The Weekend Rebel Review, 13th July 2024.

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.Well that’s the election over at last but really it’s just the start.

Tennis, Football, Masterchef the Professionals -it’s a real sportfest at the moment 😊

Rather like the England chant, when it comes to manufacturing, for a lot of UK companies, ‘it’s coming home’, in the shape of re-shoring imo.

You can invest in an index or a fund and get a certain amount of gain but I prefer to compete at finding winners in the market myself, something that seems to get easier and easier on the valuations here in the UK. It seems to me this week has seen a bit of profit taking from pensions after the election. I suspect fears over Labour taxing the 25% tax-free lump sum is on the minds of some investors and they are whipping a bit out perhaps. There’s bound to be some changes in taxation on business, industry and investments that we will likely not have guessed and these will obviously affect different businesses in different ways. Remember Gordon Brown making the BofE independent as his first move when becoming chancellor? I think Reeves will try to cuddle up to the City and investors and she’ll likely try a few stunts to please the market and get a positive reaction from her first budget so let’s see. Obviously construction, house building, green energy all come to mind. Looks like they are planning a return of PFI too which will stimulate construction in all likelihood and leave the true cost down the line. Lot’s of this continues the uncertainty for a while so I’m continuing to look for genuine undervalued stock and ignoring the noise as it has always worked well for me. I should also add it seems to have worked well for Richard Staveley at Rockwood Strategic recently – he was in early on FTC and FCH and I think he is up 27% year to date he was saying on Vox – few funds doing that well.

I ran through the positives and negatives I saw from a new Labour government last week and the sectors I’d be looking at and avoiding. Not being into resources anyway it isn’t a place I even consider investing in so never bothered mentioning it. I would say though that this week’s news that Ed Milliband has ordered an end to any more drilling and exploration in the North Sea immediately, went beyond what I even thought they may do. I had to search aout to make sure it wasn’t some AI scam. What that means for the sector I just don’t know but it isn’t good. I just hope Labour have plans to find another 200k jobs from somewhere to replace those that could be wiped out, mostly in Scotland. Meanwhile we will now be shipping in even more energy from abroad which will cost more due to shipping and will increase the carbon we use as a nation with the carbon used to ship it here. Absolute bonkers – but that well known economist Gary Linekar thinks it’s a brilliant idea so what do I know?

Market notables this week were a bit thin on the ground but GDP up 0.4% in May double the 0.2% expected, was a big positive. You can see the pick up on the chart visibly now. We haven’t had growth like this for 2 years. The big question – what was Sunak thinking calling an election so early? Here’s the GDP chart – highest in 2 years tho not a growthfest.

Services has been the stand out over the past Q

Strangely, my focus this week has been the east rather than the west and while the US has been ploughing ahead, China and Hong Kong are starting to firm after a strong Friday – Hong Kong and China breaking above short term resistance:

Meanwhile the FTSE All-World index goes from strength to strength which makes me feel that internationally involved companies here should do better than domestic in general.

While it may not feel like it, the FTSE250 broke out through the recent resistance this week to make a 2 year + high.

The FTSE Small Cap has done the same so there are some positive takes to this market even if you don’t feel it every day, so remember the Ian Dury song – Reasons to be cheerful…..

This is the first week in a while where shipping costs have stayed pretty flat in a while..

So onto stocks and with July here I have been waiting to see results and news start to move this market. So after a quiet Monday, like all Mondays these days in the market, Tuesday opened with interesting news from Capita, CPI – another Richard Staveley Rockwood Strategic stable horse.

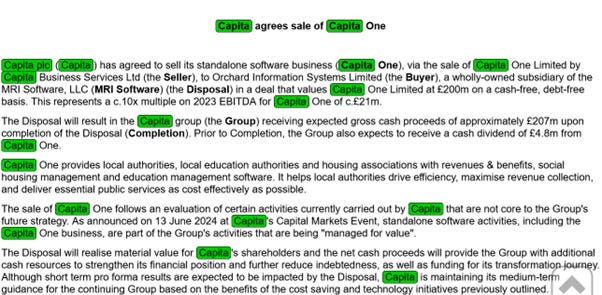

I saw these moving up on Monday but ignored them unfortunately, even though I had listened to what Staveley had said, it looked like punters just driving the price. On Tuesday they announced they had disposed of part of the company:

It still has to go through and meet certain terms but it looks pretty straight forward .

On this basis they lose a small bit of profit, about £21m of EBITDA for £200m+ which will reduce their debt a lot. The business looks far more attractive on that basis and the shares roared up from 15p to 19p. Interestingly, Staveley was saying only just last week on Vox that he believes the business is worth more than double it’s valuation as there are several disposals like this they can make that would be enhancing to the value of the company. This web interview is worth watching, Capita is the first one up, it also includes Filtronic and Funding Circle further in:

Capita has a pretty recent change to CEO and CFO which I like to see, the new CEO bought 650k shares in March and a non exec buying a decent amount too.. They have also done a deal which means they stop paying into the pension over the next year. Staveley also mentions that the debt figure includes a lot of leases that the new CEO plans to sell off a number of – so the debt is less worrisome than many may have thought. All in all with the disposal, Staveley buying recently, new CEO and CFO, the positive chart move and finally worthwhile action on disposals and pension all say to me this is an interesting stock and I’ve been buying a position that I’ll likely increases going forward if everything goes well. There is also just 12% dilution over the past 5 years – a 5 year chart below.

The June 15th trading update carried a link to a webcast – I watched it and couldn’t help thinking how similar this was to RR. and Turbo Tufan’s presentation, down to the new CEO bringing his female sidekick with him to the company. Worth watching:

https://webcast.openbriefing.com/capita-cmd24/.

Interestingly, after the disposal their doesn’t seem to be earnings downgrades. Currently, the forecasts are for 2.95p eps this year and 3.96p for 2025. There has only been circa10% dilution from 2018 where they were achieving 22.5p eps so around 20p eps with that dilution. 3.96p eps next year would be a PE of 5.2. I like recovery plays where you can see huge previous earnings and little dilution, it sort of lets you feel where the shares could go based on historic performance, if they can regain previous margins imo. I now have a 5%+ holding. In what looks like could be an OBIAY imo, but I would say that so do your own research.

Wednesday’s highlight for me was MPAC, amid much mediocrity in the market. Their regular July was thumpingly good, not that the market reaction reflected that:

Typically a number of punters banked profits but I think they will regret it.

Firstly sales are up nearly 16% in H1 compared to just under 5% sales growth forecast for the year. That’s an £8.2m increase in sales over H1 last year. The current forecast was for £6m sales growth for the whole year! So if H2 was flat, they would still beat forecasts by £2m. H2 won’t be flat though, in my opinion, the company and its brokers like to guide low and beat. When companies say earnings will be H2 weighted, that often spooks punters into selling too. But a simple look back at MPAC results show you this is always the case.

Last year was 6.5p eps in H1, 19.7p eps H2.

Watching Adam Holland on their post results presentation, he said they were targeting 10% sales growth and 10% margin growth per annum.

Panmure-Liberum said this:

“Sales growth of 16% combined with improving margin to drive a near doubling year on year in forecast H1 adjusted EBIT.”

If I crudely double H1 eps so then that’s 13p eps coming for H1. With better margins as they say, I’ll be amazed if they don’t beat the 38.7p eps forecasts by some way for this year. Just meeting forecasts would be 60% eps growth on top of nearly doubling earning last year. 60% eps growth on a PE of 13.5, just on the basic lowly guided forecast gives a PEG of 0.22. The order book for the year ahead was flat but that’s not an issue for me, MPAC have always said they have a very lumpy order book so just one order could bump that up 10% in a day.

This adds nothing into the forecasts of what might become of the Freyr battery production line that has nothing priced in, or a deal to end pension contributions going forward.

I increased my holding on Wednesday’s pull back, I believe these will have their big day before too long. Obviously do your own research.

Jet2 posted rather decent results on Thursday, beating forecasts by some way at 185p eps making a PE of sub 7. Considering how much net cash they have they do look cheap and the chart is starting to make a decent bowl at the time of the results. I don’t want to add another holding but I’d thought I’d highlight it. Strong rises across the board on the numbers in the results imo.

Coming up over the next week which I will be looking out for:

Monday 15 July

ME Group International PLC Half Year Results

Tuesday 16 July

Bloomsbury Publishing PLC Trading Statement

Brickability Group PLC Full Year Results

Intermediate Capital Group PLC Trading Statement

McBride PLC Trading Statement

RM PLC Half Year Results

Sosandar PLC Full Year Results

Wednesday 17 July

Renold PLC Full Year Results

Thursday 18 July

AJ Bell PLC Q3 Results

Creightons PLC Full Year Results

Dunelm Group PLC Trading Statement

Kier Group PLC Q3 Results

Qinetiq Group PLC Trading Statement

Friday 19 July

Hargreaves Lansdown PLC Trading Statement

That’s my week, I hope it’s a little bit interesting. Obviously do your own research as I am biased, I hold these stocks (not Jet2) and I am talking up my own shares. I’m no an analyst, just a private investor.

Have a good weekend!

Rebel

Thanks.

I use Sharepad for charting.

I agree