The Weekend Rebel Review Jan 18th, 2025

FTC, CARD, GAW, GYM, BOOM, MPAC, IGR, MCB, SMT

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

Well at last Rachael Reeves had some good news this week, the cold spell of weather is over – oh, and inflation came in a smidge under expectations, that’s expectations that were 30% above where they came into office 6 months ago. Starmer thinks we re going to be the AI leaders in the world, well I saw this this week.

This is a chart of country energy prices

At $26 compared to $6 in the US. British business is paying 4 times what they pay in the USA. How do AI companies or any companies for that matter compete with any co’s in these other countries when UK electricity is so much more expensive? And as the £ falls v the $, things get even worse for us.

At last a slightly weaker inflation number helps Reeves out but it’s only buying a little time, the Grim Reaper has his block of carborundum out and he is sharpening his sythe on a daily basis.

After the first two days this week being pretty flat, the inflation number coming in below expectations set the market galloping with a 550 point rally on the FTSE250. You really never see these things coming but I do think if the market can sustain a bit of positivity there will be some dramatic moves on some of these UK shares that are trading on such low ratings. In my experience, when you get positive news like this that surprises the market it’s the mid to large caps that react strongest first then the small caps pick up. And as the trading updates come out, there are few missing forecasts but lots inline or ahead and seeing decent reactions to the share price.

As if good news was like busses, the GDP data came in for November and showed the UK had grown 0.1% in November. That’s good news in that it wasn’t negative, the bad news is the market expected 0.2% growth. Jonathan Reynolds, the ‘Business Secretart’ (don’t laugh!) called it great news as inflation had fallen and growth was up, but then his experience is that of a solicitor, just like the Chief Secretary to the Treasury Darren Jones, in fact I’ve looked through the whole cabinet and they are nearly all career politicians with no business experience, lots of lawyers and right out of Uni into politics types, so little wonder. Maggie Thatcher’s father ran a corner shop, she knew about keeping costs down and profits up from a young age – and that is the difference. Economic literacy should be on every school curriculum, how many kids leave school understanding the power of compounding, ISA’s, dividends etc, even how shares work? I mentioned to mate the other day about M&S shares he actually had in his SIPP. “Who owns M&S?” he asked me! “You do you bloody idiot!” Honestly, guys that have gone through life with pensions and paid money in without understanding the concept of share ownership. Kids need teaching all the things that through life can make a huge difference to your wealth or poverty, then we might actually get people in public life with half a financial brain.

Anyway, a two day rally in the market of circa 750 points on the FTSE250 worth over 3.5% is not to be sniffed at when it has been so bad. It is a stock pickers market, if you can find winners you can make money, punt tips and buy indexes and I think you might struggle – research really does maker you feel comfortable and less jumpy.

Low and behold too, the FTSE100 broke out to a new high on Friday. So life isn’t quite at an end for UK shares – the biggest riser in Europe.

On to stocks:

After mentioning Filtronic, FTC, last weekend and the chart firming, the co duly obliged and posted a nice trading update on Monday saying they were ahead of forecasts. Brokers have upped forecasts to 4.8p eps this year and 3p eps in 2026. That’s 1p hike this year and a small 0.1p move up for next year.

On a PE of 20 seems cheap to me.

FTC eps record over the past 2 years show over 100% eps growth per annum:

2023 =0.22p 2024=1.41p 2025= 4.8p

Working on a pre-tax basis the pbt has gone from £1.5m in 2022 to £3m in 2024 to £8.35m forecast this year and we haven’t had H1 results yet.

They had net cash of £5.3m at year and generated £6.3m cash from operating activities:

The 3p eps for the coming year is lower but FTC tend to guide very cautiously then beat as they have done over the past two years as they raise forecasts through the year. They have used up tax credits which have flattered eps so far but they have also expanded their factory at Durham and opened an excellence centre at Cambridge Science Park – both these moves are a signal of intent, they have a long term deal with Musk’s SpaceX and more and more satellite stuff is being done which is far higher margin and will boost earnings as we go through the year from some of these large contracts.

The bowly chart has broken out to a 19 year high.

Space is to the fore with Jeff Bezos of Amazon launching the first of his Blue Origin rockets, New Glen to go into space and deploy satellites too.

I’m pleased to have bought back in at a smidge above where I sold in September. Interim results are in February and I’m sure they have kept some powder dry for then.

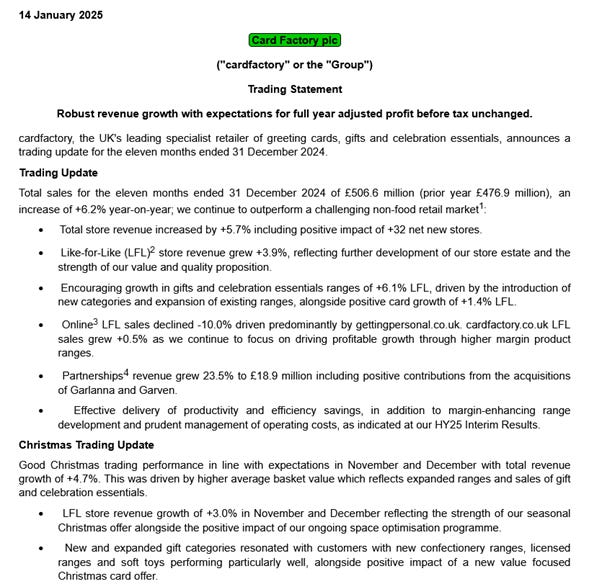

Cardfactory, CARD, one of my OBIAY Naps for 2025 delivered their trading update on Tuesday and what an update:

This was a cracking statement. CARD had basically fallen back from 143p to 90p through punters panicking when the H1 results were far lower than the punters were expecting. But they obviously hadn’t been paying attention in that case as CARD had clearly flagged they would have much higher costs in H1 due to heavy investment for H2 this year and the higher minimum wage, but expected a much stronger H2 to make up the H1 shortfall and more. To underline that they reinstated the interim divi at 1.2p. CARD invest a lot in H1 and get the sales in H2 with Christmas, Valentines and Easter etc. The big clue was in current assets that were up £7m on the previous year, about £20-£30m in retail value, likely stock imo. Of course those not paying attention panicked, thinking it was all from the cost of the rise in the living wage, which it was in part, but the co was confident of out-running those cost and seeing a huge H2. And so they proved with this trading update.

Forecasts are for them to do 14.4p eps and pay a 5p divi for the year, that was a PE of 6.3 and a 5.5% yield on the morning of the trading update.

More fantastic still, they say they are confident of absorbing Reeves’ NI raise and rise in the minimum wage at a total of £14m and still grow earnings at mid to high single digit growth this year. That is stunning for a retailer full stop, let alone in this climate. That would be another 20% on earnings this year were it not for those costs too. Earnings have grown 8 fold since 2022, a divi has been reintroduced and earnings and divi are still set to grow. I dare say punters can’t believe it again – I’ve seen in the past how fast these can rise when the company causes punters to wake up.

The exciting bit is that overseas sales via partners is up 26%. This year they will have a full performance from Garven in the US who distribute wrapping and bags to Christmas retail. CARD can put their cards straight through Garven (who don’t distribute cards it seems) into the US and cards are high margin for Cardfactory. They will also have a full year of ALDI selling via 1200 stores rather than 600 in the UK and have exclusivity. There is also the Irish acquisition of Garlanna and they also have signed a wholesale agreement in the US with someone they are keeping close to their chest. All these to fully kick in, all acquired from their own cash and debt so no dilution. The contract with Reject Shop in Australia is set to be continued and improved and signed off any time. Partnerships revenue grew 23.5% to £18.9 million including positive contributions from the acquisitions of Garlanna and Garven, H2 up nearly 200% from £6.6m in H1. The US card and celebrations market is huge.

A comment I have heard is “UK retailers usually struggle in the US”, I’d agree with that. But CARD are not going there to retail, they are going there to wholesale and distribute, it’s a huge market and volume reduces costs.

That is the great thing with CARD, they throw off so much cash, they can use it to buy businesses and there is no share dilution so all the earnings go straight to the bottom line.

CARD are now doing way over two thirds of the 18p eps earnings they were doing in 2018 and look like they have £150m less net debt since then. Back then they were trading at £4 a share, there has been next to no share dilution and set to grow at pace in the US and overseas. Here is the chart:

Punters are running scared of all retail but few have shown this confidence or cashflow and growth. I like buying when I believe punters are unjustifiably scared and uninformed. I added more the day before the results and results day so these are a big holding again for me now. All along I have said Darcy is a top retailer. When the punters were panicking there was nothing I could do but sell and wait for the panic to calm, then buy back at the lows. I only had these down as an ‘OBIAY potential’ in my year end review but after seeing this update it’s a full blown OBIAY in my book now.

One other thing, on top of the current yield of over 5.3% at 95 a share in price, there’s 6% for the coming year. They were questioned about returns to shareholders at the last presentation and said they kept it in mind. They have a record of paying special divis on top of their normal divi:

In May, CARD will pay a final divi of circa 3.8p. In the year ahead they will pay 5.6p on forecasts. I will get 9.4p back in 15 months in divis while I wait for these to one bag – and I may get a special divi on top.

It’s on a PE of 6.25 when the shares are £1. Bonkers cheap in my opinion and currently misunderstood as to how solid they are. To have £14m costs lumped on you from NI and still say you’ll meet forecasts of near 10% earnings growth speaks volumes.

https://www.cityam.com/card-factory-shares-should-rise-rapidly-after-successful-christmas/

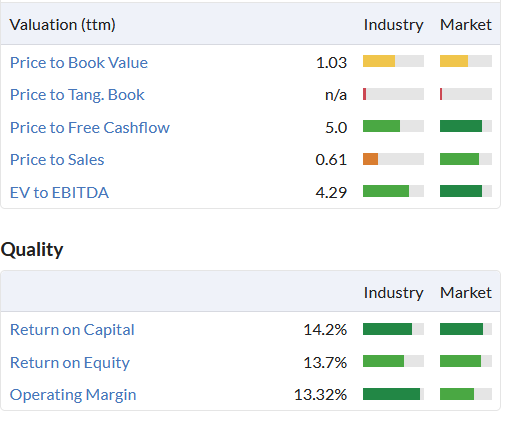

If you want to ignore the PE have a look the price to free cashflow on Stocko which works on the trailing 12 months – it will be even better this full year.

The one fly in the ointment was the online which was weak. I have said all along I am not bothered by that. If you can run a retail outfit and do so much better than Moonpig then why bother? To an extent you have to be cannibalising your retail sales if you increase online. There’s lots of costs online as Moonpig have found out. I’m sure CARD could increase online performance faster if they really wanted to but that means getting into stuff you aren’t so good at to the detriment of doing stuff that you are really good at. I’d sooner they push that when they’ve run out of options for physical sales and just have it there annoying Moonpig for now. Overseas expansion will be far more beneficial.

Scared markets create great individual bargains imo. As a footnote the CEO and CFO were buying shares at 108p last month. This potential OBIAY is being grossly underestimated when it can easily out run a £14m hit from Reeves and still grow earnings strongly. Those hits won’t happen the following years but the growth should still be rattling on imo.

As a comparison, Moonpig is on a PE of 13.2p for this year – more than double CARD. Moonpig don’t pay a divi, CARD pays 5.3%. Moonpig earnings growth negligible and adjusted if they have any.

Here’s Moonpig’s data to compare with CARD above:

I think there’s some in the market that are a bit obsessed with online. Moonpig have been trying for ages. This might be the cause of some of the weakness in the shareprice but not for me when these do so much better in physical stores than MOON can do online.

One last thing, if you want to read how good Darcy is as a retailer, read this article of how he saved Costcutters – this isn’t your average retailer and he has some great experience. It’s what gave me faith in him when he came to CARD.

In the 2022 financial plan Darcy said he was “Confident in the longer-term growth opportunity for the business targeting revenues in excess of £600m in FY26” They had sales of £364m back then. If you look now, they look like they are going to hit his £600m next year as he promised, or at least come very close.

The question I have to ask myself is, do I want to invest into the worlds fastest growing, largest card producer in the world, on a PE of 6 and a yield of 6% while the market is fast asleep to the growth?

Edison have a note out with 200p target based on a discounted cashflow model: https://www.edisongroup.com/research/delivering-fy25-expectations/BM-1027/

As ever, of course I’m saying all of this, I hold lots, I’m biased and not objective at all so do your own research and make your own decision, it’s your money.

Games Workshop posted their interims on Tuesday, a record H1 profit.

With cash of £126m they seem to be on a PE of 27 by forecasts and look like they may be ahead, having done nearly 60% of the years forecast eps in H1. With the deal with Amazon yet to be fully spelled out these do not look expensive imo. The shares came off a few percent but that’s the market and as a good company they did mention the potential tariffs as they should do – but who is surprised by that?

I think that looks a decent report and with a 185p interim divi it’s hard not to like these for the value and what Amazon could lead to imo.

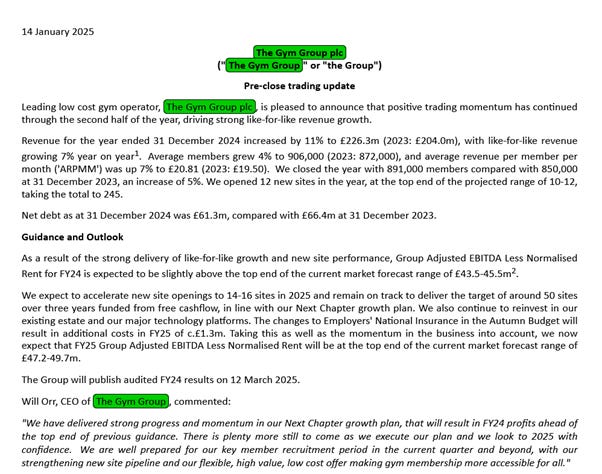

The Gym Group, GYM, featured here a couple of months ago, posted their trading update on Tuesday.

Results to be slightly above the top end they say. These have very good cashflow and a price to free cashflow of 4.1, which is attractive imo. They have a good model with round the clock trading and pay per day which the punters seem to like. The market is throwing up some big bargains now so I don’t know how long I will keep the remainder of my shares. Certainly looks a good chart especially after giving a bit back but can I find better stocks around in this oversold market is the only question?

Audioboom, BOOM.

Audioboom, the podcast infrastructure and enabler posted their January trading update on Wednesday:

A few highlights I would point out: They “ended 2024 as the 4th largest podcast publisher in the US on the Triton Digital ranker, as well as 4th in Australia, 3rd in Canada, 2nd in New Zealand and 7th in Latin America - highlighting the platform's global scale”. That is clearly a strong demand for their product.

I don’t understand all the various individual parts of Audioboom, it’s a simple business, it’s basically like a commercial radio station. Audioboom provide the infrastructure like a radio station would, and then they provide and acquire the content to attract an audience and sell space to advertisers – while the public listen to it – simples.

After entering into a number of contracts with minimum guarantees during Covid, which cost them dearly, they are coming to an end. They have a $3m reduction in their annual minimum guarantee obligations starting this Q1 which will save them money going forward as these drop out as others have started doing and will do too.

“The Company anticipates record revenue and record adjusted EBITDA profit in 2025”

The previous record EBITDA was in 2021 when they did $3.1m EBITDA which translated then into 41c EPS. They have said they will do $3.4m EBITDA this year, beating the previous record by 10%. There is now just 16m shares in circulation, in 2021 there was 17m On that basis, the current EPS forecasts of 14c this year and 18c next year look nothing like aggressive imo.

In 2021 when they did those record earnings and EBITDA the shares were trading at £22.50 or circa £24 taking into account fewer shares. I’m not saying they should be that high today but they clearly are currently on a strong growth path and trading @ £4 here is less than 20% of where they were at the previous high:

Very illiquid which means the shares can move about a bit at times but that can help you buy more cheaply at times. I was very pleased with the update and the potential looks good imo. Obviously I hold and I have them in my Naps for this year so I would say that so do your own research and feel comfortable in what you hold.

These have raised guidance 4 times since October, adjusted EBITDA raised from $1.3m to $3.4m. a near trebling. 18c eps is the forecast for the coming year, seeing they say this year will be a record year and they did 41c in in 2021 it makes me think there may be a lot more upgrades this year. The company presentation for the trading update can be found here.

Audioboom investormeetcompany presentation:

https://www.investormeetcompany.com/meetings/2024-review

Well worth watching – the graphics show just what a high placing BOOM have in the industry. It’s also interesting that they are looking at a Nasdaq listing once sales are over $100m.

Mpac, MPAC, posted their year end trading update on Thursday:

There’s a further upbeat view from the CEO Adam Holland which you can read where you read your RNS but it does say “We are pleased with full year 2024 financial performance, which is in line with market expectations. 2024 has proved to be a transformational year for the Group

This company is in a great sector, providing automated production lines. At the moment businesses are looking to save moreover they can and a ptiime way is to reduce staff and automate. There’s also onshoring going on and businesses are abandoning the likes of China and cheap wages in order to improve their ESG AND reliability of delivery. Staff in the UK cost far to much to be competitive but a robotic or automated like needs no wages nor time to stop and eat, doesn’t go off sick, doesn’t need a pension and doesn’t complain.

Interestingly they look to have done circa 20p+ eps in H2 by my rough calculations with only 3 months contributions from the two acquisitions which leads me to think current forecasts are cautious.

MPAC has made 3 acquisitions recently, CSI Palletising which does automated pallet wrapping (something CARD has stared using recently to reduce costs). Boston Conveyor & Automation is a company that does automated conveyor belts for Food, Life Science and Industry. The third is SIGA – a UK-based provider of machine vision solutions to the food, beverage and healthcare.

All these three businesses add to what MPAC can do and create big synergies and cross selling opportunities and diversifies their customer base. That trading update looked very good to me, along with the outlook for next year as it’s the coming year when the acquisitions will kick in.

VOX interviewed the CEO and CFO and it’s well worth watching:

They expect to generate £12m of cash this year and rapidly deleverage the current debt level.

The shares rallied 37p, circa 7% on results day. The chart has a gloriously large bowl:

Equity Developments put out a note on Thursday with a 865p target – if you want to read it:

https://www.voxmarkets.co.uk/media/67890471d38088bfb29321dd/

Isn’t life just fun? Friday and after what has been a good week it was all wrecked by IG Design, IGR. They put out a trading update that was shockingly bad due to troubles with DG Americas. This week, the 4th largest customer of DG Americas division has re-entered Chapter 11 protection initiating a prevision of $15m to be made by IGR and they will now only break even. This is dreadful management. They had a presentation on PI World at the end of November where the CFO explained why he was so confident about hitting the numbers and he was massively confident.

Well that is life as an investor but you do expect when you watch a presentation from a company that is so confident, they can deliver at least 6 weeks down the line. So I have taken a big wallop today, Friday. IGR were 4% of my holdings. Sadly, no matter how much research you do, even to the point of watching the board being quizzed 6 weeks ago and being extremely confident of meeting forecast, things like this still seem to happen. Anyway, will dust myself off, move on and make it up somehow after they have wiped out nearly everything I have made this week.

Do research, hold a basket of shares, never hold that much of one share that it can do more damage than you can handle and know what your risk level is and stay diversified. Just as important, never let one stock that lets you down, damage your confidence – that just makes you make poor decisions. I try to blot it out, stay cool and move on with determination to make it up elsewhere as swift as I can. Big reward requires a certain amount of risk, you just need to make sure that over all, reward outweighs risk by a long way and you get far more big winners than losers. I had WOSG January last year give me a wallop of 3% off my portfolio but still closed the year up over 30% so you have to keep everything rational and in perspective. Lack of director buying was an indicator I shouldn’t have ignored. I took a 2% hit and sold. The issue is they will likely warn again, who wants to go into the results holding these now when they halve on a warning? I’ll never touch these again unless the management changes, this lot aren’t up to the job imo. Was only a ‘potential OBIAY’ in my Naps purely because of their historic performance. Making mistakes is fine if you learn from them, I seem to be always learning!

Took what was left of my battered IGR cash after selling and stuck it in McBride, MCB on their trading update which looked very good and a company I know well. They make cleaning products and the like for supermarkets own label or white label:

With net debt falling, a PE of 5.23 falling to 5 and a reinstatement of the divi this year, directors buying and having been continuous buyers, it looks a nice place to recover my IGR losses. No time to do a full write up today but perhaps next weekend. They have some great valuation and quality stats: No mention of hat the divi will be reinstated at but they used to pay 5p divi on 13p. This year forecast to do 19p eps +.

Highlight in the RNS “contract manufacturing volumes increased by 69.0%, driven mostly by the successful launch of two new multi-year contracts with large FMCG clients over the past six months.”

Interims on Feb 25th

In brief

This week I have traded VTY, CURY, TST and GFRD for decent trades that have been hard to achieve recently, among others. Also bought and buying a few other long termer stuff that are potential holds after I see the results, will update those next weekend.

A bowl to watch – Scottish Mortgage Trust, SMT

Thanks to all those that have shown their appreciation for the hard work that goes into doing this every week, by donating to my Village Hall Refurb fund, it’s very nice of you and will all help what is going to be a long slog.

Remember these are just my opinions and thoughts, I am not making tips, I’m no analyst, I’m just pointing out what I have been doing reading, buying and selling. Please do your research, I could be totally wrong.

Have a great weekend

Rebel.

Twitter: @rebelHQ

It happens to us all now and again. On a warning I try to mentally set a price in my head where I think the stock could go, before the open, a pretty aggressive estimate always. I might then sell in tranches in order not to sell at the low.

If 3% of your portfolio halves you are down 1.5%. I try to take it on the chin. If you lost 1.5% over a few months it would likely not bother you half as much, it is because its sudden and it makes you question yourself.

Try to blot it out fast and carry on like it hasn't happened and make sure no position is too large to do lasting damage imo.

Cheers, yes, there is that and agree it is a genuine cost. Actually Stocko work on trailing 12 months so it isn't as accurate when CARD have a lot of cash coming in in H2.

On a trailing 3 years Sharepad has 8.6. I think with the cash likely to come in this H2 the number loweres for both Stocko and Sharepad.

I am not so keen to add the leases as debt to be honest. I am no accountant but if you are going to add say £100m in leases to net debt, those forward leases have a value that needs to be taken into account too and I'm not sure they fully are, but I may be wrong.

With free cashflow I like to look at what a business is doing. Are they acquiring, paying down debt or paying divis or better still doing the lot. CARD are doing all three.

Meanwhile net cashflow has gone from negative £23m in 2023 to roughly £1m net cashflow this year according to Edison while Panmure are forecasting £26m free cashflow this year.

So yes, how it is calculated is subject to variation but I like to see actual stuff being done with the cash because it makes me believe the company has confidence in it being sustainable imo.

Thanks for pointing that out.