AVON – Avon Protection Final Results 21st Nov, 2023

update.

This is just some thoughts, it isn't investment advice or incitement to buy in any way, just my views - please do your own thorough research. I’m not an analyst, I’m just a private investor looking after my own money. Nothing I do or say is meant as advice or should be taken as such. Here I publish my ideas and research that I have done and discuss the way I invest. Anything written here needs to be verified for its accuracy. Assume any stock I write about I likely own, so my views are biased. Inevitably I will get things wrong, everyone is responsible for their own decision making and what they buy and sell. Subscribing and reading this article means you accept the above and you take full responsibility for your own actions and decisions. Small Cap stocks can be illiquid and very hard to sell at times when demand is weak so caution is required. Well the rain has killed any hope of doing anything meaningful outside today so time for a weekend review again this week. There’s a fabulous feeling about the market currently imo, although many may not feel it. When investors/traders sell off just because they cannot take anymore, when they just want ‘pain relief’ or 5% guaranteed from gilts looks attractive compared to fluctuating equities that may fall at times and not even pay a yield, you know there’s a lot not participating long in this market. So why do I feel bullish (apart from the fact that I am always optimistic and often get called a perma-bull) ?

Subscribe for free here:

Today, AVON released their interim results. These are the first Final Results under Jos Sclater, the new company CEO just 10 months ago.

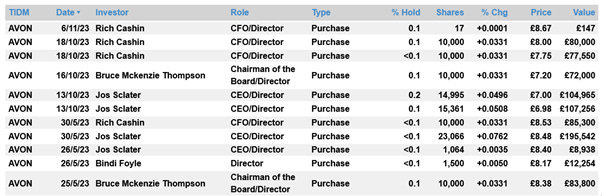

I like recovery plays because you can see where a company has been and what it can achieve by looking back at the chart and the prior few years and more. The results today are a bit messy in as much as the company has fully disposed of the badly performing Armour Business, acquired by the previous board. In all recovery plays and buying into them there are several things I like to see. Firstly I need to see a new board. Avon has both a new CEO and a recent CFO. I like to see director buying and recently:

There is usually a 6-8 week closed period ahead of the results in which directors cannot buy or sell shares so I was surprised to see directors heavily buying shares 4 weeks before the results, after a trading update. However that did say to me that there wouldn’t be anything overly on the positive side in these results as that would look a bit shabby so soon after director buying. I was looking to these results as the point to put all the bad news out in the public domain ahead of the next update when things can then look very much on the up hopefully. The company has announced a Capital Markets Day in Feb 8th. At this point Sclater will have been at the helm for a year. I’ve been pleased to see the co being upbeat and directors buying just 8 months after Sclater took the helm, this meets the speediest of recovery evidence I expect to see in a recovery play. I feel February will be where Sclater unshackles himself from the past and it becomes fully his responsibility with a year under the belt so I expect by then he will want to show clear progress.

The highlights from today were.

Dilute Earnings per Share 40.3c adjusted for the disposal of the Armour business and other one offs. This compared favourably with the 26.2c forecast on Stockopedia which itself was upgraded by 20% recently.

The company has already signalled the re-base of the divi, paying a 15.3c final divi and the annual divi will be rebased on a 1/2 split so H1 divi in the coming year looks like being around 7.5c for circa 22c-23c going forward.

Closing order book up 10.9% on last year.

On the past basis most measures were down on a continuing operations basis but as ever, I prefer in a recovery play to concentrate on the forward prospects. “Results in-line with expectations and order book to support growth in 2024” is how the company described the results.

Continuing operations1

Orders received

$258.7m $267.9m (3.4%) (2.9%)

Closing order book

$135.8m $120.9m 12.3% 10.9%

Revenue

$243.8m $263.5m (7.5%) (7.5%)

Adjusted2 EBITDA

$35.7m $38.8m (8.0%) (13.6%)

Adjusted2 operating profit

$21.2m $23.4m (9.4%); (18.5%)

Adjusted2 profit before tax

$14.0m $19.7m (28.9%) (37.5%)

I prefer in a recovery play to concentrate on the forward prospects. These numbers and most of the other stuff the company has put out today are to clear the decks for the Capital Day in Feb imo, when Sclater will have his one year anniversary. These included

Statutory operating loss from continuing operations of $12.6 million (2022: profit of $11.0 million) reflected exceptional items.

Impairments include a $23.4 million charge to goodwill.

The company will make payments in FY24 of £6.95 million, FY25 of £4.30 million and FY26 of £4.70 million in respect of deficit recovery and scheme expenses.

I won’t list the lot here as they are clearly listed in the RNS but it reads like a ‘kitchen sink’ list of stuff Sclater wants out the way for the bigger better show in the coming year imo.

The company said they were through the first leg of their STAR Strategy, moving from Strengthen now onto Transform. There’s a 5min presentation on the company website here, worth watching:

Basically nothing came as much of a surprise here in my opinion, to me or to the market with the stock price rallying 28p initially then coming off 20p as the rest of the market weakened today. Margings are set to grow, the co targetong ‘mid teens’ operating margins. Sclater reckons he can save £1m p.a. for each of the factories just by reducing wastage.

The question I ask myself with all these recovery plays is ‘what’s in the price and what’s the risk?

For me the downside is to the £6 bottom made recently, I feel comfortable with that considering the potential upside. I feel the market clearly liked the statement there and the stock has rallied strongly since. Traders jumped on board and took the stock up to £9 and it has come back to 770p now. The thing for me is that trying to buy a recovery play I just can’t wait till the company sounds jolly and upbeat because the stock is illiquid. If I’m fighting for shares when I buy with funds and large investors that all want to buy too then I’ll be paying a lot more in all liklihood imo. Taking into account all the bad news is likely in the public domain here, bearing in mind the heavy director buying and the drag of the Armour business gone then I think this is a point where I want to be long. If you watch in interim presentation from months ago it highlights clearly that orders are often delayed due to getting gov sign off or changes in spec. Helmet orders are set to go from nothing to 75k a year at one factory and helmet demand is likely to soar after Ukraine and Israel events. Helmets have a 1-2 year lead time so orders made after Ukraine will only be getting sign off and delivery from here onwards. Sclater has been there and done it with other companies as far as recoveries go so I’m willing to back that here. Others obviously might want to see more evidence and be prepared to pay a higher price for the privilege – that’s what makes investing so interesting. There was a lot of miserable numbers put a line under today and that’s often what spooks novice investors. The fact there wasn’t any big sell off says to me I’m not alone buying here.

I’m more interested in focussing on this being a world leading business with a big moat and barriers to entry and that makes it an interesting and sought after investment to me, needing to rise nearly 6 fold to get back to its hold high, and having had no dilution, while paying a 2% yield going fwd roughly.

All just my opinion and how I invest, just for informative reasons.

I’m not a qualified analyst, just a private investor so do your own research imo.

Rebel

Cheers, that's Ancora Advisers who have 5%. They want the co put up for sale.

thank you