Rebel Weekend Review, Sat 23rd March, 2024

Here Comes the Sun

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required.

Another week through March and as the days get longer it’s easy to get bored watching a slow market. This week I was saddened by the news that Cockney Rebel lead singer and writer, Steve Harley, had gone to that big recording studio in the sky. Their music was the sound track to my youth with so many other great artists and writers. Music hit its apogee in the 70’s, I grew up in the greatest times ever in the 70’s although nobody realised it at the time. Even tho many songs like Brotherhood of Man’s ‘Kisses for Me’ or Dawn’s ‘Knock Three Times’ we so corny, they were at least happy songs, you’d moan about them as a teenager then find yourself humming them. Today its all computer generated trash and depressing grey mash with some PC drumbeat sampled for the tenth time by people that don’t have 1% of the guitar talent of Clapton or Hendrix. Where’s a Cozy Powell drummer these days? We are fast losing the music giants sadly, replaced with Random Access Memory.

At least over the past week we can be grateful for a bit of a rally of sorts. The inflation figures came in on Wednesday and were better than expected for all the data aside from Producer Prices. I did say last weekend that I expected the bowl on the 250 to break out this week and so it just about did after a half-hearted rally on Weds and the Fed meeting Wednesday night, it left just the Bank of England decision on Thursday to get out of the way for a 1.3% rally. The real question is why was one lunatic at the BofE still voting for a rate hike? Anyway, with that out of the way the FTSE250 went on to actually close higher than where it opened at the start of the year for the first time in 2024. It was only by around 15 points but it got there intraday and on a closing basis. The next resistance on the 250 is about 2% higher. There was no follow through on Friday but I’m cool with that as the next leg up should confirm the break out and send the FTSE250 higher sill imo. Buyer confidence seems to be improving but there always seems to be some bad news somewhere waiting to spook the punters.

There’s plenty more results and trading updates in March and April to make the market wake up to the undervaluation so I am still 100% invested. I’ve been a bit more active this week.

Trustpilot TRST posted good results on Tuesday, posting an 18% rise in revenues and bookings, a $7m profit compared to a $15m loss last year and a net cash position of $91m, up from $73m last year. The shares rocketed on the open, going into auction , soaring 10%+ to 234p, after Berenberg put out a 260p target and a Buy rec. Then at the close Berenberg announced they were sole bookrunner for a 12m share secondary placing for major shareholder Vitruvian. The placing was done at 200p. Trading in the market the following day saw them walloped down to 183p support on the chart. At 50p off the previous day’s high I picked up a few shares. Dunno if I want to hold or trade them. They have a great bowl and great momentum but I’ve only bought for a trade, the actual valuation is a bit rich for me. I will likely trade out short term.

Another investment this week has been Yu Group, YU. You Group describe their services as:

“Trading under the brand Yü Energy, our multi-utility offer spans electricity, gas, water and other solutions for business customers across the UK, including playing a key role in supporting them in their transition to lower carbon technologies. We are committed to providing sustainable energy solutions to our customers, including the option to source 100% clean energy as part of our Pure Green plan”

“Our multi-utility offering and excellent customer service is focused on making it easier for businesses to manage their utilities. We are a direct supplier, not a broker, employing a range of routes to market in order to drive scale. We serve primarily small and medium-sized businesses across the UK – a £50 billion addressable market offering significant scope for growth.”

Rather than re-write all the attractions, here is the company’s Investment Case Page link, a 5 min read:

https://www.yugroupplc.com/investment-case/

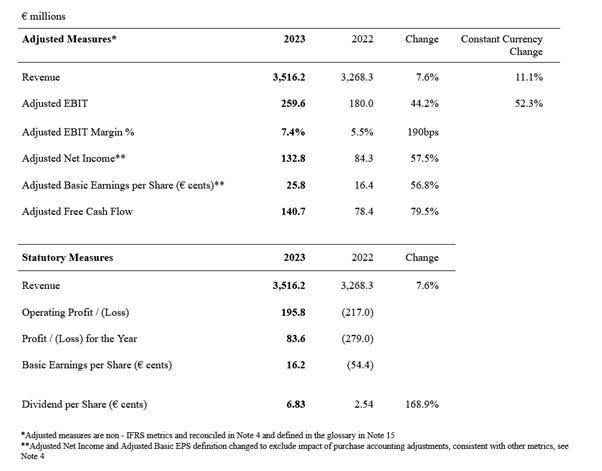

The company posted some great results on Tuesday, these are just some of the highlights:

There are loads more big numbers, all very positive including net cash of £32m. All too much to post here but worth a read of the full results RNS imo. Supplying businesses with energy and growing at a pace, Yu Group should also benefit from greater roll out of smart meters too. None of the directors have sold any shares since floating in March 2016 at around £2, now £15. Bobby Kalar, CEO holds 51%. Some may dislike that but actually I think them having grown so much and he hasn’t sold makes them interesting. I’m sure a fund or two will get interested at some point and want to acquire some in size and it will give him the opportunity to reduce and make the shares look even more attractive. Meanwhile it has been good to see no directors selling into what has been a great rally.

Currently on a PE for this year of 8.8, paying a divi of 40p and forecast to have free cashflow of £81m the company looks very cheap imo, so I have been buying. Had my eye on them for some time, I need to do more research still to make them a major holding but fit the “onebagability in a year” criteria to make the cut as a hold. Liberum forecast they will have £110m net cash this year, a huge jump from the current £31m and nearly half the market cap in net cash going forward. The chart has recently broken the all time high.

Yu Group Chart

Another I have been buying after full year results two weeks ago is TI Fluid Systems, TIFS.

I have watched this company for a long time and watched them bottom last March. At that point the results never looked good enough to give me confidence to buy. By H1 last August they were back in profit with 6.8c EPS. At around 140p it never looked cheap enough to buy then. Since Aug the price came back a fair bit and two weeks ago they announced what looked like very good numbers to me.

What interests me is they had a new CEO in September 21, the chairman has changed and they had a new CFO a year ago. That’s a good board change which I like to see in order to want to buy. The chart is also making a great bowl and has broken through the highs before the August results, bottoming just after the new CFO took his position, the company waited over 6 month for him to join, so he should be good. TI Fluid Systems make tubing and connectors for fluids, like break fluid. These things used to be aluminium or rubber but now they are made of a composite material which is just as strong but way cheaper and lighter by over 50%. Weight means cost when it comes to building cars. TIFS are exposed to the motor industry but even if EV’s slow, the growth will be there in Internal Combustion Engine Cars. EV’s use 2-4 times the amount of cooling as an ICE car so that increases demand.

This is well worth watching, the Capital Day from late 2023 – lots of interesting slides and the CEO is Scandinavian so he sounds very intelligent 😊

On a PE of 7.1 falling to 6, paying a yield of 4.23% rising to 4.83% and what looks like momentum building from the new board, I think they look good value and have bought. Scores well on Stockopedia and the chart is a fab long term bowl that’s just getting going as a recovery play.

TI Fluid Systems have net debt of £728m, 80 % of the mkt cap. But the co seems cool with that, in fact they are doing share buy backs and paying an increasing divi of size, and the debt is down £170m (20%) from 2019. Q1 trading update should be early May.

I was already holding a few MPAC before their year end results on Tuesday. I thought the results were very good. With underlying Eps of 26.2p, nearly double last year, and 38.7p forecast this year, that looks like strong growth on a fwd PE of 9 imo. I have known this company since it was Molins, making tobacco machines. Now it is a very good, world class, production line designer and manufacturer/installer/servicer. They have net cash of £2.1m. I like the recent CEO Adam Holland, he came across very well in Yesterday’s webcast results presentation. He has a good track record having come from AEA Technology, Rolls Royce Plc, Siemens and then JCB. The recording of the presentation is worth watching and should be on the company website now. The added spice is that MPAC are currently designing and building a prototype production line for car battery company Freyr in Norway. The forecasts have nothing built into them for this, or what the follow-on orders would bring in. This could be a game changer. They are also working with battery maker Ilika.

I added a few while watching the presentation and later on – really worth watching imo, it should be on their website now.

As far as other existing holdings go, Rolls Royce RR. had a number of upgrades and sizeable ones which sent the shares sharply higher:

JEFFERIES RAISES ROLLS-ROYCE PRICE TARGET TO 470 (390) PENCE - 'BUY'

UBS RAISES ROLLS-ROYCE PRICE TARGET TO 550 (400) PENCE - 'BUY'

GOLDMAN RAISES ROLLS-ROYCE PRICE TARGET TO 524 (398) PENCE - 'BUY'

It’s interesting that all these brokers are hiking their forecast and targets suddenly again.

M&S also saw an upgrade

RBC RAISES MARKS & SPENCER TO 'OUTPERFORM' (SECTOR PERFORM) - PRICE TARGET 300 (285) P

I am expecting an unscheduled trading update in the next few weeks, ahead of the results in mid May. Next put their results out on Thursday and raised guidance, this saw Next hit new highs – that bodes well for MKS performance too imo.

Warpaint London W7L and Ashtead Tech, AT. both hit new highs.

Judges Scientific, JDG which I bought a few weeks ago, posted very good results but it looks up with events imo, so I took my profits there rather than hold long term, as I can’t see it doubling in 12 months. I spend my time trying to trim my portfolio down so regularly go through trades and decide whether they are continuous holds or need to be trimmed. Too many stocks dilute your gains. It’s been a good week for the portfolio with RR., MKS. AT., CMCX, BMY, AVON and GAMA all performing great and adding 4%+ for this week to the portfolio. It’s about time I had a week like this, well overdue. I hope all the readers hear have had a great week too.

That’s mainly been my week. Please remember I hold most of these shares I’m talking about so I am biased, or at least not totally objective, so please do you research.

GAMA Communications, GAMA have results on Monday so I’m looking out for them.

I’ll leave you this - introduced by the late Steve Wright too

Rebel

I've learned something, cheers!

RIP Steve