The Gym Club,

GYM, No Pain, Plenty of Gain?

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

The Gym group, GYM is a stock I have watched for some time. A fascinating part of it is the fact that at first glance you wouldn’t be turned on by the PE valuation, which is what most investors look to first but as Miranda would say – “bear with, bear with”.

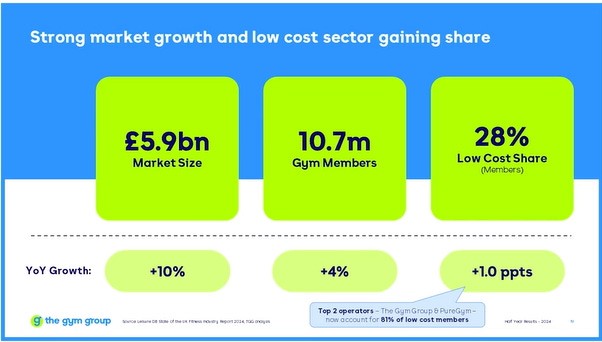

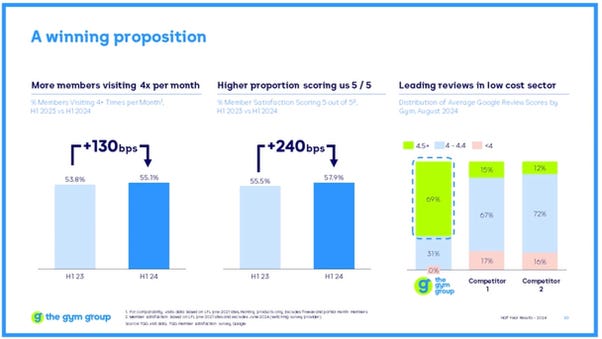

The Gym Group is a chain of low-cost, affordable personal gyms in the UK with stripped back models that have no steam rooms, saunas or swimming pools while providing top equipment levels. They are very popular, scoring 4.5 on Google satisfaction reviews, much higher than their nearest competitor. Largest competitor is Pure Gym with roughly double the number of gyms compared to The Gym Group, while Pure Gym have around 1.6m members compared to GYM’s 905k. As the second largest affordable gym co, Gym Group offers 24-hour access to gyms across the UK without a contract while much of the market require £50-60 monthly membership. Other competitors are David Lloyd Leisure, Energie Fitness, Hussle, John Reid Fitness and Fitness First, JD Gym, Bannatyne Heath Club, Virgin Active among many more. Total UK gym membership is rising and the increase in membership numbers means that 15.9% of the UK population is now a member of a gym. This figure is up from 15.1% in 2023. The global health and fitness club market size was valued at $104.05 billion in 2022 and is projected to grow to $202.78 billion by 2030, a compound annual growth rate of 8.83%. The market size of the Gyms & Fitness Centres in the UK has grown 2.5% per year on average between 2018 and 2023.

GYM floated in November 2015 @ 195p a share. There has been 30% share dilution in that time. They are fully listed and NOT Aim as many assume. Here’s the long term chart:

I was attracted firstly by the change in the chart which became clear around March. Changes in charts are great indicators in my opinion but the change needs to be significant. You can see on the chart above that at 2017-18 the chart curved up but since 2019 the chart has been a sequence of up and down spikes both large and small over the years, short-term ones and very volatile. Since April 23 the chart has made a clear curve up that is different to the previous chart history. This coincided with Richard Darwin, CEO stepping down. Was Richard Darwin the problem that the market wasn’t happy with? The line shows you Richard Darwin’s term in office. I don’t know but it is interesting. John Treharne, the Gym Club founder, became executive chairman during the hunt for a new CEO in early 2023. Treharne must have been impressed by Will Orr, the new CEO, as they hired him in April and waited 6 months till November for him to take his seat. Treharne was the CEO at the floatation and still holds 1.63m shares, just under 1%. GYM has obviously not been a great long-term investment over its 9 years as a public company, unless you were lucky enough to sell out on the highs. They took a huge wallop through covid with the lock downs then bounced fast but since late 2021 it had been one long decline. In September 2022 the co appointed a new CFO, Luke Tait, formerly CFO at Nandos. A year later in September 2023, Will Orr joined as CEO, formerly MD of Times Media, part of News Corp. He was there for 3 year, prior to that he was MD of RAC Consumer Roadside for 3 years.

For a recovery play, there are 4 main things I look for. 1) The first thing I want to see is board changes which there is. 2) Next, I look for is a positive change to the chart, particularly a curve up which we have here too. 3) Third, I want to hear news that is at least less negative than it has been, better still, something slightly positive, which the interims were.

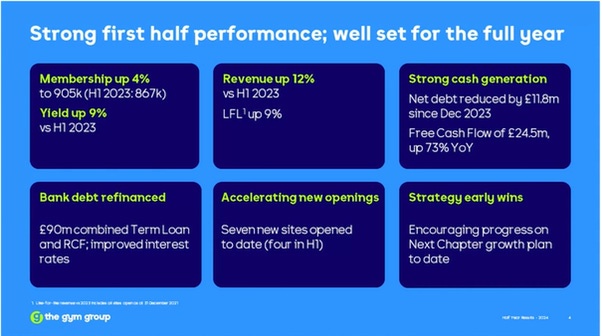

At the interim they actually made a 0.3p eps which, considering they had made a 4.7p eps loss last year as a whole, and were forecast to make a 0.2p eps loss this year, this looked reasonably positive, even if brokers only upped forecasts a gnats, although all 12 brokers in Stoko’s consensus have them as a “Strong Buy”. At this point, many investors get turned off because the forecasts show a loss for the year and at best a small profit, but the story looks much better imo. Since Jan this year, earnings forecasts have risen 3.3p, despite a big rise of nearly 11% in the minimum wage. It’s a very easy business to understand. They do have a fair amount of replacement per annum with new kit. Repairs, replacement and the like which amounts to around £45k per year, per gym and with 250 gyms, that’s £11m or so p.a. But with the high free cashflow that they have they can pay for that and the new stores while still paying down debt. If you can grow sales reduce debt and use cashflow to grow then just paying down the debt reduces interest charges and grow fast. They have refinance recently and lowered the interest payments and with cost savings they look like margins can increase and hopefully get back to the 15.8% operating margins of 2018. Currently on a trailing 12 months they stand at 9%. The growth can become quite exponential if done well, not letting debt gallop away and not expanding too fast or into poor locations just for growth sake.

GYM have members, members pay in advance on a daily, monthly or annual basis and that creates great cashflow opportunities with these up-front payments. If you are expanding a business and opening more stores you don’t need to borrow more or borrow at all if you can do it out of cashflow. If you open more profitable stores the eps rises faster as does the cashflow, if you can get the business working right, it’s the classic retail growth model that self-funds expansion and has worked for many retailers in the past too.

The operative phrase there though is “if you can get it right”, so can the new board return this into a growth story?

The 2024 interim results webcast is well worth watching:

https://vimeopro.com/instinctifpartners/the-gym-group-half-year-results-2024

The above slide shows strong progress and with 10-12 new sites being opened this year, they have refurbished around 150 sites, the other 100 sites will be refurbished in the coming year, making circa 250 gyms. 50 sites will be added in the coming 3 years. Sales this year are expected to be £224m, and £244m next year, that will be nearly double 2018. In 2019 they achieved 6.4p eps on £153m sales (4.3p allowing for dilution). If they get operating margins back to where they were in 2015 then on sales of £224m they would do something around 6.5p even allowing for dilution.

They increased prices 9% in H1 without reducing member headcount. Sales in H1 were £112m, half of what is expected for the year while growing at 12%. If the sales growth continues at that 12% rate this year then the £109m sales in H2 last year would become £122m sales in H2 making £234m sales for this year. Now I’m not saying they will do that but you can see they are ahead on the run rate in all likelihood.

The co has revised sales growth guidance for the year from 4-5% to 5-6% which having done 12% in H1 would pretty much mean no sales growth in H2, that just doesn’t jive with the rest of what the company says. In the presentation they say that growth has continued in July and August and into the important student sign up period. All of this suggests there is a good chance that the earnings forecast get dragged forward in my opinion.

So why would this be the growth area to invest in? Well today, gyms are becoming the new pub or club apparently. The youth of today are very fitness-aware, many go to the gym in groups together, or as couples and work out and socialise, compared to my youth when Friday night was 6 pints of Guiness and a Doner Kebab, today young adults prefer to be as peak fit and often as alcohol-free as they can - they will never have a physique like mine doing that :-) . The demographics and trends are strongly improving for low cost gyms. The Gym Group is cheaper headline priced than their competitors but have been narrowing that gap while competitors raise their prices and there is headroom for higher prices.

Net debt has fallen £30m to £385m over the past two years and a recent refinancing has reduced interest payments but this includes leases under current accounting. More importantly in my opinion, the “genuine net debt” at the interims, excluding leases was £54.6m, down from £69.7m at the interims last year. At the start I said I looked for four indicators for a recovery play and only listed three. The fourth is director buying. On Thursday, a non-exec director bought 12.5k shares @ £1.62, which is a start.

All in all, growing revenues, increasing margins, increasing cashflow and investing that cashflow into more sites is a recipe to get the eps and cashflow rising fast and higher if they continue their performance. Basically, my view here is that the company is likely trading ahead of market expectations. They said at the interims that they expected to deliver results at the top end of recently revised forecasts – I think they are on course to do better than that, hence I have been buying. Are the new CEO and CFO turning this around? Will Orr has been in place a year and the news is turning more positive and the chart perking up – I like to see a share respond within 6-18 months of a new board and tangible improvements. That seems to be the case here.

The next scheduled news is the year end trading update on January 14th according to their website, although that doesn’t rule out one sooner. All in all these look rather interesting to me, they look as if they are potentially under estimated by the market, which is why I am a buyer here.

This is not a tip or meant as advice, I am just sharing my research to help others save some time perhaps and flag something interesting. Obviously like all shares you need to do your own research as only you know your own risk/reward profile. As I am a holder of GYM shares, anything I say will likely be biased or this could be completely wrong or a pack of lies and you will never know without verifying it so please do your due diligence.

Other reading:

Gyms beat pubs for a Gen Z night out

https://www.thetimes.com/uk/society/article/gyms-beat-pubs-for-a-gen-z-night-out-gbzcnx28v

The Gym Group furthers its early adopter status, by achieving FITcert Level 4 certification

Rising membership and prices lift Gym Group back to profit

https://www.ft.com/content/40ae47db-d51a-4575-be03-e836166c9ff6

The Company Interim Webcast

https://vimeopro.com/instinctifpartners/the-gym-group-half-year-results-2024

Cockney Rebel.

Cheers, yes, I pointed out the maintenance and repair costs, rather like airlines.

However the growth and cashflow significantly outweighs that for me and without the sauna and stuff the higher end subscription models provide, they are at an advantage there imo.

I'm expecting cashflow to improve significantly too.

I floated this company in Nov 2015. The issue is the relatively high maintenance capital intensity. The business model is sound - like LCCs like RYA - lowest cost and lowest cost to serve