Card Factory updated the market today with what looks to me some excellent results:

The highlights for me were:

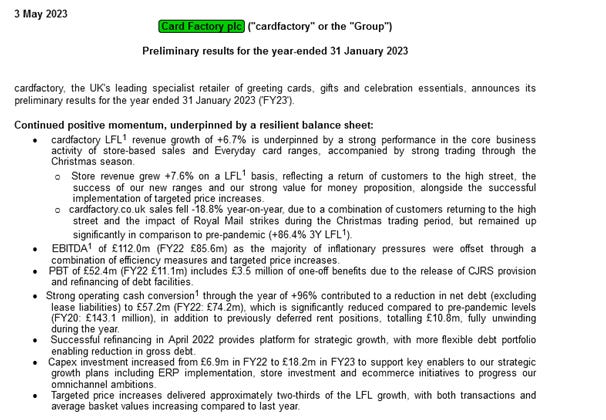

Sales at a record high.

Pre-tax profit at £52.4m – bear in mind at October the forecasts were for circa £34m pbt, so over the last 6 months the company has delivered 50%+ more profit than expected which also fell right through to EPS with 12.8p diluted EPS, 20% above the consensus forecasts.

Net debt now stands at £57.2m (FY22: £74.2m), a £17m reduction. This was despite having paid off circa £11m in deferred rents. They also spent a lot on investing in a new ERP system so that stock data can be tracked throughout the business and they also combined their gettingpersonal.co.uk website with the new Card Factory website which will save costs and attract greater sales. The company said current trading was slightly ahead of co expectations in the first quarter.

Looking at what the company says, they now expect sales of £650m by 2027 and PBT margins of 14%. This seems to be a conservative estimate, seeing the trailing 12 months operating margins were 11.6% and this year’s margins were 13.7% by my calculations, which should mean H2 operating margins were well over 14% already. But I prefer a company that guides low and delivers high as we have seen recently. The likes of Dunelm only manage 12% operating margins.

Price increases never got enacted till H2 so we go into H1 with prices a lot higher than last year. H1 this year should see lower shipping costs, lower cardboard buy-in prices and a stronger £ v $ so significant tailwinds although they are well hedged on currency till 2024 so any currency gains will be down the line.

Click and collect which had been trialled in 85 stores has now been rolled out across the business. This drives people into stores and they are picking up additional items while in-store which boosted basket size and price.

Additionally to the recent announcement regarding the acquisition on SA Greetings in South Africa the co said they had signed a long-term master franchise agreement with Middle East-based, Liwa Trading Enterprises, who will act as exclusive franchise partner in the region, to open cira 36 Card Factory branded stores in the Middle East. These both add to the existing international partners the Reject Shop who already sell Card Factory goods in Australia. Card Factory have a capital investment plan of £24m per annum, over the next three years to increase earnings.

Listening to the presentation today they now have 1032 stores. 17% of Card transactions now see a gift sale as well. Total sales seem to be 53/47 Gifts v Cards now based on cost. The company has revised its addressable market up from £5bn to £13.4bn in the UK alone, after recent research.

As far as financials go the co is expecting 14% PBT margins by 2027 and say that a divi will be payable from January and will be 2-3 times covered.

The international expansion looks very interesting and looks capable of expanding sales and earnings strongly. They expect to capital invest £24m per annum in diving growth which should bring appropriate returns. Most of the international roll out is capital light, with franchise partners paying the bulk of the costs. It really is a lot to relay her but I recommend anyone investing or interested go to the investor page on the co website and watch both presentations, especially the Capital Markets Day presentation which is very enlightening. Darcy Wilson Rymer has really delivered over the past two years and that gives me the confidence that this guy knows what he is doing, he’s ambitious and knows how to promise modestly and deliver surprisingly positively in my opinion. I continue to back him as a guy that knows what he’s doing. A very exciting holding for me with the high earnings growth, high cash generation and likely return to the dividend list before too long.

Traders who have jumped on board off the back of 3 huge profit upgrades recently obviously banking profits today, which may provide an opportunity for people who like the cashflow and a PE of 8 or perhaps a lot less going forward,

All obviously just my opinion, I’m heavily invested so biased so obviously do your own research and confirm what I have said.

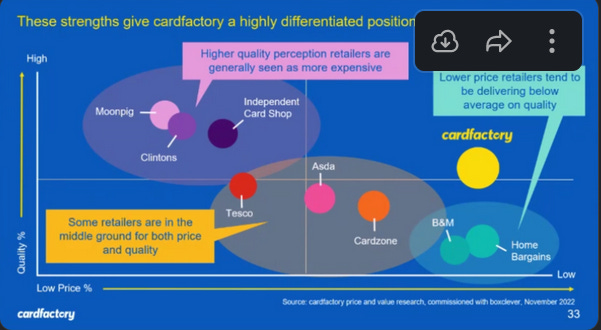

Two very interesting slides from the presentation

Darcy's targets are always conservative, that's why profits beat by over 55% from wher they stood in October imo Martin. He hasn't over-promised by a long shot imo.

Some of the targets seem very modest, e.g. for UK store sales, so hopefully they have set modest targets which they will strive to well beat.