSE250 and the Small Cap Index. As long as I beat them over the months and years, I know I am going to out-perform those rising charts. Monday was a fabulous day. I’ve been waiting to see the rush into small caps and it feels like it is starting. Aim has fallen for 3.5 years, as has the FTSE Small cap index.

Aim is 42% off it’s high, the Small Cap Index off 8% while the FTSE250 is 12% off the high.

Aim has bounced 25%, the Small Cap Index up 22% while the FTSE250 is up 22%.

From that I see Aim as having lost the most and bouncing the hardest.

Lots of institutional funds, private equity higher net-worth investors fled UK small caps for the US. After the flakiness of Trrump, many want out of the US and they want back into small and mid caps here, and they are driving the price up in great part, in my opinion. After Trump’s tariffs it became clear many overseas investors in the US were going to get hit by the share price and the currency in all likelihood. Switching heavily into small caps 8 weeks ago still feels a good decision.

And this is why it pays to be a contrarian, don’t follow the crowd, do your research and lead the crowd by doing the opposite before all the rest join in. Aim has risen 7% since then, the FTSE250 has only managed half that, and that’s the first time in literally years that small caps have out-performed mid-caps over that time-frame.

FTSE Aim All Share Index (mauve) v FTSE250 (green).

Everything looked perfect then Trump screwed the market for foreign funds who were likely going to lose out of share price falls and the currency. That was a shock and many found themselves too long in the US. Small cap Argentex was a classic where a company took its eye off all the risks and there will have been others that got off lighter but still felt pain. Cash will keep flowing back to the UK in my opinion, for some time. It might be fairly quick to dump larger US positions but trying to build them again in small caps will drive prices up. I’d say to anyone looking to invest in small caps at this point, do your research so you know what you are buying, be confident in what you are buying but remember not to get cocky too – there’s a thin line between having great confidence and being cocky. Strong confidence is great, but cockiness causes errors of judgement. Always have a feet on the ground moment, once a day.

One thing I have noticed recently, lots of days the markets starts weak, then recovers through the day – that is positive and shows investors buying the dip. Starting strong and weakening through the days isn’t good when it happens often imo.

On Friday it was announced that government borrowing was £17.7bn in May, the second highest May on record, and while tax receipts were up £5bn, borrowing was up even more. Oh dear Rachael, your self-imposed rules loo rocky.

On to stocks

Warpaint London, W7L posted their trading update on Tuesday.

Sales in H1 are up 13% while the full year sales according to forecasts on Stocko say this year should be £128m, up 25% for the year. They need to do huge sales in H2 to meet forecasts. Brand Architects acquisition has only had 4 months in H1 so that muddies things somewhat. They say total sales have been impacted by sales in the US, when the US should be their growth driver. They say earnings will be weighted to H2 more than normal – investors often don’t like to hear that, it can be a company hoping to get out of jail with a sales pick up in H2 when they don’t think they will meet forecasts. They do say margins are improved which offsets some of that. All in all the update wasn’t as exciting as the market wanted and the shares came off45p by Tues lunchtime.

I only hold a small amount these days and will likely continue to hold them and see how things play out.

On Friday morning, IG Design, IGR announced CEO Paul Bal was out the door.In my opinion, this guy was dull, poor at communication, over promised and under delivered - out of his depth, and it is a good day for IGR.

I don’t think he bought a single share with his own cash as far as I could see – and there lies a lesson for us investors.

A little bit of Filtronic news from Linkedin:

Double winners:

https://www.linkedin.com/posts/filtronic_filtronic-awardwinning-technologyleadership-activity-7341666791288430593-cY0B/

Highlighted here on my Substack a month ago (May 17th issue), The Works, WRKS has doubled since (that’s what you pay your huge subscription fee for 😊) after a great trading update. This week I did Mello Monday and Vox Markets Live. I covered The Works, on both shows. It has been a very quiet week for company news, but you can’t just make news happen. For those that missed it, as it has been a quiet week, I have posted my full research notes here:

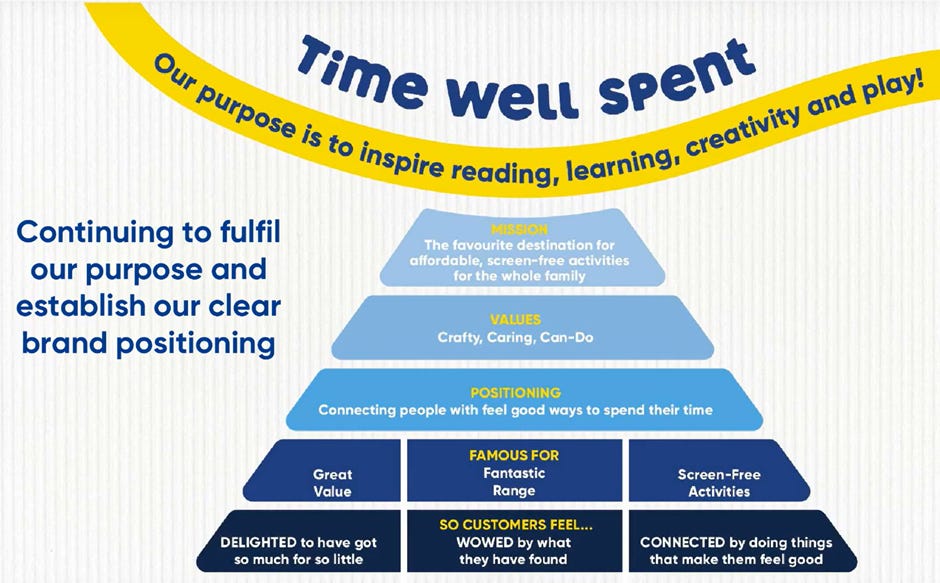

The Works, WRKS, is a retailer of books, games and crafting materials and tools, selling “stuff to do” which doesn’t involve being on a screen – family-oriented things for “time well spent”, inspiring reading, learning, creativity and play. Brought to the stock market by Huddersfield Town Chairman, Dean Hoyle in 2018, The Works floated at 160p, it peaked at 180p, with 9p eps and a 3.6p divi in 2019. After 6 years of hot and cold performance as a listed company, and general disappointment, big city Investors have moved in over the past year.

Graeme Coulthard A Retired Private Equity Partner / Private Investor (and yes, brother of David Coulthard) 7.4%, https://www.linkedin.com/in/graeme-coulthard-b4ab2365/details/experience/

Hudson Management 17%, Private Investor

Mike Burn 5.7%. Private investor

Kelso, active investors, have bought 6.4%.

https://kelsoplc.com/

Kelso took a couple of seats on the board and set up the new strategy. John Goold (ex Zeus Capital) is Kelso Chief Executive and Mark Kirkland is CFO at Kelso. They have since declared” "We joined The Works board on a temporary basis to provide additional guidance as the business underwent a period of change. Since then, significant progress has been made, namely transferring from the Main Market to AIM and strengthening the leadership team. We are content to step down now, knowing that the company is on a path to growth and with full confidence in the management team."

The Chairman of one year is Stephen Bellamy (a former strategic advisor in commercial and financial due diligence and very experienced, having been a director at multiple listed companies). He has recently bought 710k shares (1.2%). His Linkedin ‘about’ says “Chairman, Non-Executive Director and Advisor to public and private companies and to corporate capital providers. Focus on maximising the value of both high growth and turn around companies, mostly in B2B industries. NZer with extensive international experience - 35 years UK, 3 years US.

https://www.linkedin.com/in/stephen-bellamy-a801902/?originalSubdomain=uk

Simon Hathaway, a highly experienced guy in value retail, Commercial Director at 3i’s ‘Action’ retail team for 4 years is now a non exec advisor. He is known for creating Tesco Homeplus virtual store in a Seoul subway - and its partnership with Samsung and now advising The Works. He is head of The Marketing Society and recently bought 100k shares. https://www.marketingsociety.com/simon-hathaway. His Linked in ‘about’ says: A senior retail leader with over 27 years Blue Chip and PE backed retail experience gained in the UK, Europe and Asia. Highly commercial and with a proven track record of delivering outstanding results and transformation. Responsible at Board level for Buying, Marketing, Retail Operations and Multichannel. Now a self-employed Board Advisor, Consultant and NED working across Mainland Europe. An expert in Discount Retail and with a focus on; Strategy, Proposition and Format Development, Sourcing and International Expansion.

A team of astute, experienced city guys having taken near 38% of the company in the past year. Along with Schroders having 20%, that’s 58% of the company and together they now call the shots.

The Works trades from 506 stores of which 98% are trading profitably, all on short leases. Recent trading update raised guidance. Adjusted EBITDA raised to £9.5m, up from £6m last year, making 5.4p eps forecast for year closed. Forecasts are for 6.7p eps this year according to brokers, a PE 6.5. They had £4m cash at year end, up from £1.6m. Stockopedia will say the net debt is £87.8. This is the shop leases of which 98% are profitable. Taking out the leases, the business is net cash. Market Cap £31m @ 54p a share, tiny compared to sales of £227m) are 9 times the market cap after the recent rise to 58p.

H1 highlights:

There’s a lot more H1 performance and company information at https://www.investormeetcompany.com/companies/theworkscouk-plc and a must watch for investors to gauge performance in my opinion

The company has introduced a new strategy – “Time Well Spent”, getting kids off the computer and doing reading, crafting and playing board games on a Saturday night as a family. I think that strikes a chord with many young families. They believe they can grow sales by at least £100m or 35% over the next 5 years. They expect Ebitda margins to grow to in excess of 6%

All of this is being done by improving the brand appeal, increasing brand awareness, improved products and margins, enhancing online with click and collect, and next day delivery, optimising the store estate by killing off the few unprofitable and marginal stores and increasing stores in the best likely locations. Online has always been poor, making up less than 10% of sales. last Christmas they took a hit from their online fulfilment partner who had issues which led to a 12% drop in sales over the festive period. Since then they have changed their fulfilment partner, reversed the performance for online to flat. This is now an area of focus and online sales should now start growing significantly. Anyone who knows the website will have seen a great improvement in speed and presentation in recent months and well worth looking at

https://www.theworks.co.uk/

They have mitigated the minimum wage rises this year and still grown profits by £3.5m, or 60%, and expect to grow profits this year despite a £6.5m Minimum wage and NI headwind. When your profit is £9.5m and you can offset a further £6.5m in costs in the coming year and still be confident of profit growth, you have got earnings momentum. They have moved to Aim to reduce costs.

The new look Works store.

The old style Works store.

In my opinion, these have never made best use of space and they sell stuff often too cheaply, I’m always gobsmacked by just how cheap their stuff is. Most of their books compete there or there abouts with Amazon, but stuff like Jeremy Clarkson’s Diddly Squat hardback is £11 on Amazon, a fiver at The Works.

Billy Connolly’s Tall Tales and Wee Stories, £6.28 on Amazon, £3 at the Works, or get 3 books like this for £7.50 at the Works – nearly the price for the Big Yin’s book on its own at Amazon.

It isn’t just books. 500 piece Jigsaws, £7 at the works

£11+ at Gibsons https://gibsonsgames.co.uk/collections/500-piece-puzzles?srsltid=AfmBOoo_Zx0Qw6Ae_DYxZzj7uGWPAq5nzhzOPAar_YSIDFh8rcntgo6B

There’s some rubbish looking jigsaw on Amazon for£5-6 but anything similar to those on the Works seem to be £9-10.

Art canvasses are much cheaper at the Works than Amazon.

In 2019 they were doing 9p eps, paying a 3p divi and trading at 180p a share. Next year, or possibly even this year, they could get back to something like those numbers based on current guidance being a bit conservative perhaps and the strong momentum in my opinion. The new investors are holding 38%, they won’t be selling their shares in this illiquid company into the market imo, they must have a decent pre-planned exit strategy. Results are on July 22nd.

What are the risks? A retail downturn or a recession, but as they are bargain bucket sellers, if people reduce spend, this may be where they go for a bargain too. Rate rises are not good for retail so higher inflation could be poor for The Works, like most retailers. You have to ask yourself, is the fleet of new large shareholders working for the business? The CEO and CFO take their eye off the ball? Having got themselves into what looks like a great position now, it would be a negative if they then over-promised and under delivered due to lack of focus. I don’t think with all the big investors onboard they would do it or the investors would let them do it personally, but it is always a risk. Currency shocks, hedging mis-management, all manner of things can disrupt earnings for retailers and need to be kept in mind. So far, within a year they have delivered and the stock has double in response. But even after that improved performance and the rise to 58p a share, the PE is just 9. Is this the inflection point where The Work becomes a full-on recovery and push to record earnings, much higher public awareness and one of those retail darlings? I think having seen the difference activist investors have made over the past year and the current valuation, this might be an interesting place to be an investor over the coming years. The city investors all seem to have bought in around circa 35p. With such a small market cap and so many of the shares in the hands of large investors, the shares can be volatile with moves of 5-7% in a day being common, both up and down. Highlighted on my Substack a month ago, just before the recent trading update, the shares have since doubled in response to trading statement, to 58p.

With such huge sales to market cap, any rise in margins should have a disproportionate gain on profits. Small. Illiquid, Aim share. Larger active investor action as a catalyst and a low PE. That’s The Works. The shares hit 3 year highs this week.

I have been in some great consumer and retailer recovery plays, Hornby 10 bagged in 2 years. Churchill China (CHH) fell from £7 to 55p at the turn of the millennium, if you bought at 55p you 40 bagged your money over 20 year and got some tasty divis too. Perhaps the greatest was Next (NXT) – if you had bought these at 10p during the tech boom, rather than many of the techs then you would have 120 bagged your money and you’d now be getting 20 times you original investment each year in dividends plus special divis on top! Sadly, Next was one I missed. One I never missed was Sanderson (SDG) (Walker Greenbank in those days), which went from 6p to 240p in 6 years. I sold in the 80-90p level. More recently, Shoezone (SHOE)went from 35p to 260p from 2020-2023 – even through Covid, I bought at 70p there and trebled my money on my first buys. Even M&S (MKS) has 3 bagged in the past couple of years so it just goes to show how big and how wide the retail/consumer recovery plays can see huge and prolongs share-price rises. You can’t buy a retail 10 bagger if you don’t have a holding early into the recovery and start compounding early imo. Will the WRKS, with all board and investor changes be another? Your mind is like a parachute, only useful if it is open.

New strategy and appeal:

Remember you need to satisfy yourself that any share you buy is right for your risk/reward profile. These are a small cap, dreadfully illiquid at times and difficult to sell when the market turns bearish. I could be completely wrong about what I have deduced or a liar, a complete idiot – you will never know unless you verify what I have said with your own research, that is important. You press your own buy and sell buttons. Please remember any action you take is your own action.

So that has been this week, pretty uneventful for news but great for holdings. One share that I have looked at before and caught my eye again was Cordiant Digital Infrastructure, CORD, who had pretty decent results out. A main market share, £750m mkt cap so FTSE250 size but unclassified. Stockopedia Summary says this:

Cordiant Digital Infrastructure Limited is an externally managed closed-ended investment company. The Company's principal activity is investing in cloud and data centers, telecommunications towers, distributed sensor networks, and fiber-optic networks. It owns and operates digital infrastructure assets in the United Kingdom, the European Economic Area, and North America. The Company’s investment objective is to generate total returns (on a risk-adjusted basis) for shareholders over the long term, comprising capital growth and a progressive dividend through investment in digital infrastructure assets. Its diversified portfolio includes digital broadcast infrastructure, mobile towers, backbone fiber-optic networks, data centers and cloud systems, and Internet of Things/Smart City solutions. The Company follows a Buy, Build, and Grow model. It seeks to generate total returns of approximately 9% per annum over the longer term. The Company’s investment manager is Cordiant Capital Inc.

Not my type of share really but I would think these could be decent beneficiaries of all the data centre builds if you wanted exposure perhaps. A nice bowl too.

Perhaps worth a bit of research but look at the rise in debt and shares in the past 3 years – probably used to invest with but might clip gains from growth a bit. Interesting sector and chart though imo. Killik put out a Buy Rec on Thursday which caught my eye too. A PE of 6.5 ad a 4%+ yield. The shares rose 3% on 750% normal daily volume.

Next week’s results and trading updates to watch out for:

Tues 24th G4M final results

Weds 25th PROC final results

Weds 25th BAB final results

Weds 25th LIO final results

Thur 26th MSI final results

Thur 26th MOON final results

Thur 26th VLX final results

Have a great factor 50 weekend - the results and updates pick up pace from here.

Rebel

Twitter: (X) @rebelHQ

yes, I think having some retail experts onboard now, is making the difference.

Thank you for another insightful and useful weekly update, much appreciated.